Mar 6, 2026

Global Economy

Economic data released during February suggested that the global economy continues to expand, though the momentum remains uneven across major regions. Activity indicators show a world that is neither accelerating strongly nor slipping into recession, but rather moving through a phase of modest and differentiated growth.

In the United States, economic signals remain broadly resilient. Business activity surveys continue to point to expansion, supported by a still-robust labour market and steady consumer spending. The manufacturing sector has shown tentative improvement after a softer period last year, while services activity remains the principal driver of growth. Financial conditions have eased slightly as bond yields stabilised, helping maintain confidence in the “soft landing” narrative, although inflation persistence continues to keep the Federal Reserve cautious.

Europe’s economic picture is more fragile, though signs of stabilisation have emerged. Manufacturing activity remains subdued, reflecting weak external demand and the lingering effects of tighter financial conditions over the past two years. However, sentiment surveys suggest the pace of contraction is easing and services demand has held up better than expected. Fiscal policy discussions across the region, particularly around investment and defence spending, may provide a modest tailwind later in the year.

Japan’s economy has shown renewed momentum, supported by domestic demand and the gradual normalisation of corporate and wage dynamics. Structural reforms and a shift in corporate governance continue to support business confidence. At the same time, currency fluctuations and the evolving stance of the Bank of Japan remain key influences on the outlook.

Across emerging markets, growth remains comparatively strong. Several countries benefit from improving trade flows, stabilising inflation and earlier monetary tightening cycles that now provide room for policy flexibility. Asia in particular continues to act as a key engine of global growth.

Taken together, February’s data portray a global economy that is proving more resilient than many had expected a year ago. Growth is not synchronised, but it remains intact, with the United States providing stability, Asia delivering momentum and Europe gradually attempting to regain its footing.

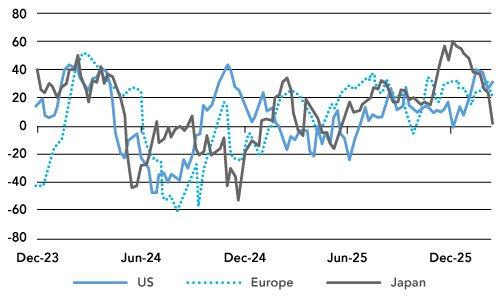

Chart 1: Global Economic Surprise Indices – Inflation and Growth

Index

Source: Bloomberg

Asset Markets

Equities

Equity markets are not surging; they are evolving. The more interesting development this month has been the quiet redistribution of leadership. For much of the past decade, US mega-cap technology set the pace. That dominance is softening at the margin. US equities however made a decent 5.2% for the month with a very late surge.

Japan +7.9% in local currency terms remains one of the most compelling structural stories. Corporate governance reform, balance sheet discipline and a generational shift in policy thinking continue to re-rate the market. Currency volatility has diluted some of the return for dollar investors, yet that itself is a signal: Japan is no longer passively accepting currency weakness as policy orthodoxy.

Within the US, the participation of smaller companies is noteworthy. The Russell 2000’s relative resilience hints at improving domestic breadth (+5.5%) a modest outperformance in the event although they spent the month with a wider margin of performance. Technology still leads, but the outperformance gap has narrowed. Banks and healthcare are contributing; consumer defensives are marking time. Markets appeared to be transitioning from a liquidity-led rally to one that is more earnings-discriminating.

Japan – good news

Japanese equities delivered one of the stronger performances among developed markets during February, reflecting continued optimism around corporate reform and improving domestic fundamentals. The Tokyo market has benefited from a combination of factors: stronger shareholder discipline, rising wages supporting domestic demand, and a steady reallocation of global capital into Japanese equities after years of underweight positioning. Corporate governance reforms and balance sheet efficiency continue to underpin investor confidence. Currency movements, however, moderated some of the gains for international investors, reminding markets that the yen remains an important driver of USD-based returns.

Europe.

European equities recorded a more modest performance during the month. Markets continue to navigate a fragile economic backdrop characterised by subdued manufacturing activity and cautious business sentiment. That said, the region has benefited from stabilising inflation and the prospect of fiscal support through investment and defence spending initiatives. Investors remain selective, favouring companies with global revenue exposure and strong pricing power. Europe’s equity market therefore appears steady rather than dynamic, supported by valuation appeal but still waiting for clearer evidence of a stronger economic recovery.

Emerging-market equities

India was more measured. Returns were positive but restrained. After a prolonged period of strong outperformance and elevated valuations, February felt more like consolidation than acceleration. Foreign investor flows have shown tentative improvement, yet investors remain valuation-sensitive.

Brazil and parts of Latin America lagged. Performance was modest despite supportive real yield dynamics. Political uncertainty and questions around fiscal discipline continue to temper enthusiasm, even where monetary policy credibility has improved.

