Mar 13, 2026

Fundamentals Improve, but Geopolitics Looms

After nearly 18 months of significant underperformance relative to global peers, the fundamentals of the Indian markets had begun to show signs of improvement. Economic activity was indicating a gradual rebound, earnings growth had picked up, and valuations across several segments of the market had moderated.

However, these positives now risk being overshadowed by escalating geopolitical tensions following the U.S. and Israel’s attack on Iran, and the potential implications for global oil prices. India remains heavily dependent on energy imports, sourcing around 85% of its crude oil and roughly half of its LNG requirements from overseas. About 40–50% of crude oil and 50–60% of LNG supplies are transported through the Strait of Hormuz, a key maritime chokepoint that has now come into sharp focus for India as well as the rest of the world.

Source: Bloomberg, Sanctum Wealth

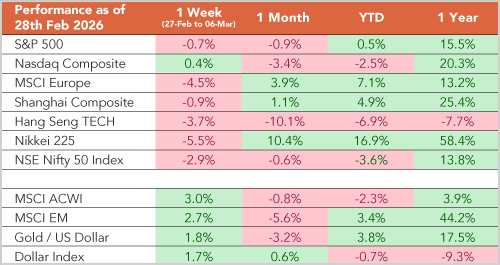

Above returns are only price change and not total returns

We recently concluded our quarterly Asset Pair Model review, which guides our tactical asset allocation decisions. The model indicated a positive bias toward equities, with a preference for mid-caps over large-caps. It also suggested a marginally positive outlook on the INR and a neutral stance on gold. However, the escalation of the Middle East conflict occurred after our review and has somewhat influenced our near-term assessment. In this note, we discuss the potential implications of the conflict for Indian markets and outline our more longer-term outlook.

Impact of Middle East Conflict

The current Middle East conflict differs significantly from the 12-day war in June 2025, when U.S. involvement was limited and Iran’s retaliation was largely directed at Israel. This time, joint U.S.–Israel strikes have sharply escalated tensions, including the killing of Iran’s Supreme Leader. The development appears almost existential for the Iranian Revolutionary Guard (IRGC), prompting Iran to target U.S. bases across several Gulf countries.

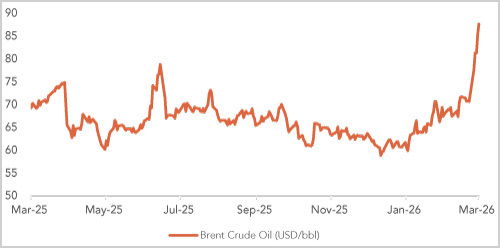

The escalation has led to the closure of airspace across the Gulf and has sharply slowed traffic through the Strait of Hormuz. The strait is critical to global energy markets, with nearly 20% of global oil and LNG trade passing through it. Energy markets have reacted swiftly. Crude oil prices briefly touched USD 120/bbl before settling around USD 90/bbl at the time of writing, up from about USD 66–67 in early 2026. Meanwhile, LNG prices have nearly doubled in Asia and increased by more than 50% in Europe.

Brent crude oil has shot up

Source: Bloomberg, Sanctum Wealth

To put the situation in context, global oil markets were in surplus before the conflict, with roughly 3 million barrels per day (bpd) of spare capacity which is close to Iran’s current production of 3.3–3.5 million bpd. However, most of this spare capacity is located in the Middle East and would also need to move through the Strait of Hormuz. At the same time, global growth was slowing and inflation moderating across most major economies. But the oil shock now adds a source of uncertainty.

The Middle East conflict has multiple dimensions. Beyond energy markets, it carries significant geopolitical and U.S. domestic political implications, with mid-term elections scheduled for November 2026. These developments are likely to influence markets in the near term.

A short-lived conflict followed by rapid de-escalation could push crude prices higher temporarily before they return to the USD 60–70/bbl range over the coming months. With elections approaching, the U.S. administration may be inclined to limit inflationary pressures, keeping the broader economic impact contained. In such a scenario, market weakness could present a buying opportunity for investors.

A longer, regionally contained conflict lasting several months, without major disruption to the Strait of Hormuz, could sustain elevated oil prices in the near term as uncertainty persists. However, prices may gradually normalize if OPEC+ compensates for any supply losses from Iran. Global inflation risks would rise in the near term, central banks might delay rate cuts, and emerging markets such as India could face wider current account deficits, currency pressure, and selective earnings downgrades for a few months before conditions normalize. Markets may remain under pressure initially before stabilizing. In this environment, a staggered approach to investing may be prudent.

