Jun 22, 2026

• The Great Equity Reversal – Equity comes out of Retirment

• The Warsh Fed – Short and sweet

• The Musk Premium – SpaceX outpaces Tesla

• The Dysfunctional America Risk – Where will we be by December?

There are weeks when the responsible thing to do is to sit down quietly, pour a decent cup of tea, and admit that the geopolitical situation in the Strait of Hormuz has once again defeated our best efforts at analysis. This is one of those weeks. TACOs — Tactical About-turns Creating Ongoing Surprises — have been arriving with a frequency that would exhaust a principal dancer and certainly exhausts us. We have not stepped back from our clients; we would never dream of it. We have simply concluded that any view held with conviction on a Monday has, by Tuesday, the shelf-life of a UK weather forecast in April. And so, in a spirit of intellectual honesty that borders on the therapeutic, we offer this week’s GCIO note as a dispatch from the calmer waters of equities, central banks and capital markets — where at least the absurdity follows a discernible pattern.

This week, four themes should command investor attention: 1) The structural shrinkage of global equity markets appears to be turning — a first in two decades, with significant implications for price discovery and capital allocation; 2) Kevin Warsh’s debut as Federal Reserve Chair confirms a fundamental shift in how the world’s most powerful central bank will communicate and act; 3) Elon Musk’s valuation premium continues to evolve in ways that challenge traditional financial analysis; and 4) Asian investors are beginning to make contingency plans for the risk of a dysfunctional United States — a risk that could become more pronounced as mid-term elections approach and domestic politics grows more volatile.

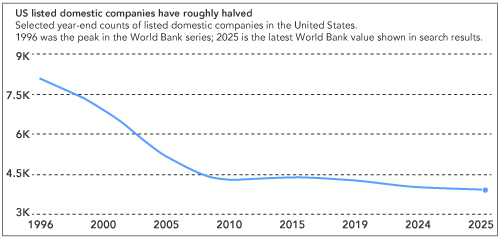

The Great Equity Reversal

Public markets start to grow again after nearly two decades of shrinkage

For the best part of two decades, the number of publicly listed companies has been on the wane. The United States, for instance, had roughly 8,000 listed companies at its peak in the late 1990s; by the mid-2020s that figure had shrunk by nearly half. Europe, Japan, and other developed markets witnessed a similar phenomenon. Public equity, in structural terms, was in retreat.

Chart 1: The Decline of Quoted US Companies

Two forces drove the decline. Private equity — sustained by two decades of cheap money and an apparently inexhaustible supply of institutional capital — systematically extracted companies from public markets. Management teams found the economics compelling: private ownership offered patience, opacity, and restructuring freedom that public life, with its quarterly scrutiny and activist shareholders, could hardly match. Entire sectors — healthcare, technology, industrial services, software — progressively moved toward privatisation. At the same time, the share buyback machine permanently retired large amounts of equity. Corporate America discovered that repurchases were more tax-efficient than dividends, more flexible than acquisitions, and reliably supportive of earnings per share. The net effect was a steady reduction in the supply of listed shares even as valuations rose, amplifying not only the upside but also the fragility of what remained.

The institutional framework changed in parallel. Passive strategies gained in popularity, relegating traditional active fund management to the background, and retail participation through ETFs surged. This new crop of investors was price-taker rather than price-setter, more keen on tracking indices than challenging valuations. Institutional influence declined; retail numbers grew; but the quality of price discovery weakened.

What appears to be changing now is the direction of travel. Tighter private equity financing conditions, a more selective IPO environment, and the growing appeal of public markets for AI and technology companies seeking large amounts of capital may be beginning to reverse the long structural decline in listed equity supply. If the public equity universe is genuinely expanding again after two decades of contraction, active managers who can distinguish real value from recycled private equity dressed up for public consumption may find conditions considerably more favourable than they have been in years.

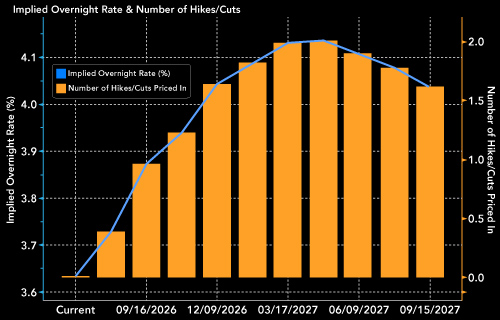

The Warsh Fed

Shorter words, harder message, new rules

The Federal Reserve held its policy rate unchanged at 3.50–3.75% last week. While the decision was unremarkable, the surrounding framework was not. Warsh’s first statement as Chair was almost half the length of his predecessor’s, devoid of any elaborate balance-of-risks language and conditional forward guidance. The message, precisely because of what was omitted, was harder: inflation remains elevated, the easing cycle is over, and the commitment to price stability is non-negotiable.T

The projections reinforced the hawkish shift. The median rate forecast for the end of 2026 rose to 3.8%, implying one more 25-basis-point increase rather than the cut previously signalled. Nine members now expect at least one hike before year-end; only one expects a cut. Inflation explains the pivot. The Fed raised its 2026 headline PCE forecast to 3.6% from 2.7%, with core moving to 3.3%. Of the 18 participants, 17 judged inflation risks to be skewed to the upside. Growth was barely touched, revised to 2.2% from 2.4%. This is not a stagflation diagnosis. It is an economy with solid fundamentals and too much inflation, and the Fed has decided to treat it as such.

