Jun 10, 2026

• A Middle East deal appears within reach but remains uncertain.

• Global equity momentum increasingly depends on earnings growth, led by AI infrastructure spending.

• India’s macroeconomic resilience continues, though higher energy costs have yet to be fully passed through to consumer prices.

• Q4FY26 earnings were broadly strong, with mid- and small-caps outperforming large-caps.

• We remain cautiously optimistic on Indian equities, supported by resilient growth, earnings recovery, and better valuations, while monitoring Middle East risks.

Deal or No Deal

Over the past few weeks, an interim agreement between the US and Iran has appeared increasingly likely, yet a durable resolution remains elusive. While the ceasefire has broadly held, the Strait of Hormuz continues to represent a key source of uncertainty and potential volatility. Despite these geopolitical risks, markets have largely shifted their focus back to earnings. With inflationary pressures re-emerging and growth moderating, earnings growth has become the primary driver of market performance, increasingly supported by the ongoing AI infrastructure buildout.

In India, economic activity remains resilient and Q4FY26 earnings exceeded expectations. Inflation has remained relatively contained due to limited pass-through of higher energy prices, while strong domestic flows continue to offset foreign investor outflows.

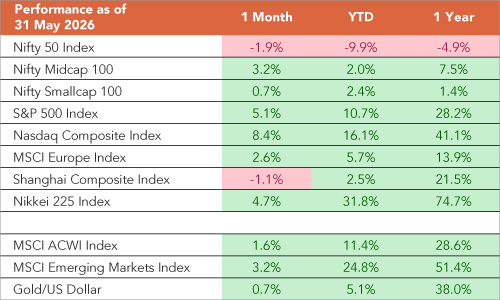

Source: Bloomberg, Sanctum Wealth

Above returns are only price change in local currency terms and not total returns

Global Market Update

As we write, the Nasdaq has fallen 4% on 5 June 2026 as investors reassess the prospect of US interest rates remaining higher for longer. The sell-off was triggered by a much stronger-than-expected jobs report, with the US economy adding 172,000 jobs in May after an upwardly revised 179,000 in April, well ahead of expectations of 80,000–85,000. At the same time, inflationary pressures are re-emerging. Headline PCE inflation accelerated to 3.8% year-on-year in April from 3.5% in March, while core PCE remained elevated at 3.3%. The combination of sticky inflation and a resilient labour market have shifted market expectations. The Fed funds futures are now pricing in nearly a 70% probability of at least one rate hike by year-end, up from around 50% before the jobs report.

Inflationary pressures visible in the U.S.

Source: Bloomberg, Sanctum Wealth

As long as the labour market remains resilient, the Fed is likely to prioritise inflation control over growth. With rates expected to remain higher for longer, the valuations of technology companies and the sustainability of the AI-led capex cycle are likely to come under increasing scrutiny.

Meanwhile, the AI infrastructure buildout has become the dominant driver of global earnings growth, particularly in the US and in some parts of Asia like South Korea, Japan, Taiwan and China. Semiconductors, power equipment and related infrastructure businesses continue to report exceptional results as demand for compute capacity remains significantly ahead of supply. Much of the earnings growth is currently being driven by strong pricing power and operating leverage rather than volume expansion alone, highlighting the scarcity value of advanced compute.

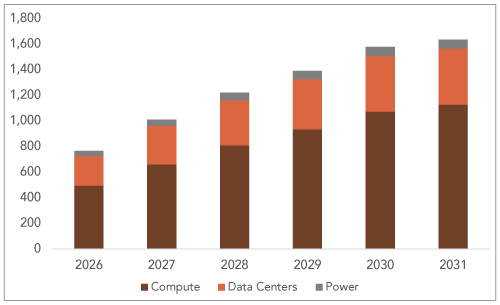

Baseline aggregate AI capex estimates (in USD bn)

Source: Bloomberg, Sanctum Wealth

Goldman Sachs Global Investment Research NVIDIA projections as of March 3, 2026

The investment cycle is being led by Hyperscalers and AI model developers whose unprecedented capital expenditure plans are cascading through the broader industrial ecosystem. What began as a technology investment cycle has increasingly evolved into a wider industrial capex cycle, supporting demand across power equipment, electrical infrastructure, wires and cables, cooling systems, specialty chemicals and data-centre construction.F

Defence is emerging as another powerful earnings driver. Governments across the world are increasing spending to build indigenous capabilities as geopolitical tensions rise and the post-Cold War global order continues to fragment. The combination of higher defence budgets, localisation initiatives and long procurement cycles is creating a favourable backdrop for sustained earnings growth across the sector.

