Jul 2, 2026

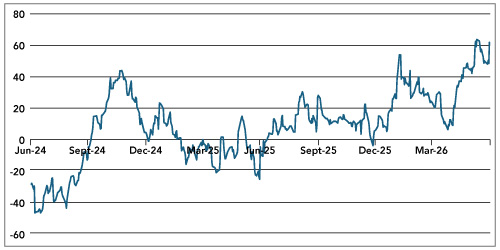

Q2 was neither recession nor recovery in the textbook sense. The global economy absorbed a genuine shock — the Gulf disruption, higher energy costs, tighter financial conditions — without buckling, then surprised positively into quarter-end. The global economic surprise index fell sharply through April before recovering sharply through June, comfortably above trend. But the composition of that resilience matters more than the headline: this is a capital-spending-led expansion, not a consumer-led one, and that distinction may shape how growth plays out in coming months.

April was the hard month. The Gulf disruption was never just an oil story — oil moved first, but the pressure quickly spread through freight, insurance, fertiliser and metals. What began as a commodity spike started to look more like a supply-chain sequence, and that distinction matters for policy: central banks can raise or cut rates, but they cannot produce more tankers, reopen shipping lanes or widen the Strait of Hormuz. The inflation this kind of shock generates is not one monetary policy is well-equipped to address

May exposed how regional the picture had become. The US and Japan turned higher on the surprise index while Europe slid deeply negative, China remained a selective, policy-supported story rather than a broad recovery, and India was squeezed by expensive imported energy and a weaker rupee. Treating the world as one macro block stopped being useful.

By June the US economic surprise index hit a three-year high, but the underlying mix is the real story. Corporate capex, AI infrastructure and technology investment are carrying the cycle; the household is along for the ride rather than leading it. Real consumer spending is tracking near 2% annualised — enough to sustain the expansion, not enough to call it a consumer boom. Savings rates remain low and accumulated price increases have left many households feeling poorer even with employment intact. That asymmetry — strong profits and capex, fatigued consumer — is the defining feature of this cycle, and it has policy implications: a capex-led expansion lifts earnings and markets without necessarily broadening into wages and demand.

Chart 1: US Economic Growth Surprise Index

Index

Source: Bloomberg

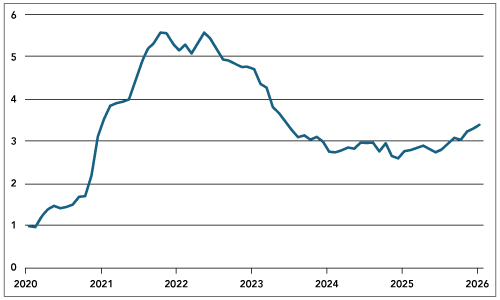

Inflation hasn’t been solved by the growth surprise.Core PCE rose to 3.4% y/y in May, the highest since late 2023, and the June Fed dot plot delivered a hawkish surprise — nearly half of FOMC participants now see at least one hike this year, versus none in March. The lesson: better growth data is not automatically good rate-cut news.

Chart 2: US Core PCE Higher but Likely Topping Out

Regionally, Europe remains weak but structurally constrained — exposed to imported energy, weak demand, and an ECB that may need to stay tighter than domestic growth alone would justify. Japan continues to benefit from corporate reform and reflation, though the yen and JGB market are now central to the equity story. Korea has become one of the clearest expressions of the AI infrastructure trade via memory and HBM chips — a reminder that the AI boom is as much an Asian industrial supply chain story as a Silicon Valley one.

The Gulf remains the key swing factor. Markets are pricing as if the disruption risk has passed, but a durable settlement isn’t yet visible. A resolution would bring quick relief on oil and inflation expectations; what it won’t bring quickly is normalised shipping and insurance costs or rebuilt inventories — businesses cut prices more slowly than they raise them. The first reaction to a deal would be relief; the second might still be sticky inflation.

China

China remained investable in Q2, but selectively so. Policy support was present and visible — enough to prevent a sharp deterioration and keep certain sectors functioning — but it did not translate into a broad domestic demand recovery. Consumption stayed subdued, the property sector offered no meaningful tailwind, and the recovery continued to depend more on state direction than organic momentum. For investors, China in Q2 was less a growth story and more a question of picking the right policy beneficiaries and avoiding the rest.

India

India’s structural story remained intact, but Q2 tested its near-term resilience. As a large energy importer, India was directly in the path of the Gulf shock — higher oil prices widened the current account, pressured the rupee and fed through into domestic inflation. That combination left the RBI with limited room to ease even as growth momentum softened. Valuations, which had already been pricing in India’s long-run potential, offered less cushion than usual when the macro headwinds arrived. The long-term case is unchanged; Q2 was a reminder that it will not be a straight line.