A more severe scenario, where the conflict persists for months and shipping through the Strait of Hormuz is significantly disrupted, would have serious implications for global economy and markets, particularly for energy-importing economies like India. At present, however, this outcome appears unlikely at present.

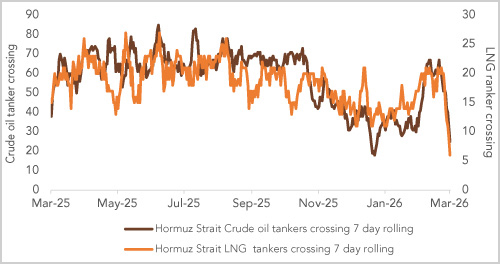

While the situation is evolving, Iran has stated that the Strait of Hormuz remains open and that it has no intention of closing it. Nevertheless, shipping activity has slowed as insurance costs rise and crews weigh safety risks. In the coming weeks, developments in the Middle East are likely to remain a key driver of market sentiment.

Crossing through Strait of Hormuz has plummeted

Source: Bloomberg, Sanctum Wealth

Global Macro Update

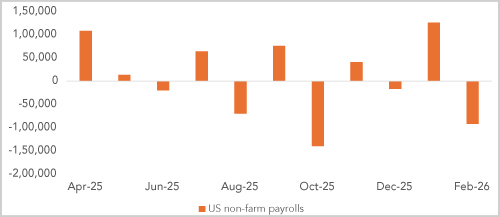

Even before the Middle East conflict erupted, global economic data suggested a modest and uneven growth environment. In the U.S., the labour market has shown signs of weakening. Non-farm payrolls unexpectedly declined by 92,000 in February against expectations of a 59,000 increase, while the unemployment rate edged up to 4.4%. Job growth has been volatile in recent months, with the six-month average now negative 1,000, raising concerns about underlying labour market momentum.

U.S. job market has weakened significantly

Source: Bloomberg, Sanctum Wealth

Consumer spending has so far remained resilient, but a softer labour market is likely to weigh on demand with a lag. At the same time, inflation had been moderating, with U.S. CPI slowing to around 2.4% in early 2026. However, the surge in oil prices following the conflict has already pushed gasoline prices higher, raising the risk of renewed inflationary pressure.

Overall, the U.S. economy was entering the conflict with weakening growth momentum. A prolonged rise in energy prices could therefore create a difficult policy mix, with slower growth alongside higher inflation, complicating the Fed’s policy path and increasing stagflation risks.

Europe’s economy remains fragile, with manufacturing still weak amid soft external demand and the lingering effects of tighter financial conditions over the last two years. While the pace of contraction appears to be easing and services activity has been relatively resilient, the region’s heavy dependence on imported crude oil and LNG adds to uncertainty amid the Middle East conflict. Higher fiscal spending, particularly on investment and defence, could nevertheless provide some support later in the year if the situation in the Middle East improves.

Japan’s economy showed renewed momentum in February, supported by domestic demand and improving corporate and wage dynamics. Structural reforms and stronger corporate governance underpin business confidence. However, Japan’s heavier reliance on oil and gas imports than Europe makes its outlook particularly sensitive to developments in the Middle East.

China is also dependent on energy imports, but its strategy is more diversified. It sources crude from a broader range of suppliers and holds substantial strategic reserves, and its closer economic ties with Iran and Russia may help secure supplies even amid disruptions. Additionally, Beijing could mitigate risks through policy tools such as stock releases, subsidies, or price controls.

South Korea’s markets have rallied sharply over the past year, with the KOSPI more than doubling. However, the equity market remains highly sensitive to energy prices, as the country’s energy-intensive industrial and semiconductor sectors face rising operational costs when electricity and fuel prices increase.

India Macro Update

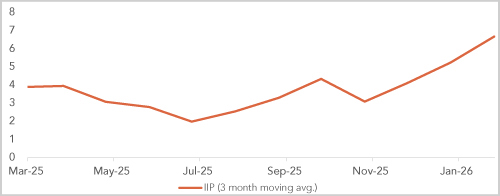

Most high-frequency indicators point to improving economic activity in India. Banking metrics—non-food credit, personal loans, and industrial credit—are all growing in double digits. Industrial activity is recovering, with IIP averaging over 5% in the past three months, while railway freight, e-way bills, and vehicle registrations remain steady. Rural consumption is relatively strong, supported by higher farm incomes, MSP hikes, and easing inflation. Urban demand remains muted but is set to recover as real wages rise and price pressures ease. Overall, private consumption is expected to strengthen to 7.7% in FY26 from 5.8% in FY25, signalling broad-based economic improvement.