Asia is asserting itself. China’s rebound is no longer purely speculative positioning; it reflects policy calibration, incremental fiscal support and, crucially, valuations that had priced in deep pessimism. Asia ex Japan has moved with purpose, suggesting that capital is again willing to differentiate within emerging markets rather than treat them as a homogeneous risk trade.

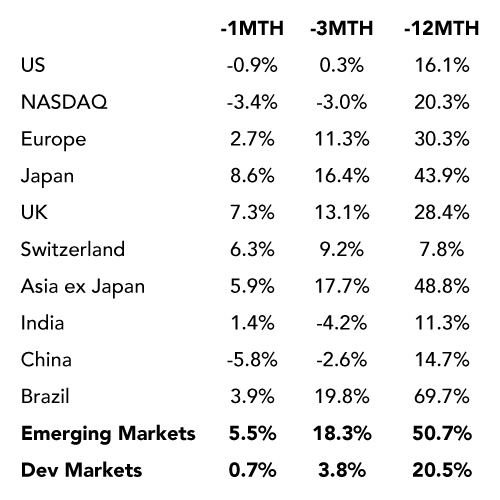

Table 1: Equity Market total returns as at February 2026

Source: Bloomberg

Equities- Sectors

Sector performance in February highlighted a clear rotation in market leadership. For much of the past year, technology dominated returns, but the most recent month suggests investors are reassessing where earnings resilience and pricing power lie in a world still shaped by inflation, fiscal expansion and geopolitical uncertainty.

Energy was the standout performer, rising sharply during the month and extending a powerful longer-term trend. Strength in oil and gas prices, combined with disciplined capital spending and shareholder-friendly policies among producers, continues to underpin the sector. The sector also benefits from geopolitical tension, which tends to place a premium on energy security and supply resilience.

Consumer staples also delivered a strong February, reflecting a shift toward defensive earnings. In periods where macro uncertainty increases, investors often return to companies with stable demand profiles and pricing power.

Healthcare recorded a more modest advance, continuing a steady but unspectacular recovery. The sector has benefited from its defensive characteristics and from innovation in biotechnology and pharmaceuticals, yet valuations remain sensitive to regulatory debates and the broader direction of healthcare spending in major economies.

Banks were broadly flat during the month, though the longer-term performance remains striking. Over the past year, financial institutions have been among the best-performing sectors globally. Higher interest rates have supported net interest margins, while credit conditions have so far remained relatively stable. The pause in February likely reflects consolidation after a strong run rather than a fundamental shift in sentiment.

In contrast, technology experienced a notable pullback during the month, following an extended period of leadership. The sector’s longer-term gains remain impressive, but the February decline suggests some profit-taking and valuation sensitivity after a powerful rally driven by enthusiasm around artificial intelligence and digital infrastructure.

Consumer discretionary stocks also weakened, reflecting the market’s sensitivity to the outlook for household spending. With interest rates still relatively elevated and real income growth uneven across economies, investors appear cautious about sectors most exposed to discretionary consumption.

Taken together, February’s sector performance tells a broader story. Investors are not abandoning technology, but they are redistributing exposure toward sectors linked to real assets, pricing power and defensive earnings. Energy and consumer staples leading the month while technology and discretionary lag is a classic signal of a market broadening beyond a single narrative.

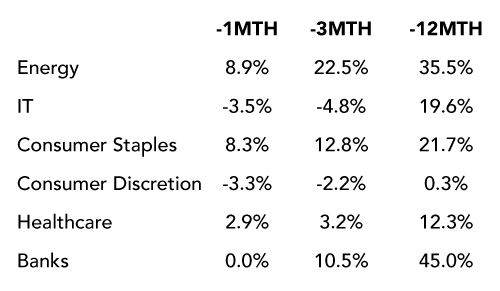

Table 2: Global equity sector total returns in February 2026

Source: Bloomberg

Bond markets

Bond markets delivered a constructive, if somewhat nuanced, performance in February. After a prolonged period in which higher interest rates weighed heavily on duration assets, the month provided some relief as yields stabilised and investors began to reassess the balance between inflation risk and economic resilience.

Core global bonds posted a solid gain for the month, with the global aggregate index advancing as yields eased modestly across several major markets. The move reflects a gradual recalibration of expectations around monetary policy. While central banks remain cautious about declaring victory over inflation, the absence of renewed price shocks has allowed investors to re-enter duration selectively.

US investment grade credit also performed well, continuing to benefit from stable corporate balance sheets and resilient economic activity. Spreads remain relatively contained, reflecting confidence that large corporations are well positioned to navigate a higher-for-longer rate environment. Over the past year, investment grade bonds have delivered respectable returns, supported both by income and by the gradual stabilisation of long-term yields.

