Apr 7, 2026

Longer Crisis, Larger Inflation Pulse

The market still seems to think this is an oil spike with an exit ramp. We take a different view. We believe investors are underestimating the duration of the ongoing conflict in the Middle East and, therefore, its long-term inflationary impact. The initial signs of the conflict are already visible in exposed Asian economies. The United States has yet to feel the full force of the conflict, however. If the disruption persists, the issue will not be about oil alone but also about the spread of higher costs, as transport, fertiliser, and food prices soar and inflation expectations spike.

Recession? Not yet, but…

Last week’s economic data did not scream recession. It did, however, suggest that economic momentum is gradually fading in the most exposed parts of the world economy just as inflation risks begin to emerge. While that is still far from a catastrophe, it nonetheless is troublesome. Global manufacturing has lost momentum yet again, and the softening has been most visible in parts of Asia most dependent on Middle Eastern energy flows. That should not be brushed aside as statistical noise. Economic weakness rarely arrives with fanfare. It usually starts with a few hairline cracks in places under the greatest strain.

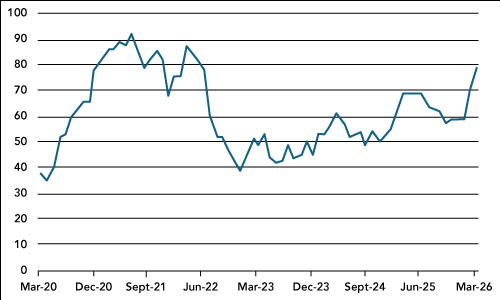

Chart 1: ISM Manufacturing Sector Prices Paid Index – Highest since COVID

Index

Source: Bloomberg

…headwinds are emerging

As we entered the first quarter, the world economy was not especially robust to begin with. Growth was respectable enough, but not so strong that it could absorb a prolonged energy and logistics disruption without consequences. What we are now observing is not a collapse, but a deterioration in the quality of growth. It is becoming less widespread, and more prone to inflation. Markets are still behaving as though time is on their side. We believe the opposite. Time is the issue here.

The real question is not whether oil prices will rise. They already have. The real question is how long the secondary effects will persist. Airlines are beginning to tell us what lies ahead. Vietnam Airlines is cutting flights. Ryanair is openly considering summer cancellations. Korean Air has moved into emergency mode. When airlines begin trimming schedules, the issue is not merely that fuel is expensive. It reflects a far deeper anomaly – one where the smooth functioning of the modern economy itself becomes harder to guarantee. Markets should pay more attention when the real world starts cancelling take-offs.

Governments to the rescue…

Governments are moving quickly to soften the price shock through tax cuts, subsidies, and emergency support, but these are temporary measures and do not create new supply. Spain, for instance, has approved a €5 billion emergency package, including lower electricity VAT and support for agriculture and transport fuels. Thailand is recalculating refining and marketing costs and considering tax cuts to manage prices, while also freezing cooking-gas prices. The Philippines has declared a national energy emergency and activated a 20 billion peso fund to boost fuel security. Yet, at the same time, rationing is already under way. Myanmar has imposed odd-even driving days for private vehicles. Government offices in Pakistan have shifted to a four-day week, reducing vehicle use. Sri Lanka has tightened fuel rationing, imposed odd-even access, and even made Wednesdays a public holiday to curb demand. Bangladesh has shortened office hours, limited fuel-station operations, and is effectively rationing supply through restricted access. While these measures can subsidise the pain, they cannot subsidise physical scarcity out of existence.

…but those measures may not be enough

The impact of the rise in oil prices is only one dimension of the future inflation pulse. The impact on agriculture may prove even more damaging because the economic effects arrive later and are therefore easier to ignore initially. Around a third of the global seaborne fertiliser trade normally moves through Hormuz. India, for instance, has built a partial cushion, with current fertiliser inventories of about 18 million tonnes, up from 14.7 million tonnes a year ago, but against an estimated summer demand of 39 million tonnes. That is protection, not immunity. A missed fertiliser window is not repaired by paying more a few weeks later. If disruption persists, farmers cut application rates, alter planting decisions, or accept weaker yields. That is how an energy shock quietly turns into a food inflation shock. The supply curve, to put it plainly, is hobbled. Higher prices do not suddenly create new shipping routes, more gas feedstock, or instant export availability.