India’s economic activity is improving

Source: Bloomberg, Sanctum Wealth

Meanwhile, India’s CPI inflation rose to 2.75% in January 2026 on the new 2024 base but remains benign. The uptick partly reflects a lower weight for food in the basket, consistent with shifting consumption patterns, while core inflation, excluding food and fuel, moderated during the month. Inflation may edge higher in the coming months due to a low base but is unlikely to pose a major concern unless there is a significant spike in oil prices.

While India’s growth is strengthening and inflation remains benign, the country’s external macroeconomic position is also more resilient compared with previous oil shocks. Fiscal prudence has kept the deficit under control, the current account deficit is below 2%, and forex reserves exceed USD 725 billion. The rupee appears undervalued, having depreciated significantly in recent months. FPI ownership of equities is at record lows, as emerging market funds remain underweight India, reducing the risk of sudden capital outflows in the near term. Oil marketing companies may absorb some of the price increases, and the government could adjust excise duties. However, prolonged high oil prices would weigh on government finances and could have broader macroeconomic implications.

India’s strategic petroleum reserves cover only 75 days, below the recommended 90-day level, limiting immediate buffers against supply shocks. Overall, while India is better placed than during past oil shocks, sustained spikes in oil prices would test these buffers, affecting inflation, the current account, the currency, and corporate earnings.

Q3FY26 Earnings Results

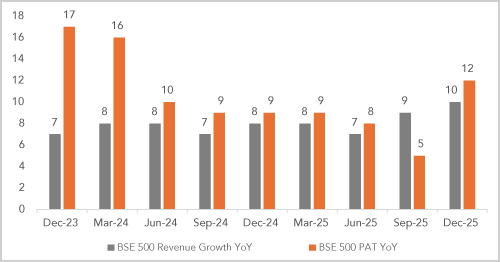

India Inc. delivered a broad-based Q3FY26 earnings recovery. Nifty 50 (ex-Tata Motors) revenues rose 12.5% YoY, an 11-quarter high, supported by festive demand, GST adjustments, strong credit offtake, and higher realizations in Materials and Energy. BSE 500 revenues grew ~10% YoY, with mid- and small-caps driving double-digit expansion and improving market breadth. Margins were slightly affected by labour-related adjustments, yet Nifty 50 aggregate PAT rose 12.8% YoY. Within the broader market, the Nifty Next 50 posted median PAT growth of 13% YoY, the Nifty Mid-cap 150 19% YoY, and the Nifty Small-cap 250 22% YoY.

Earnings growth picked up in last quarter

Source: Nuvama Research

Earnings downgrades again exceeded upgrades, though less sharply than in early 2025. Overall, consensus forecasts remain largely stable, with Nifty 500 FY26 EPS estimates were trimmed by 0.1% and FY27 upgraded by 0.7%, implying growth of 15.7% in FY27, highlighting earnings recovery in coming quarters.

Equity Outlook

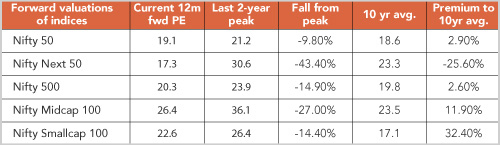

India’s economic activity and corporate earnings are beginning to rebound, as discussed earlier. Meanwhile, valuations across several segments have moderated from peak levels, with the market largely moving sideways over the past 18 months. Mid- and small-cap stocks, in particular, have seen sharper corrections at the stock level even as the broader indices have remained relatively resilient.

Foreign institutional investors (FIIs) have been net sellers in recent months, though the pace of outflows had eased by February 2026. Selling has picked up again in recent days amid escalating Middle East tensions. However, domestic institutional investors (DIIs) have more than offset these flows, reflecting the continued strength of domestic liquidity. Earlier concerns that mutual fund inflows and SIP contributions might slow as market returns moderated have not materialised; flows have remained steady and increasingly appear structural in nature.

Source: Bloomberg, Sanctum Wealth

With earnings growth improving and domestic flows resilient, our longer-term outlook on Indian equities remains constructive.

In the near term, developments in the Middle East are likely to take centre stage. As noted earlier, oil prices have a significant impact on the Indian economy, and sustained increases could raise input costs, pressure corporate margins, and delay the earnings recovery by one to two quarters, depending on the oil price trajectory. Against this backdrop, we recommend a staggered approach to equity allocation and suggest using any sharp market corrections to deploy additional capital. Investors should be prepared for relatively muted returns until geopolitical tensions ease.