Emerging market debt remains one of the stronger performers over a longer horizon. Several emerging economies moved earlier in tightening monetary policy cycles, leaving real yields comparatively attractive. That policy credibility has supported capital flows into both local and hard-currency EM debt. The asset class has therefore been able to deliver solid returns over the past twelve months despite periodic bouts of dollar strength.

High yield credit was comparatively subdued in February. After a strong period of spread compression over the past year, the sector paused as investors became slightly more selective. The relatively modest monthly gain reflects a market that is no longer pricing an imminent recession but is also unwilling to chase risk aggressively after the strong performance already achieved.

Taken together, February suggests that fixed income markets are gradually finding their footing after several turbulent years. Income is once again a meaningful component of total return, and the dispersion between government bonds, investment grade credit and higher-yielding segments reflects a market increasingly comfortable with moderate growth but still alert to inflation risks.

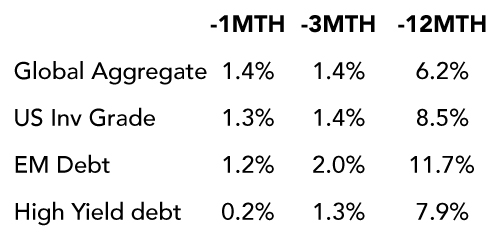

Table 3: Bond Market Total Returns for February 2026

Source: Bloomberg

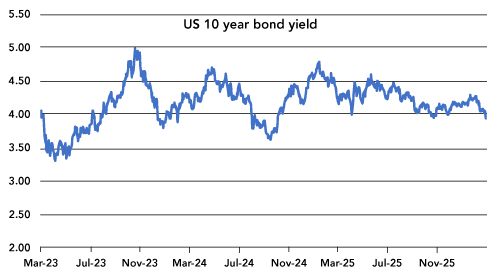

Chart 2: US 10-year yield back to the low end of the recent range

Source: Bloomberg

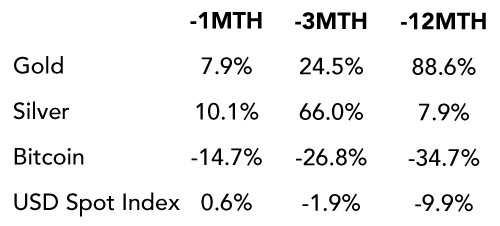

FX and Precious metals

February delivered a striking divergence within the universe of alternative stores of value. Precious metals surged, the US dollar stabilised modestly, while cryptocurrencies experienced a sharp retrenchment. The pattern says much about how investors are currently assessing geopolitical risk, inflation uncertainty and financial stability.

Gold recorded a powerful advance during the month, extending an already exceptional twelve-month rally. The metal continues to benefit from a combination of forces rarely aligned so clearly at the same time: geopolitical tensions, persistent fiscal expansion in major economies and a gradual erosion of confidence in government bonds as a traditional “risk-free” anchor. Central bank buying has also remained a powerful structural driver, particularly from emerging market reserve managers seeking to diversify away from the US dollar. When gold rises strongly even as the dollar stabilises, it often signals strategic rather than purely tactical demand.

Silver moved even more dramatically. The metal’s surge reflects both its precious metal characteristics and its role as an industrial input. Demand linked to electrification, renewable energy and advanced electronics has tightened the supply-demand balance. Silver therefore behaves partly as a macro hedge and partly as a beneficiary of the global technology and energy transition. The strength over recent months highlights how quickly sentiment can shift in markets where supply growth has been constrained for years.

Table 4: Precious metals and FX

Source: Bloomberg

Bitcoin, by contrast, suffered a sharp correction. The decline over the month and the broader three-month horizon suggests that the digital asset complex remains sensitive to liquidity conditions and investor risk appetite. Periods of heightened geopolitical tension and market uncertainty often favour tangible safe-haven assets such as gold rather than highly volatile digital alternatives. February’s performance reinforces the distinction between speculative risk assets and established stores of value.

The US dollar strengthened modestly during the month, though the broader trend over longer horizons remains weaker. The modest rise reflects short-term safe-haven flows and the relative resilience of the US economy compared with other developed markets. However, the longer-term decline in the dollar index points to deeper structural themes: expanding US fiscal deficits, the gradual diversification of global reserves, and the increasing willingness of some economies to transact outside the traditional dollar system.

Taken together, February’s moves underline a broader shift in investor psychology. In an era characterised by geopolitical fragmentation, large fiscal deficits and technological transformation, investors are rediscovering the value of tangible assets and strategic hedges. Precious metals have therefore become more than a crisis trade; they are increasingly being treated as a core component of long-term portfolio diversification.