In contrast, sectors exposed to the consumer remain under pressure. Higher inflation and elevated interest rates are weighing on discretionary spending, while rate-sensitive segments such as housing, automobiles and consumer durables continue to face a more challenging demand environment. The result is an increasingly bifurcated earnings landscape, with capital expenditure-led sectors driving growth while large parts of the consumer economy struggle to keep pace. As a result, the durability of AI-led investment spending remains a key determinant of global earnings and equity market performance.

Deep Dive: Emerging Markets

After more than a decade of underperformance relative to developed markets, particularly US equities, emerging markets have staged a remarkable comeback. Having outperformed most major markets in 2025, the momentum has accelerated further in 2026, with emerging market equities rising nearly 25% Yp and over 50% over the past one year.

What makes this rally particularly noteworthy is that valuations remain far from stretched. The MSCI Emerging Markets Index continues to trade at a forward P/E of roughly 13.0x, a substantial discount to MSCI World’s 20.6x. Strong earnings growth, attractive starting valuations and a stable US dollar have together created a favourable backdrop for the asset class. We highlighted the opportunity in emerging markets in 2024, when investor sentiment was pessimistic, and the subsequent performance has reinforced the case for maintaining strategic exposure.

Relative Valuations Favor Emerging Markets

Source: Bloomberg, Sanctum Wealth

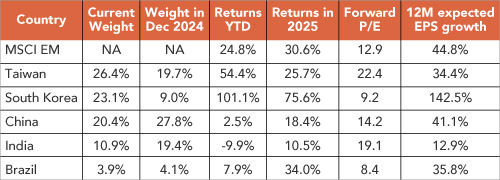

However, today’s emerging markets look very different from those of a decade ago. The composition of the index has shifted dramatically, both geographically and sectorally. Taiwan and South Korea have emerged as the largest country weights, while semiconductors and AI-related technology have become increasingly dominant. TSMC, Samsung Electronics and SK Hynix alone now account for nearly a quarter of the MSCI Emerging Markets Index.

Source: Bloomberg, Sanctum Wealth

South Korea’s KOSPI has surged more than 100% this year, hitting fresh highs, while Taiwan’s TAIEX has also repeatedly posted new records as investors piled into the semiconductor trade at the centre of the AI boom. The Korean rally, notably, is broader than just chips. Investors are also allocating to shipbuilding, defence, power equipment and even the K-culture trade, making the rally more reflective of Korea’s wider industrial base.

China led the initial phase of the EM recovery in 2025 as policy stimulus and improving technology sector sentiment drove a sharp re-rating. Between January and October 2025, foreign investors poured $50.6 billion into Chinese and Hong Kong equities, up from just $11.4 billion over the same period in 2024, according to IIF data. However, the enthusiasm has moderated. Domestic demand remains weak, the property sector continues to adjust, and deflationary pressures persist. While China has established leadership positions in EV, clean energy and AI adoption, investors have become more selective. China today looks more compelling as a targeted technology and advanced manufacturing opportunity than as a broad domestic recovery story just yet.

Elsewhere, performance has been more mixed. Brazil initially benefited from the commodity cycle and rallied more than 35%+ in 2025 but has recently faced headwinds from rising political uncertainty and trade tensions. India, which was among the strongest-performing emerging markets through 2024, has underperformed since late 2024 as elevated valuations, moderating earnings growth and higher energy prices weighed on investor sentiment. Foreign investors have withdrawn more than USD 58 billion since the September 2024 peak, resulting in Indian equities lagging the MSCI Emerging Markets Index by almost 60% in USD terms.

Source: Bloomberg, Sanctum Wealth

Returns are local currency price returns

Unlike previous emerging-market cycles that were driven by commodities, dollar liquidity or synchronised global growth, the current rally has been concentrated in markets linked to the AI and semiconductor supply chain. Taiwan and South Korea have been the primary beneficiaries, while countries without significant exposure to these themes have relied more heavily on domestic growth and reform narratives to attract capital. Given the strength of the recent rally in EM, some moderation in returns should be expected, even if earnings growth remains robust.