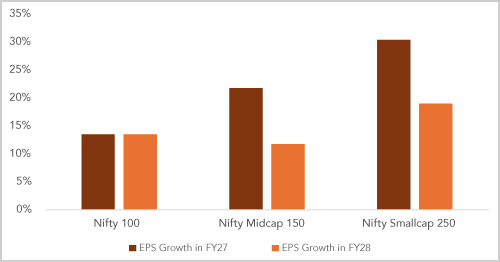

SMID earnings set to accelerate in FY27

Source: Bloomberg, Sanctum Wealth

Within equities, mid-caps are delivering stronger earnings growth and are expected to continue outperforming on this front. Valuations have also moderated meaningfully from peak levels. In small-caps, both earnings growth and valuations are far more dispersed. Based on discussions with active managers, this dispersion is creating a wider opportunity set within the segment. However, mid- and small-caps are generally more vulnerable to oil price shocks due to relatively lower pricing power and weaker balance sheets. As a result, we prefer to increase mid-cap exposure gradually.

Fixed Income Outlook

While the government’s FY27 gross borrowing plan came in higher than expected, net borrowing remains largely in line with forecasts. Additionally, budget estimates are conservative, providing some fiscal flexibility. State borrowings, however, have been rising steadily, and the RBI has managed the abundant supply through open market operations (OMOs), having absorbed nearly half of the Centre’s FY26 borrowings by February 2026.

FPIs have slowed sharply in FY26, with just USD 1.5 billion until January, compared with USD 15.6 billion in FY25. FY25 inflows were supported by index inclusion, while FY26 flows were weighed down by uncertainty around the India–US trade agreement, a narrowing yield differential, elevated global volatility, and a roughly 5% depreciation in USD–INR. With oil price concerns persisting, FPI inflows are unlikely to pick up meaningfully in the near term.

CPI inflation is expected to inch higher and hover around 4% in FY27. Hence, the RBI is likely to remain on hold. Against this backdrop, bond yields are unlikely to decline and may even rise if oil prices remain elevated. We therefore prefer to avoid duration and suggest shorter-duration positioning.

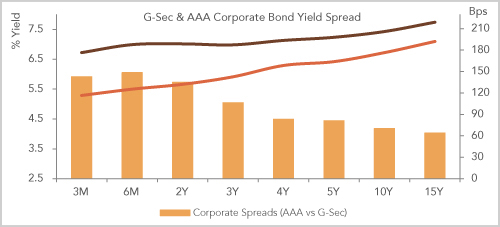

Shorter term credit spreads attractive

Source: Bloomberg, Sanctum Wealth

Corporate spreads, particularly at the shorter end of the curve, remain attractive, with the corporate yield curve flatter than the government curve. Investors may consider money market and ultra-short-term funds for horizons under one year. While the rise in STT has reduced arbitrage fund returns, they can still offer higher post-tax gains for those in the top tax bracket. Actively managed short-term and corporate bond funds may generate modest alpha amid likely volatility from Middle East developments. For tax-efficient strategies with horizons of over two years, income plus arbitrage funds remain a viable option.

Gold and Silver Outlook

Despite all the volatility, Gold had another positive month in February 2026, marking a sixth consecutive gain. However, despite escalating Iran–Israel tensions in recent days, gold prices have corrected as investors booked profits, the U.S. dollar strengthened, and market participants shifted focus to liquidity needs or alternative assets such as crude oil.

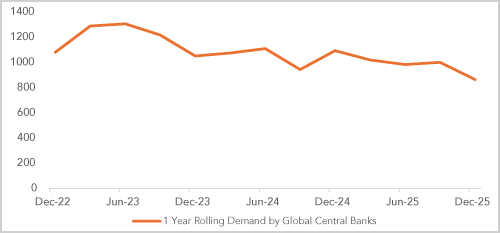

Geopolitical developments could continue to influence gold prices in the near term, as the metal remains a key safe haven during periods of heightened uncertainty and market volatility. Over the longer term, central bank demand remains supportive even at elevated price levels. However, momentum has moderated in recent months, with gold ETF flows and speculative positioning becoming a larger driver of price movements. These ETF and speculative flows can reverse quickly.

After a multi-year rally, investors should approach gold with caution, as prices are likely to remain volatile in the near term. Investors who are under-allocated may consider building exposure gradually or on price dips with a three-year-plus investment horizon. Those who are over-allocated could use sharp price spikes as opportunities to trim exposure. In our model portfolios, we plan to reduce our overweight allocation to gold.

Central bank buying has declined in last few months

Source: Word Gold Council, Bloomberg, Sanctum Wealth

The view is broadly similar for silver. However, given its sharper rally, the gold–silver ratio appears more stretched, and silver’s inherently higher volatility warrants greater caution. Accordingly, we have fully exited our silver position in the model portfolios.