Asset Markets

Global Equities

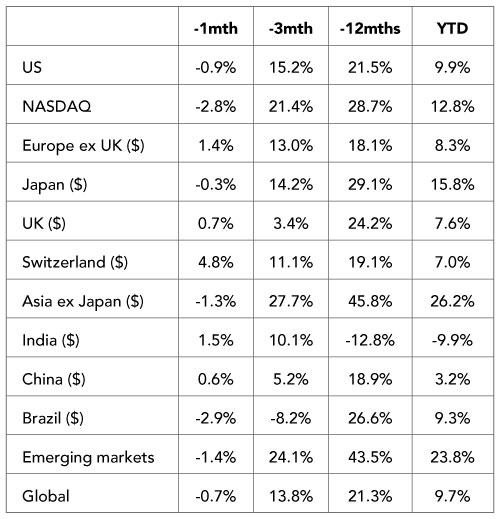

Global equities at quarter-end were in good shape, though the final days of the period have taken some of the gloss off the rally. The broad MSCI indices, measured in US dollars, show that the quarter has been positive for risk assets, but not in a simple or uniform way. The more interesting message is not that equities rose, but that leadership broadened and became more selective. The United States remained an important contributor, but the quarter was not simply an other chapter in the story of US exceptionalism.

Developed markets performed well, with the US, Europe and Japan all contributing to the global advance. The US market remains supported by earnings resilience and the continuing strength of the technology complex, but its relative performance was less dominant than in much of the post-pandemic period. That matters. A market priced for superior growth, superior margins and superior capital allocation has less room for disappointment when policy uncertainty, funding costs or geopolitical risks intrude.

Table 1: Equity Market returns in Q2

Source: Bloomberg

Europe also participated in the rally, with the eurozone stronger than the broader European market. That relative strength suggests investors were willing to look beyond the region’s familiar weaknesses of slow growth, political uncertainty and fragile confidence. The UK lagged over the quarter, although its longer-term performance remains respectable, helped by its more defensive and income-heavy market structure. Europe has not become a growth market overnight, but it has at least shown that lower expectations can be a useful investment starting point.

Japan has continued to behave well in dollar terms, despite the complications created by yen weakness. The market is still being supported by corporate reform, improved capital discipline, higher nominal growth and a more credible return of domestic inflation. That combination gives Japan a different character from most other developed markets. It is not simply a technology story, nor just a currency translation story. Investors are increasingly treating Japan as a structural reform market, and that remains an important change after decades in which rallies too often proved tactical and short-lived.

The most dramatic part of the quarter, however, came in North Asia. Taiwan and South Korea produced exceptional returns, with the TWSE rising around 45% and the KOSPI delivering a total return of around 68% in the quarter. Those are not ordinary moves for major equity markets. They show how powerful the combination of semiconductor demand, AI-related capital spending, currency support, recovering earnings expectations and domestic liquidity can become when global investors decide that the next phase of technology leadership is not confined to the United States. In this respect, the quarter was not just a US technology story. It was also a supply-chain story, and the market rewarded the countries most directly exposed to the physical infrastructure of the AI cycle.

Emerging markets also had a strong quarter, but the aggregate return hides a major split. Asia outside Japan and broader emerging markets performed well, while China remained the clear weak point. That divergence is important because it shows that investors are no longer buying emerging markets as a single risk basket. They are distinguishing between markets where earnings, policy, currency and liquidity conditions are improving, and China, where confidence remains fragile and the benchmark index continues to be a poor representation of the full opportunity set. India recovered during the quarter, but its year-to-date weakness means it still looks more like a rebound from a de-rating than a clean momentum story.

Taken together, the equity returns point to a market that is healthier than the headlines might suggest, but also less forgiving. The rally has broadened beyond the US, Japan has continued to build a credible structural case, and Taiwan and South Korea have shown that the AI trade has developed a powerful North Asian expression. Yet the late-month softness is a useful warning. Valuations, positioning and policy uncertainty still matter. The quarter has rewarded investors for taking risk, but the pattern of returns suggests the easy phase of the rally may already have passed.

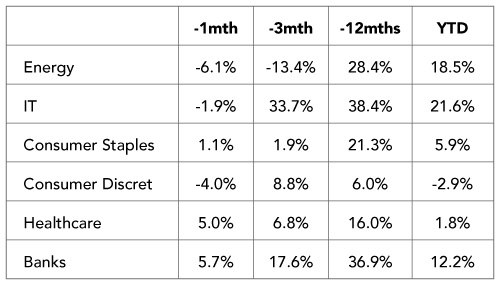

Equity sector performance

Sector returns this quarter showed a market becoming more selective. Gains concentrated in sectors with a direct line between current earnings and the year’s dominant themes, while sectors without that link lagged.

Information Technology led by a wide margin. The move was concentrated in AI infrastructure, memory, semiconductors and data-centre spending, not generic growth exposure. Micron’s results confirmed the AI cycle has broadened beyond Nvidia and processors into memory, particularly high-bandwidth memory. In South Korea, Samsung Electronics and SK Hynix became central to the story as investors priced in a stronger earnings cycle and large planned capacity expansion. The US still dominates the AI narrative, but the servers, chips, memory and manufacturing capacity sit largely in Taiwan and Korea.

Banks were the other clear positive. This added breadth beyond tech: a functioning economic cycle, decent nominal growth, capital markets and wealth-management income, and balance sheets holding up better than feared. The sector signalled no credit accident is underway.

