Jun 29, 2026

• An unconventional US economy revival led by CAPEX

• Stronger consumer spending led by higher wage growth is needed, but it may worry the Fed

• Market rally broadens – the old economy stirs

• :contentReference[oaicite:0]{index=0} sees pushback from the bond market

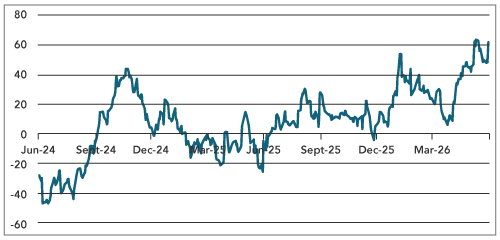

US economic data has staged a striking recovery, signalling the economy continues to remain resilient despite ongoing geopolitical tensions. In fact, the US Economic Surprise Index now stands at its highest level in about three years. Lingering worries about recession, energy shocks, trade disruption, weaker consumption, and the lagged effect of higher interest rates have taken a backseat, and the incoming data now point to a much more resilient US economy.

Chart 1: US Economic Surprise Indices – Inflation and Growth

Index

Source: Bloomberg

But the harder question is: what kind of recovery is this? It is tempting to call it a conventional cyclical upturn. The problem is that the post-COVID economy has exhibited patterns that have never behaved like a conventional cycle. It began with huge fiscal transfers, excess household savings, and distorted supply chains. The recovery was then characterised by strong nominal growth, debt-funded demand, an inflation shock, and the normalisation of interest rates. Now the economy appears to be entering a second phase of expansion, but with a different engine pulling it forward. It is not the household sector driving it. It is corporate spending, technology investment, and the extraordinary capital demands of the AI build-out.

In a traditional recovery, the consumer leads, employment rises, wages improve, confidence recovers, and households spend more. Companies then invest to meet stronger final demand. The current US cycle looks different. Corporate spending, especially around technology, is doing much of the heavy lifting. Households are still spending, but they are not obviously happy. The savings rate remains low, credit is much more expensive, and the cumulative effect of inflation has left many families feeling poorer. Real consumer spending is tracking around 2% annualised for Q2: enough to avoid a recession, but not enough to call it a household-led boom.

The global macro picture is more constructive now than it was earlier. Business sentiment has improved, financial conditions remain supportive, profits are strong, and technology spending is broadening. Business lending is also improving, and global capex indicators remain robust. But consumer spending has been steady rather than accelerating. That is why the word “recovery” needs careful consideration. The data are better, and the growth scare has faded, but this is not a clean early-cycle upswing. It is an erratic, debt-heavy, capital-spending-led expansion where the corporate sector is carrying more of the load than the consumer.

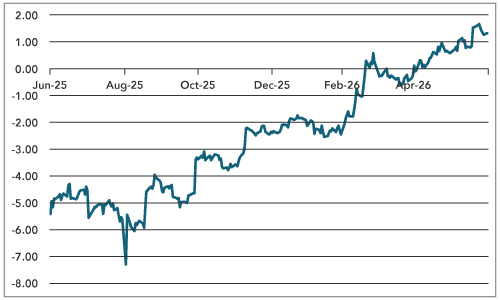

The wage question cuts both ways. Stronger wage growth would help households, but it would also concern the Fed, which is already looking at an economy that refuses to show classic signs of a slowdown. Core PCE inflation rose to 3.4% year-on-year in May, its highest since late 2023, and service inflation remains sticky. The June dot plot delivered a hawkish surprise: nearly half of the FOMC participants now project at least one hike this year, against zero in March. Market pricing of Fed rate hikes has pulled back in recent days, but good growth news is still not automatically good interest rate news.

Chart 2: Market Expectations of Change in Policy Rates by Year end

Source: Bloomberg

There is also a geopolitical caveat. Markets are behaving as if the disruption risk caused by the Middle East conflict has passed, but there is not yet a fully settled agreement. Renewed tensions between US and Iran and fresh pressure around Israel, Lebanon, and Hezbollah mean that the oil tail risk has not disappeared. It has merely moved in and out of the market’s attention. A sustained rise in oil prices would be particularly worrying because it would hit consumers while making central banks more reluctant to ease. That is the awkward mix investors hoped had faded: weaker real incomes, higher inflation risk, and less policy flexibility.

The Technology Debate Needs More Precision

The market’s view of technology is recalibrating quickly. The sector has moved from a near-universal push higher to a much greater discernment. Year-to-date performance now ranges from Micron up around 96% to Palantir and Oracle down more than 20%. The market is beginning to distinguish between real demand, stretched valuations, and the funding burden required to build the new infrastructure.

