Apr 27, 2026

Indian Equities: A pause in Leadership, not the end of it

• India remains a structural outperformer vs broader EM despite near-term divergence

• Corrections of 10–15% in a year have historically led to strong forward returns

• Current phase is a reset in valuations and time, not a break in the cycle

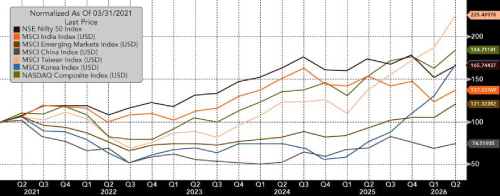

Indian equities are currently navigating a phase of consolidation after a strong multi-year period of outperformance. As the data suggests, while global markets particularly, the US and select North Asian markets have seen sharp rallies, India has taken a breather. This divergence reflects a confluence of factors: earnings moderation in domestic markets, global liquidity rotation into AI and semiconductor themes, valuation normalization, and sustained FII outflows.

It is important to contextualize this phase correctly. From CY21 through August 2024, India was a clear outperformer versus most global markets, supported by superior earnings visibility, macro stability, and strong domestic participation. The recent underperformance has largely emerged post September 2024 and remains narrow in duration. Even after accounting for this phase, India continues to hold its ground on a cumulative basis relative to global peers and remains ahead of broader emerging markets, which have seen more volatile and less consistent return profiles.

Historically, such phases are neither new nor alarming. Indian equities have frequently witnessed 10–15% corrections or periods of underperformance, often triggered by external factors such as global risk-off episodes or liquidity shifts. What stands out, however, is the market’s behaviour post such phases. Corrections in India have typically been sharp but short-lived, with the subsequent 6–12 months delivering strong returns as earnings catch up and flows normalize. Over the past decade, this dynamic has strengthened further, with recoveries becoming faster and more decisive, reflecting the growing role of domestic capital in anchoring markets.

In the current context, the evidence points to a time correction rather than a structural breakdown. Unlike the narrow, theme driven leadership seen in global markets, India’s market remains more broad-based, a characteristic that may cause it to lag in sharp global rallies but tends to make it more durable across full cycles.

Portfolio Performance: Viewing results through right lens

The past quarter was more challenging than anticipated, shaped largely by geopolitical uncertainty and relentless selling from foreign institutional investors.

The performance of our strategies relative to their benchmarks must be viewed through this lens. A summary as of 31 March 2026 is provided below

As on 31st March 2026

Sanctum Indian Olympians has been among the best-performing large-cap funds, delivering Quartile 1 performance for most part of the year. The portfolio changes implemented over the past several months have begun to show meaningful traction, and we expect this momentum to continue as the macro environment stabilises.

Sanctum Indian Titans experienced a more challenging second half of FY26, driven by broad-based selling pressure in mid- and small-cap names. However, we believe the worst is behind us. Several holdings that faced significant selling pressure have already staged strong recoveries in April 2026, including Oswal Pumps, Trent, BHEL, and JSW Energy. In addition, we have been incrementally building positions in names where we have high conviction: Solar Industries (defence supply chain), Nippon AMC (capital markets recovery), and Blue Star (summer cooling demand and data centre cooling infrastructure). These additions reflect our forward-looking view rather than a reactive repositioning.

India Aspires, being a concentrated strategy, was more directly exposed to the uncertainty created by geopolitical tensions and the resulting equity sell-off. In response, we adopted a deliberately conservative stance over the past 2–3 months, maintaining a higher cash allocation to preserve capital and retain flexibility. With the near-term environment showing signs of stabilisation, we have begun redeploying this cash into high-conviction opportunities aligned with the strategy’s core themes.

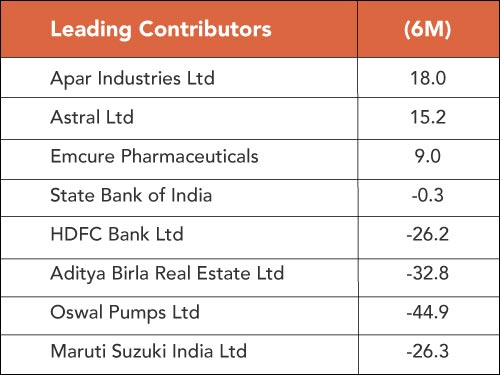

A six-month attribution summary of the top five contributors and detractors for each strategy is provided in the table below.

Here is the six-month attribution of the top five contributors and detractors.

Olympians Attribution

Titans Attribution

Portfolio Positioning: Themes we continue to back

• Energy and power – structural tailwinds from data centre expansion and the green energy transition continue to make this a multiyear opportunity.

• Selective lending financials – exposure to NBFCs and banks remains stock specific.

• Capital markets – we have incrementally added exposure to asset managers, reflecting confidence in the long-term financialisation of savings.

• Consumption and retail – under review, given rising input costs and margin pressure; any reallocation would be deliberate and data-driven.

• Commodities and exports – tactical allocations will be considered on a case-to-case basis as global trade dynamics evolve.

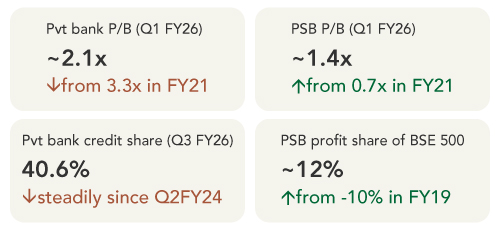

Sector in focus: Lending financials

One of the most frequent questions we have received is on our positioning in lending financials, the largest weighted sector in Indian equities. Our view has evolved and we want to be transparent about that.

The data demands a more selective stance.

Banking remains the largest profit pool in the BSE 500 and cannot be avoided in any serious portfolio. However, a blanket overweight is no longer warranted. The decade-long thesis of owning private banks at a structural premium to PSBs is under meaningful stress. Despite record-high profits, the sector is experiencing a structural de-rating, a signal that the market is demanding more before re-rating it higher.

We favour a more balanced approach: selectively retaining exposure to private banks with strong liability franchises and retail moats, while becoming more constructive on quality PSBs where the re-rating story is not yet fully reflected in valuations. A sustained re-rating of the sector, in our view, will require private lenders to demonstrably regain credit market share, a recovery that is likely to be gradual rather than sharp.

Outlook: A difficult year behind us, a better one ahead

FY26 proved to be an exceptionally challenging year, marked by extreme volatility, escalating geopolitical tensions, sharp energy price shocks, and record FII outflows. Indian equities underperformed global peers significantly. That said, we believe this painful reset has laid a solid foundation for recovery in FY27.

Valuations have been corrected meaningfully. The Nifty is now trading at a 12-month forward P/E of 19.0x, a 10% discount to its long-period average of 20.9x, offering an attractive entry point for patient investors.

Near-term conditions may remain choppy and range bound as global uncertainties linger. In this environment, a disciplined, bottom-up approach to stock selection will be the most reliable driver of outperformance. With much of the earlier optimism already reflected in prices, future returns are likely to hinge on actual earnings delivery rather than broad valuation re-expansion.

The structural growth case for India remains fully intact. Selective, earnings-focused investing should deliver rewarding results as geopolitical headwinds begin to ease, and we remain committed to that approach.

Here is how our flagship strategies have performed over different time periods.

Portfolio Performance