May 12, 2026

Oil, AI, and the inflation regime equities have not yet discounted

It is not too difficult to conclude what is driving market performance even as conditions remain unfavourable. A 60% surge in technology earnings in Q1 2026 – the rest of the S&P 500 grew at 17% – has helped the market hold its nerve. What may complicate it, however, is the story accumulating in the oil inventory data.

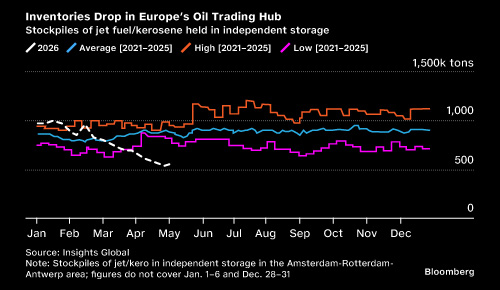

The most recent US Energy Information Administration (EIA) report showed US commercial crude stocks were down 2.3 million barrels in the week to 1 May; gasoline was down 2.5 million barrels; distillates were down 1.3 million barrels; and total petroleum stocks were down 5.9 million barrels during this period. A Bloomberg report states that inventories have fallen at their fastest pace since 1 March. The Strait of Hormuz remains largely closed. Brent settled around $101 after a renewed US–Iran exchange, having dropped $9 earlier in the week on ceasefire reports before spiking again. One hundred dollars a barrel is still a large shock relative to the pre-war baseline. Each pause in military hostilities is being priced as though it restores the physical cushion. It does not.

Chart 1: Current Path of Oil Inventories Way Below Historic Norms

Source: Bloomberg

Investors are also hopeful that the current administration will manage to resolve the conflict quickly. While that optionality keeps investors engaged beyond what the data alone might justify, it does not change the inventory position.

AI as a near-term inflationary demand shock

The consensus view is that AI is medium-term disinflationary: software compresses marginal costs, automation lifts productivity, and unit labour costs fall. That may prove true. The current build-out does not resemble a software cycle. It requires land, chips, power, cooling systems, gas turbines, transmission lines, engineering labour, copper, and concrete. Goldman Sachs has identified three near-term inflationary channels: higher computing component costs, AI-linked software price increases, and rising electricity bills as data-centre load strains power grids. The IEA’s base-case scenario expects global data-centre electricity consumption to double by 2030, reaching approximately 945 terawatt-hours. The EIA projects US power demand to rise to 4,381 billion kWh in 2027 from 4,195 billion kWh in 2025. Average US residential electricity prices are forecast to rise 5.1% in 2026 before inflation.

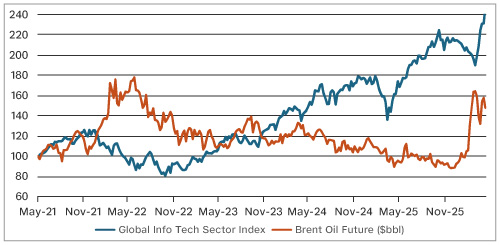

The AI build-out adds demand now. Productivity arrives later. A trillion-dollar-plus investment cycle competing for power, engineering labour, grid capacity, and financing does not take pressure off the bond market when oil is at $100. It adds to it. The market is capitalising AI as asset-light software. The cost curve is not.

Chart 2: Brent Oil Price Now Positively Correlated with the Tech Index

Source: Bloomberg

Inflation: Composition matters as much as the headline

Tuesday’s US CPI is the week’s key number. Consensus expects the April headline number to increase +0.6% month on month and core to grow +0.4%; PPI consensus is +0.4%. The Cleveland Fed nowcast was tracking headline at 0.45% and core at 0.21%, a material divergence from sell-side estimates. UBS projects April headline CPI at 4.3% year on year, up from 2.4% in February, with three-month annualised headline potentially at 8.5%. The risk is to the upside. Gasoline, airfares, shelter, motor insurance, core goods, and tariff-sensitive categories are the ones to watch out for. A single high print is containable. A sequence that shifts expectations is not.

Chart 3: US Inflation Steadily Higher

Source: Bloomberg

Employment: Resilient aggregate, narrowing breadth

The labour market complicates the Fed’s probable response to that inflation picture, but not in a reassuring way. April non-farm payrolls rose 115,000, beating consensus estimates; unemployment numbers held steady at 4.3%. Gains were concentrated in healthcare (+37,000), transportation and warehousing (+30,000), and retail (+22,000). The two-month net revision was –16,000. Persons working part-time for economic reasons rose 445,000 to 4.9 million. Federal Reserve staff analysis (Murray–Vidangos, April 2026) places breakeven employment at under 10,000 jobs per month — an extraordinarily low figure that suggests the headline growth rate flatters the underlying condition. A fuller treatment appears in the forthcoming GCIO Macro Note “US Labour Market: The Structural Inflection” (May 2026).