India Macro Update

High-frequency indicators continue to point to resilient domestic economic activity despite the ongoing conflict. GST e-way bills grew 11.8% in April, toll collections rose 12.6% in May and GST revenues increased 8.7%, indicating healthy underlying activity. Services and manufacturing PMIs remained firmly in expansion territory at 59.8 and 55.0, respectively. Demand conditions also remain supportive, with strong growth in two-wheeler and tractor sales and resilient merchandise and services exports. Overall, the economy has weathered the immediate spillover effects of the conflict reasonably well, although cost pressures are beginning to emerge.

Looking ahead, higher energy prices and supply chain disruptions are likely to weigh on growth, with the extent of the impact dependent on the duration of the conflict and the pace of normalisation. A below-normal monsoon forecast, at 90% of the long-term average, adds another layer of uncertainty by posing risks to agricultural output, rural demand and inflation. While urban consumption should remain supported by resilient services activity and stable employment conditions, growth could soften in the coming months if supply disruptions persist.

Inflation, meanwhile, is beginning to trend higher, although consumer price pressures remain manageable for now. CPI inflation stood at 3.5% in April, reflecting the limited pass-through of higher energy costs to consumers. In contrast, WPI inflation accelerated sharply to 8.3% as rising energy and input costs fed through to producer prices. With the pass-through to retail prices now gradually underway, CPI inflation is likely to move higher and could approach the upper end of the RBI’s tolerance band over the coming quarters.

Pass through of higher energy price to CPI has just begun

Source: Bloomberg, Sanctum Wealth

Reflecting these risks, the RBI has revised its FY27 inflation forecast upward to 5.1% from 4.6% and lowered its growth forecast to 6.6% from 6.9%. As expected, the central bank kept rates unchanged, while acknowledging both upside risks to inflation and downside risks to growth. We expect the RBI to remain largely data-dependent and maintain a wait-and-watch stance, unless the conflict becomes prolonged or inflationary pressures intensify materially.

The INR was a key focus of the latest policy measures, with both the government and the RBI announcing a series of steps to attract foreign capital. These included tax incentives for foreign investors in government bonds, broader eligibility for global bond index inclusion and measures to lower hedging costs on foreign currency inflows. Collectively, the initiatives could help bridge a significant portion of India’s FY27 balance of payments gap and were well received by currency markets. With policy support now in place and the INR appearing significantly undervalued on a real effective exchange rate basis, we believe the risk of further meaningful depreciation has reduced.

INR one of the worst performing EM currencies in last 12 months

Source: Bloomberg, Sanctum Wealth

Q4FY26 Earnings Results

Q4FY26 earnings concluded on a stronger-than-expected note, with broad-based outperformance across sectors. For the BSE 500 (excluding OMCs), revenue growth accelerated to 13% YoY, the strongest pace in three years, supported by higher commodity prices, a weaker rupee and the impact of tax cuts. Top line growth is now showing signs of recovery after multiple quarters of single digit growth. EBIpA growth remained relatively muted at 7%, reflecting margin pressures amid higher input costs, while PAT growth held steady at 12%.

The earnings surprise was led by BFSI, metals, OMCs, automobiles, telecom and technology, while the oil and gas sector remained a drag on aggregate profitability. Despite the stronger quarter, the Nifty delivered its eighth consecutive quarter of single-digit earnings growth, highlighting the uneven nature of the recovery. Broader large-cap earnings were relatively stronger. While revenue growth across mid-caps and small-caps was only modestly higher than that of large-caps, profit growth was significantly stronger in Q4FY26, driven by operating leverage and margin expansion.

For FY26 as a whole, Nifty 50 earnings grew by just 5%, marking a second consecutive year of single-digit growth. In contrast, earnings growth broadened beyond the benchmark index, with the Nifty Next 50 delivering a stronger performance, mid-caps reporting earnings growth of over 20%, and small-caps growing by around 12%, comfortably outperforming their large-cap peers.

India Inc.’s earnings are recovering

Source: Amsec

The beat-to-miss ratio remained favourable, with nearly half of companies reporting earnings above expectations, while only about one-third missed PAT estimates. However, the upgrade-to-downgrade ratio remained broadly balanced for a second consecutive quarter. As a result, FY27 EPS estimates were trimmed by around 1% at the aggregate level, with slightly steeper cuts of 2–3% for mid- and small-caps.

Despite these revisions, earnings growth is expected to accelerate meaningfully in FY27. BSE 500 earnings are projected to grow by 19%, while Nifty earnings are expected to rise by around 15%. Earnings momentum is likely to remain strongest in the broader market, with mid-cap and small-cap earnings growth estimated at 20% and 30%, respectively.

