Mar 12, 2024

• US equities discount more of the same – growth and low interest rates

• A more sobering view has less growth and higher interest rates and hence lower valuation

• A serious correction in the near-term maybe headed off by the near term hope of robust growth, lower interest rates and a future corporate tax cutting President!

• US employment report was a messy set of data with underlying strength

• The balance of risks is skewed to a stronger than expected US inflation report

It Equity markets drifted lower on Friday, but not before scaling new highs earlier in the week. The S&P500 hit an all-time high on Thursday before the markets put in a mixed performance on Friday after a slightly confusing US jobs report.

This week’s US inflation report will be key for market sentiment. Macro data in recent weeks has pointed to stronger-than-expected inflation, but that strength has not been sufficient to either seriously worry the bond market or prompt the Fed to consider serious delays to a rate cut. Indeed, last week Fed Chairman Jerome Powell appeared to want to dispel any notion that a rate cut would not be forthcoming. Maybe Powell was taking on those in the market who rule out any rate cut this year or some such as Larry Summers who, in fact, talk up the risk of a possible rate rise.

Chart 1: US CPI Due This Week; Market Expects Unchanged Headline Inflation at 3.1%

Source: Bloomberg

US jobs report: Underlying strength in an otherwise confusing report

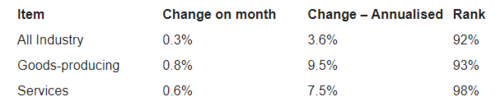

The US labour market report highlighted stronger-than-anticipated headline job growth. Adjustments to the figures from the prior two months brought the total growth back in line with expectations. A detailed analysis of the report reinforces the view that US growth remains buoyed by a dynamic services sector. However, for those anticipating a rate cut in the near future, the possibility of a resurgence in the manufacturing sector could mean interest rates remaining unchanged for longer than expected. Notably, the monthly uptick in hours worked within the manufacturing sector reached the upper limit of typical monthly fluctuations (Table 1).

Table 1: Selective Lines from the Industry Subsectors for Hours Worked

Source: BLS and Investor Acumen

US equities navigating the bear perspective

The US equity market, despite the headwinds of challenging inflation data, has continued to perform well. However, the heady valuations should make you pause for some reflection. Here, we would like to quote from an article by Stuart Allsop at Icon Economics on the macro challenges to a high P/E multiple the market ascribed to the S&P500. Let us first say that the valuation of an equity market provides limited value in timing a purchase or sale. In any quantitative trading model trying to predict the exact time to buy or sell an equity market the valuation of the equity market is typically given a low weightage. However, it is also true to conclude that buying or selling markets when they are on a high/low valuation increases the chances of getting your positioning right for the longer term.

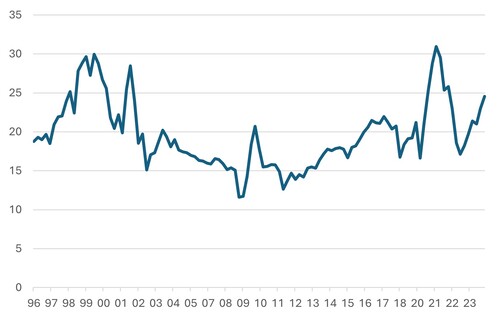

The US equity market trades at a P/E multiple of 24.5x historical earnings, with only exceptions being COVID times when earnings collapsed and the tech bubble of 2000 when the market peaked at a P/E of 30x.

Chart 2: S&P500 Current P/E Multiple

Source: Bloomberg

Unravelling the unsustainable forces in the US equity market

A critical examination of the current bear view on the US equity market reveals a building consensus around the unsustainable nature of recent macroeconomic tailwinds. The apprehension centres on the premise that the macroeconomic factors fuelling the market’s elevated valuations are fleeting. Here’s a closer look at the underlying concerns:

Unprecedented Corporate Profits: The US corporate sector has witnessed a remarkable surge in profit margins, now standing at 11% of GDP, and sales alike. Such levels pose the question of sustainability, hinting at the ceiling we might be hitting.

Depleting financial reserves: Both household savings reduction and governmental fiscal deficits have temporarily buoyed the economy. However, with potential GDP growth pegged at a modest 1.5%-2.0%, the runway for further growth appears limited.

Deteriorating Financial Health: Since 2000, there’s been a marked decline in the financial stability of the corporate and government sectors, highlighted by increased government debt-to-GDP (from 54% to 121%) and a shift from a government fiscal surplus to a significant deficit (from +1% to -7%).

The corporate sector’s fragile foundation

The boost to GDP growth, fuelled by government expenditure and a dip in savings rates, has temporarily favoured the corporate sector. However, the looming threat of reduced GDP growth rates and the potential for higher long-term interest rates because of fiscal challenges paint a grim picture. The Federal Reserve’s projection of a mere 1.8% long-term real GDP growth, coupled with an expected inflation rate of 2.2%, implies a restrained corporate revenue growth forecast of 4%. This scenario, even with sustained profit margins, suggests a subdued profit growth outlook, starkly lower than the historical average of 6.4%.

US equity valuation dilemma: A mathematical conundrum

The valuation of the equity market hinges on the principle that equities should yield a return that accounts for the bond market yield plus a risk premium.

Box A

To simplify the math around valuing the equity market, equities must return the bond market yield plus a risk premium, considering the greater risk of holding equities. So, a simple equation is:

Current dividend yield plus long-term dividend growth = bond yield plus an equity risk premium

Dividend yield (3%**) plus dividend growth (4%) = bond yield (4.1%) plus risk premium (4.8%*)

**The current yield of the S&P 500 including share buy-backs is around 3.0% (dividend yield just 1.4%).

*Historical average

A glaring mismatch exists in the current equation (see Box A), indicating a shortfall of 1.8% and suggesting an inevitable adjustment in equity market valuation. This adjustment could manifest as:

• A decline in US government bond yields.

• A reduction in the equity risk premium demanded by investors.

• An increase in the equity market dividend yield, potentially necessitating a market correction as drastic as 38% in a worst-case scenario.

• A note of caution amid short-term optimism

While the current market valuation provides scant insight into short-term performance, several factors may temporarily sustain the US equity market’s strength. These include stronger-than-expected economic growth, signals from the Federal Reserve of a forthcoming rate cut, and the perceived corporate-friendly stance of a potential Trump presidency.

Nevertheless, while short-term factors may provide transient support, the bear perspective underscores significant structural concerns. Investors would do well to navigate this landscape with a cautious and informed approach.

Egypt: Is this time for real?

Egypt, a nation brimming with opportunity and home to more than 100 million inhabitants, has recently experienced a wave of positive economic developments. The Egyptian government has implemented economic policies that have secured a substantial support program from the International Monetary Fund (IMF) and other international entities. While these economic adjustments have come with their challenges, including a devaluation of the Egyptian pound by nearly 40% against the US dollar and an unexpected 600 basis-point hike in interest rates by the central bank, these moves have surpassed market anticipations.

The future stability of the Egyptian pound is further bolstered by support commitments from the governments of the United Arab Emirates and Saudi Arabia, both of which are poised to make significant investments in the Ras Gamila area, located near Sharm el-Sheikh. Furthermore, ongoing negotiations with China aim to establish a large industrial export zone along Egypt’s Mediterranean coastline. This series of strategic moves and international collaborations underscores Egypt’s promising economic trajectory. Reflecting these developments, the EGX index has surged approximately 70% since last September, effectively compensating for the depreciation of the Egyptian pound against the dollar.

Chart 3: EGX30 Index Performance in USD

(rebased to March 2023 =100)

Source: Bloomberg