Chart 2: Market Pricing of Fed Rate Hikes

Source: Bloomberg

Warsh has replaced Powell’s detailed instruction manual with something closer to: we know where we are going, but we are not giving you the direction. There is intellectual merit in that approach — forward guidance too often becomes a hostage to forecasts that subsequently prove wrong, and the discipline of saying less can itself be a form of credibility. The risk is that the communications vacuum does not stay empty. In such a scenario, every regional Fed president becomes a potential market mover, and competing interpretations may generate more volatility between meetings than carefully choreographed guidance ever did. Nevertheless, our own interpretation is that the burden of proof has shifted. The debate is no longer about when the Fed might cut. It is about whether the Fed can avoid tightening again. That is a material change for risk assets, duration, and credit spreads.

The Musk Premium

When a founder becomes an asset class

Financial history has had moments when investors stopped valuing a company and started valuing an idea. Tesla was a straightforward execution premium — rather than buying the company, investors bought the belief that Musk could dominate the electric vehicle market. His documented history of achieving outcomes that expert consensus had dismissed made that belief – and the premium – defensible. Reusable rockets were once considered impractical. Then, for years, established automakers dismissed mass-market electric vehicles as unsustainable. The Tesla premium reflected a genuine track record applied to a visible future market.

SpaceX is a fundamentally different proposition. The operational business is exceptional: Starlink alone would command a premium valuation in its own right, with launch services and defence contracts further boosting its appeal. But an increasing share of the valuation debate concerns markets that do not yet exist — orbital data centres, space-based AI infrastructure, lunar logistics, Mars transportation, etc. Tesla asked investors to believe in one large future market. SpaceX asks them to believe in several speculative ideas simultaneously, and to trust that Musk is uniquely capable of bringing those ideas into existence.

Chart 3: Tesla Price to Sales Ratio – SpaceX closer to 130x

Source: Bloomberg

Musk may have become one of the few individuals in modern financial history whose personal credibility is itself a valuation metric. Investors are no longer simply buying a company; they are buying an idea and his probability of being right on that idea. The question worth asking is not whether that probability is high. It is whether current prices already assume that idea to be near-certain, and what happens if it fails. The execution premium that made Tesla’s valuation rational was grounded in a track record within visible markets. The premium now embedded in SpaceX reflects confidence in Musk’s ability to create markets that do not yet exist. That is a categorically larger leap of faith.

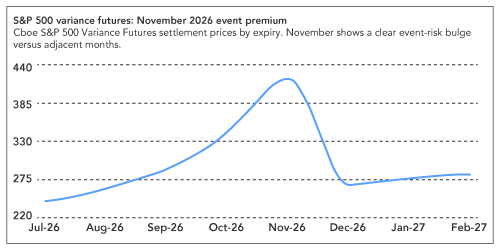

The Dysfunctional America Risk

Asian investors start to plan for it

A conversation is gaining momentum among Asian institutional investors that has not yet been fully acknowledged within Western risk frameworks. The concern is not about a specific policy decision or an identifiable event. Rather, it is the possibility that the United States is entering a period of genuine political dysfunction at a moment when its global leadership role is most in question. President Trump’s second term has been characterised by erratic decision-making, abrupt trade policy reversals, and an approach to allies that oscillates between coercion and indifference. The administration’s grip on Congress has narrowed, domestic opposition is growing, and the institutional guardrails that once moderated policy volatility are under continuous pressure. As mid-term elections approach, a president who perceives his power weakening has every incentive to escalate rather than moderate. History suggests administrations in that position do not pull back; they double down.

US volatility markets are already attaching a premium to the November 2026 risk window. The S&P 500 variance futures curve shows a pronounced jump in the November contract, well above adjacent expiries, consistent with investors hedging not simply day-to-day volatility but a more extreme political or policy-related market shock. The message is not yet panic, but it is a clear sign that the midterm election period is being treated as a discrete risk event.

Chart 4: Market pricing Trouble around Mid Term Elections

Source: Bloomberg

Asian investors — sovereign wealth funds, family offices, and institutional allocators from Singapore to Tokyo to the Gulf — are having a serious rethink even as their Western counterparts remain largely indifferent. As those concerns grow, three broad contingency themes are emerging: a gradual reduction in unhedged US dollar exposure, into gold and regional currencies, deliberate but modest; a reassessment of US Treasury duration, with investors becoming more selective about the yield required to absorb supply; and an acceleration of intra-Asian investment frameworks in trade finance, technology supply chains, and financial infrastructure, partly economic and partly insurance against abrupt American policy shifts.

None of this implies investors are wholeheartedly abandoning the United States. Its capital markets remain the deepest and most liquid in the world, and its technology sector is unrivalled. But the working assumption of American stability — the bedrock of global portfolio construction for three-quarters of a century — is undergoing a careful reassessment. When sophisticated Asian investors begin building portfolios that do not assume that stability as a given, global allocators would do well to pay attention. The risk is not that America fails. The risk is that markets are pricing as though it cannot.