The Federal Reserve Transition

With inflation rising and the labour market showing signs of softness, this is not an ideal moment for a leadership change at the Central Bank. Kevin Warsh cleared a Senate procedural hurdle on 29 April and is expected to succeed Jerome Powell as the Fed chair around 15 May. The Fed funds rate stands at 3.50–3.75%, with the Committee divided in its approach and its statement retaining an easing bias despite rising inflation risk. Warsh is associated with balance-sheet discipline and a narrower reading of the mandate. The first market test should be straightforward: does his early communication reinforce inflation credibility, or does it read as accommodation of political pressure? If CPI is high this week, the answer matters immediately. A premature dovish signal would weaken the dollar, steepen breakeven inflation rates, and tighten conditions through the long end regardless of any front-end relief.

Bonds: The structural case against a durable rally

Bond funds attracted $17.0 billion in the week to 6 May, the largest weekly inflow since the week ended 18 February. Money-market funds took in $148 billion over the same period. The two flows sitting alongside each other rather than substituting signals regime uncertainty, not a clean risk-off trade.

The structural argument has not changed. Nominal growth is being supported by an energy price shock and an AI investment cycle that is, in the near term, demand-additive rather than supply-expanding. The Bank of England has modelled scenarios in which inflation induced by the Iran war exceeds 6% in early 2027. Joachim Nagel, President of the Deutsche Bundesbank and ECB Governing Council Member, has flagged a possible June rate increase. The Bank of Japan is reassessing its accommodating approach. A dovish Fed pivot into that global context would be the outlier, not the signal.

Xi –Trump summit and the Asia technology rotation

The 14–15 May Trump–Xi summit is the other principal risk event that will keep the market on its toes. A constructive outcome is a managed détente — US product purchases, tariff carve-outs, rare-earth assurances, possible Gulf co-ordination — sufficient to extend the China equity rerating and give the AI hardware rotation an Asian second leg. AMD gained 14.9% this week, adding $86 billion in market value; the Philadelphia Semiconductor Index gained 59% gains in 2026, a record in itself; South Korean retail investors’ leveraged exposure to KOSPI reached a record 25 trillion won in late April.

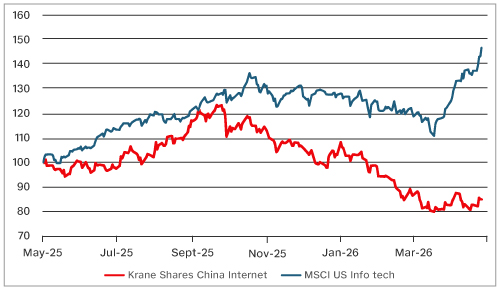

The bear case is not a bad-tempered press conference. It is a communiqué that leaves Taiwan and technology-control language ambiguous enough to unsettle allies without resolving the bilateral conflict. A mere paragraph of text – conciliatory or otherwise – has the power to reprice a sector. For context, Asian Technology shares in some places have lagged the US tech plays significantly (Chart 4).

Chart 4: Asian Technology has in Some Quarters been left Way Behind the US

Source: Bloomberg

The week ahead

US: CPI (Tuesday), PPI (Wednesday), retail sales, jobless claims, industrial production, import prices, and consumer sentiment. International: China inflation and activity, UK labour market and GDP, euro-area industrial production, ECB and Bank of England speakers. Geopolitical calendar: Trump–Xi summit (14–15 May) and any US–Iran shipping or ceasefire developments.

A last thought on the physical limits of the technology cycle

The market is pricing AI as though the build-out faces no binding constraints. The evidence from the ground is different, however. The proposed Stratos Project in Box Elder County, Utah, covers about 40,000 acres (approximately the size of the city of Paris) and could draw up to 9 gigawatts of power, more than double Utah’s current total power consumption. Governor Spencer Cox has imposed phased approvals, an initial cap of 1.5 gigawatts, and mandatory reviews of air-quality and water-use conditions. Communities are being asked to carry costs — electricity bills, water stress, emissions permitting, and land-use change. These costs do not appear in the share prices of the companies building the facilities. Utah will not be the last such dispute.

The deeper question is whether the productivity dividend embedded in AI valuations will materialise, and for whom. In what can be termed a sobering milestone, the 2024 National Assessment of Educational Progress reported that scores of US 12th-graders in mathematics and reading reached their lowest recorded levels: mathematics 3 points below the 2005 baseline and reading 10 points below 1992. A Senate testimony from cognitive neuroscientist Dr Jared Cooney Horvath argued that cognitive development across much of the developed world has stalled or reversed over two decades of rising school attendance and public investment, with digital saturation in education identified as a contributing factor.

The investment thesis for artificial intelligence is built on productivity gains delivered by a capable human workforce. If the same technology being priced as a productivity miracle has also degraded the cognitive formation of the next labour cohort, the return profile is more ambiguous than current multiples suggest. The winners are visible in the index. The costs are in utility bills, planning appeals, school attainment tables — and something harder to quantify.