Industrials benefited from less cyclical, more structural demand: defence spending, grid investment, automation, reshoring and the physical infrastructure data centres require. The AI economy runs on power, steel, copper, cooling and logistics as much as software, and Industrials captured that.

Healthcare was positive but unconvincing, without its usual defensive leadership. Obesity drugs remain a structural growth story, but pricing pressure, patent cliffs and uneven biotech confidence kept the sector divided. Novo Nordisk illustrates the tension — a large long-term opportunity offset by growing sensitivity to pricing and competition.

Consumer Staples was modestly positive — stable, not exciting. Predictable cash flows, but a more price-sensitive consumer after years of inflation kept the sector in a supporting role. Consumer Discretionary was mixed, reflecting a cautious consumer story. Pockets of strength in travel, premium brands and online platforms, but higher financing costs and uneven wage growth kept the market from re-rating the sector broadly.

Energy was the clear disappointment, giving back its Q1 Gulf-crisis gains. As the geopolitical supply premium faded, European majors lost the tailwind from Middle East-driven prices, while US majors saw a more uneven picture.

Materials also lagged, lacking a catalyst either way the global economy wasn’t weak enough to crush commodity demand, but China wasn’t strong enough to drive a materials boom.

Overall, the quarter marked a shift from Q1’s inflation-shock leadership toward visible earnings momentum: Technology led on real AI-driven orders and profits, Banks and Industrials added breadth, while Energy and Materials lost ground as the geopolitical premium faded and China failed to deliver a demand impulse.

Table 2: Global equity sector returns in July

Source: Bloomberg

Bond markets

The outperformance in the riskier parts of the credit spectrum through the quarter tells its own story. Spread compression rather than a rates rally did most of the work for returns. The EMBI spread tightened meaningfully over the quarter, continuing a trend that has been running for most of the year, as emerging market borrowers benefited from a calmer macro backdrop, firmer commodity prices in places, and investors searching for yield now that the acute risk-off phase of Q1 had passed.

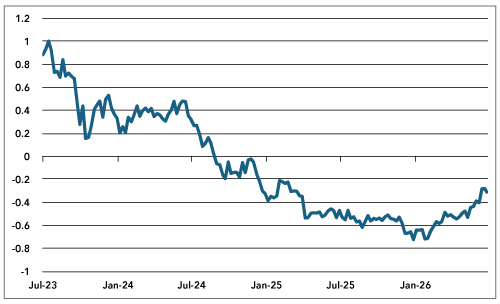

Government bond yields told a different and more nuanced story. The curve steepened over the quarter, with short-dated yields little changed to modestly higher while longer maturities rose more decisively. The move at the long end fits with the equity market narrative: an economy still expanding, an AI-driven capex cycle requiring financing, and growing supply of duration just as term-premium concerns resurface. The 2-year, more tied to the path of Fed policy, was comparatively well-behaved, while the 5-year and 10-year bore the brunt of the back-up in yields. Investors are increasingly distinguishing between near-term policy expectations, which remain anchored, and the medium-term fiscal and issuance dynamics, which are not.

For diversified portfolios, the quarter delivered what bonds are supposed to deliver in calmer conditions: positive carry and modest total returns, rather than the kind of negative correlation to equities that shows up only when growth is the dominant worry. With both equities and credit rallying together, government bonds were the laggard of the quarter — a reasonable outcome when the prevailing narrative is one of broadening earnings strength rather than recession risk.

Chart 3: US Government Bond Curve inversion starts to unwind

10-year US government Bond Yield less the two year

Source: Bloomberg

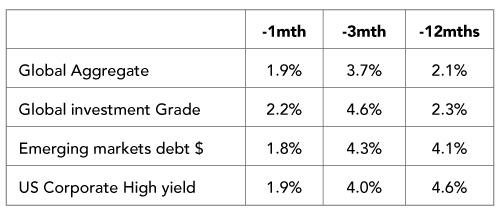

Table 3: Bond market returns In July

Source: Bloomberg

FX and Precious metals

The foreign exchange story in the quarter was dominated by a firmer US dollar. The USD Spot Index rose 1.2% over three months and 2.3% over one month. While investors still have their long term terms about the structural headwinds to the dollar from a high government debt to GDP ratio, the near term macro picture is supportive. The substantial inflows into US assets particularly the tech sector has helped as has the increased anticipation of a Fed rate hike.

Table 4: Monthly performance of precious metals and currencies for July

Source: Bloomberg

Gold was the quarter’s most striking reversal, falling 14% — one of its sharpest quarterly declines in recent memory. The move captures the Q2 narrative in a single price: gold had been bid up aggressively through the Gulf shock as investors priced in sustained inflation, geopolitical disruption and potential central bank policy error. As each of those fears moderated — energy risk premiums compressed, the US economy proved resilient and the Fed, while hawkish, remained orderly — the defensive premium unwound sharply. The hawkish June dot plot reinforced the pressure; real yields moved against gold and the dollar held firm. The decline is less a statement about gold’s long-run role and more a measure of how much crisis insurance had been priced in by March.