The full impact of higher energy prices haven’t yet been seen in earnings amid limited pass through and only one month in the quarter being impacted. The full impact of higher energy prices has yet to be reflected in earnings given limited pass-through and only one month of disruption affecting Q4FY26. Management commentary remains cautiously optimistic on a second-half recovery, with the consensus view that higher crude prices are a manageable headwind unless the conflict becomes prolonged or results in a sustained disruption to energy supplies.

Equity Outlook

Indian equities delivered a mixed performance over the past month. While large-caps corrected, mid- and small-caps continued to advance, supported by stronger earnings growth. Mid-caps were the standout performers, while the Nifty Next 50 has also distinguished itself this year, outperforming the Nifty 50 by more than 12.5%. The underperformance of the Nifty has been driven largely by its two heavyweight sectors, banks and IT. While banking sector earnings remained healthy, the segment has been weighed down by persistent foreign investor selling. IT, meanwhile, faces a more structural challenge as investors reassess the long-term implications of AI on traditional outsourcing and technology services business models.

Source: Bloomberg, Sanctum Wealth

Above returns are only price change and not total returns

Looking ahead, improving earnings growth, more reasonable valuations and continued domestic inflows provide a supportive backdrop for Indian equities. While foreign investor sentiment remains weak, India’s prolonged underperformance relative to broader emerging markets and the correction in several segments of the market suggest that a meaningful portion of the current macro and geopolitical uncertainty is already reflected in prices to some extent. India also serves as a defensive market in the event of a reversal in the AI-driven rally.

We therefore remain overweight equities, particularly mid- and small-caps where earnings growth remains stronger. While the Middle East conflict could continue to create near-term volatility, any further correction would provide an opportunity to increase exposure. Conversely, a de-escalation of the conflict could improve sentiment and support a recovery in markets. Waiting for complete clarity before investing may result in missing the opportunity altogether.

Fixed Income Outlook

Ahead of the RBI policy, markets had begun to worry that pressure on the INR and India’s balance of payments could force the central bank to raise rates despite a slowing growth outlook. Instead, the RBI kept rates unchanged and announced a series of measures to support the currency, easing these concerns and helping bond yields decline.

Although inflation risks remain elevated, much of the potential policy tightening appears already reflected in bond yields. The spread between the repo rate and the 10-year government bond yield is currently around 170 bps, well above the historical average of 100 bps.

Widening repo–G-Sec spread suggests

markets are pricing in some future rate hikes

Source: Amsec

As a result, current bond yields appear attractive and could moderate if energy prices ease, geopolitical tensions subside or foreign flows improve. However, the risk-reward in taking significant duration exposure remains less compelling. We continue to prefer corporate bond and short-duration funds, which can benefit from attractive accrual yields without assuming excessive interest-rate risk. For investors with shorter investment horizons, money market funds remain the preferred option.

As mentioned in our last monthly note, we have exited our REIT and InvIT exposure across managed portfolios. While REITs can provide attractive inflation protection over the long term, they tend to be vulnerable in a rising interest rate environment. Rental and concession revenues adjust to inflation with a lag, while higher borrowing costs can pressure cash flows and valuations, particularly since most of them have leveraged balance sheets. In addition, rising bond yields reduce the relative attractiveness of their distribution yields.

Given the current environment, we believe the risk-reward is more favourable in alternative income-oriented strategies such as Income Plus Arbitrage Funds and Unifi DAAF, which offer comparable return potential with greater stability and tax efficiency. REITs and InvITs continue to merit a strategic allocation over the long term, but tactically we expect them to face headwinds and potentially underperform.

Gold and Silver Outlook

While gold has underperformed in US dollar terms recently, INR depreciation and higher customs duties have helped domestic gold prices remain resilient. As a result, gold has continued to deliver positive returns over the past month and is up nearly 15% year-to-date in INR terms.

Near-term returns, however, could be more muted. Rising inflation and higher interest rates globally increase the opportunity cost of holding non-yielding assets such as gold. At the same time, elevated prices have dampened jewellery demand, while higher margins have encouraged increased mine production and recycling supply.

That said, the long-term investment case for gold remains intact. Geopolitical uncertainty continues to support safe-haven demand, while central banks remain significant buyers as they diversify reserve assets. Although the pace of de-dollarisation has moderated, the broader trend remains supportive for gold over time. As such, we continue to view gold as an important portfolio diversifier that merits a strategic allocation, even if near-term returns are likely to be less compelling than those seen in recent years.