We should not give up on the broad technology sector. The AI cycle remains strong and second-quarter results could still surprise positively. Taiwan’s May export orders rose 47.2% year-on-year to around $89.5bn, the second-highest monthly total on record, with AI-related demand still the main driver. Clearly, that is not the behaviour of a technology cycle that has disappeared. But it certainly is the behaviour of a cycle where investors must be more selective.

As AI moves to the next stage, it is becoming more physical and more industrial. AI scaling is increasingly constrained not just by transistor density, but by the ability to assemble complex chip systems. Global silicon supremacy is no longer determined solely by who manufactures the smallest transistor. It is increasingly determined by who can assemble the most complex system. TSMC is expanding its CoWoS advanced packaging capacity from roughly 35,000 wafers per month in late 2024 to 130,000 wafers by the end of 2026, and the line remains sold out. NVIDIA alone has locked up more than half of CoWoS capacity through 2027. This is not a vague AI story. It is a real bottleneck in silicon, packaging, memory, substrates, and equipment.

SpaceX represents the best symbol of the change in investor sentiment. The company has been treated as one of the great frontier stories of the age: rockets, satellites, communications, AI, data, and ambition all wrapped into one, and thus demanding an exceptional valuation. But the bond market has a colder view than the equity market. SpaceX’s $25bn bond deal was a reminder that even the most exciting technology stories need financing. The subsequent weakness those bonds witnessed –the 10-year yield reported to have moved towards 6% – is a warning. SpaceX has not lost its imagination. It has simply met the cost of capital. SpaceX has come down to earth.

Chart 3: SpaceX 10-year Bond Slips After Launch

Source: Bloomberg

That is the broader message for technology. The AI boom is real, but so is the capital bill. The sector has run out of relying solely on internally generated cash and equity-market enthusiasm. It now has to tap credit markets, and the bond market is becoming plain hard-nosed. Equity investors can dream in decades. Bond investors ask who gets paid and when and with what protection.

For portfolio construction, this argues for a more specialist approach. The breadth of returns within technology now lends itself to actively managed long-short strategies, particularly in specialist hedge funds that can exploit dispersion rather than simply rely on the sector rising. In this environment, the best opportunity may not come from getting the market direction right, but from getting the winners and losers right.

The Old Economy Is Stirring

The consumer side of the equity market tells a different – and difficult – story. In the year-to-date, McDonald’s expected earnings have been revised lower from a peak of around $3.49 per share last August to around $3.34 per share now. Some of that may be company-specific, but it also reads as a warning about the average household’s ability to spend. McDonald’s has flagged that high gasoline prices and weaker consumer sentiment have hurt lower-income consumers. That fits the broader pattern. The consumer is not in collapse, but neither is the consumer obviously enjoying this recovery.

The broader corporate profit signal is more positive. The S&P 500 year-end target has been raised to 7,800, with 2026 EPS forecast at $350 and 2027 at $390. That tells us the profit cycle is still advancing. It also makes sense of the rotation visible on our performance screen. Over the past three months, some of the best performers have not been the fashionable mega-cap AI names, but rather brokers, banks, asset managers, selected consumer cyclicals, and industrially linked companies. Robinhood, Franklin Resources, Interactive Brokers, State Street, Morgan Stanley, Williams-Sonoma, MGM Resorts, Masco, Citigroup, Northern Trust, Goldman Sachs, and T Rowe Price all sit near the top of the three-month performance table. That is not a narrow technology market. It is a market beginning to reward better growth breadth.

The laggards tell an equally important story. The bottom of the three-month screen includes Charter, Tractor Supply, APA, CME, Occidental, EQT, AT&T, Netflix, Kroger, Nike, Lululemon, Exxon, and Chevron. That is a mixed group, but it reinforces the point that this is not a simple recovery trade. Some consumer names are struggling. Energy names have been hit by the conflict. Some quasi-defensive names are not behaving defensively. The market is rotating, but not blindly.

For Markets Next Week

The tension is straightforward. Better US growth news should help boost risk appetite. A stronger surprise index, improving earnings expectations, and a broader set of leadership names can keep nudging equities higher. Investors may continue to move beyond the narrowest AI winners into financials, selected industrials, capital markets businesses, and old-economy cyclicals that benefit from better nominal growth.

But, as stated earlier, the recovery is not normal. The consumer is constrained, the Fed is not yet friendly, geopolitics remains capable of reintroducing an energy shock, and parts of the technology complex are now being asked to justify their capital needs in the bond market as well as the equity market.