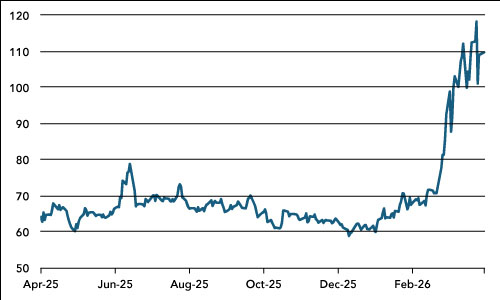

Chart 2: Brent Oil Price ($bbl)

Source: Bloomberg

The United States has yet to see any major economic damage, and that is encouraging as far as it goes. Growth still looks reasonably firm, business investment has not fallen apart, and the consumer has not yet retreated in any meaningful way. The forward view is less comfortable, however. The next phase is likely to be characterised by softer growth and firmer inflation – a combination that markets keep trying to wave away. It would not be outlandish to expect a roughly one percentage point rise in US headline inflation if the energy and logistics disruption persists. Temporary shocks tend to become persistent once they move through transport, food, and expectations.

Outside the United States, the policy dilemma is sharper still. Central banks are being forced into an uncomfortable choice – tighten policy against a supply shock and risk looking performatively hawkish while growth weakens; sit still and risk being accused of complacency as inflation rises. Neither option is attractive. That is why the coming months may produce one of the more awkward backdrops for markets: slower growth, firmer inflation, and a monetary response that is fragmented rather than coherent. Investors have spent years assuming that central banks, when in doubt, would rescue sentiment. They may find this time that central banks are just as confused and compromised as everyone else.

Then there is Washington. The proposed FY2027 budget matters less as an accounting exercise and more as a statement of intent. Defence spending is set to rise to roughly $1.5 trillion in FY2027, up from about $1 trillion in 2026, while non-defence discretionary spending is reduced by $73 billion. A government asking for the largest increase in defence budget in decades is not one confidently betting on imminent calm. That does not make escalation inevitable, but it does make the market’s assumption of a quick geopolitical off-ramp look rather too far-fetched. The peace dividend from the 1990s is officially dead. We have not reversed every gain since the fall of the Berlin Wall, but we have reversed the direction of travel. The assumptions of the post-Cold War era — peace dividends, economic integration, and a steady broadening of the liberal order — are being dismantled in front of us.

India offers a useful window into how these shocks tend to unfold. High-frequency indicators are already hinting at a loss of momentum — surveys have softened, credit growth has eased, and travel demand has cooled. Yet, the inflationary hit from higher fuel costs has not fully landed at the household level. That means the first phase is softer activity, while the second – and more worrying – phase is higher living costs. Growth weakens first, inflation arrives afterwards, and policymakers are left trying to explain why both are true at once. Markets, which prefer tidy narratives, tend to dislike that sort of untidiness.

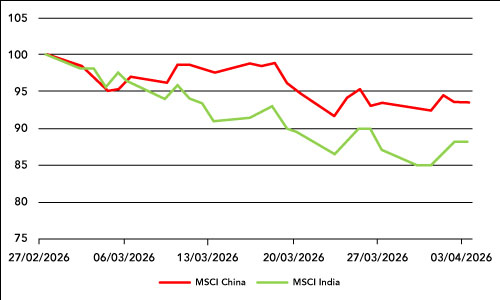

China, meanwhile, looks more resilient, though not in a way that can necessarily cure the ills of the region. As the crisis has unfolded, Beijing’s instinct has been defensive, not generous. It is seeking to protect domestic supply, keep refinery throughput up, and avoid importing instability into its own systems. While that is sensible for China, it is less helpful for everyone else. A self-protective China is not a regional stabiliser.

Chart 3: MSCI China Equity Index (TR USD) and MSCI India Equity Index (TR USD)

rebased to 2th February=100

Source: Bloomberg

Q1 earnings season offers a clear picture of relative resilience. S&P 500 earnings are expected to grow roughly 14% year on year, with technology, energy, and defence doing much of the heavy lifting. Europe looks far more dependent on energy windfalls than broad corporate strength, and Asia is sharply split between semiconductor winners and energy-sensitive losers. Capital flows are telling a similar story: not outright flight from Europe, but growing wariness about owning European duration and the euro, while investors gravitate toward the earnings depth and liquidity the United States still offers.

In summary, investors are still fixated on the price of oil when they should rather be debating the duration of the shock. Duration is what turns an energy scare into an inflation regime. Last week’s data do not justify a global recession call, but they do suggest that the shock is beginning to migrate from markets into activity — and that the migration is still in its early stages.

When governments start counting driving days and shortening working weeks to ration fuel, the shock is no longer a market event. It is a social one. Duration is the variable that investors keep underpricing. That is the mistake.