Jul 18, 2024

Quarterly Roundup

• The markets kept crawling up during the quarter amid heightened volatility around the general elections.

• If the earnings continue to grow, there shouldn’t be a significant threat to long-term equity returns.

• The granular election results don’t look so favourable for the current dispensation, which went quite confidently into the elections expecting a bumper majority.

• If the government ups the social welfare expenditure or devises other schemes to address rural distress, some opportunities will emerge in the rural-focused sectors.

• We made further changes to the portfolio this quarter, adding exposure to telecom, consumer, auto and housing finance.

The markets kept crawling up during the quarter amid heightened volatility around the general elections. The headline indices posted mid-single-digit returns, while the mid-and-small-cap indices massively outperformed the headline indices with 15-20% return in the quarter.

The March quarter earnings also came in the last three months, and barring IT, Consumer Staples and Chemicals, all other sectors put up a decent show. The traction was better in B2B and B2G businesses, riding on the investment/capex-led economic growth. Premium/luxury discretionary consumption continued to do well, vindicated by the presales volumes and cash generation of property developers and sales volume growth in premium liquor.

Here is how the aggregate earnings looked in the quarter for the BSE500 and Sanctum Indian (Titans) portfolio.

Source: Ace Equity, Sanctum Wealth Research

The big event (general elections) is now out of the way for the markets, and in the absence of a clear mandate for a single party, a coalition government is back at the centre after a 10-year hiatus. The markets became used to the political stability at the centre in the last ten years, with Nifty500 delivering a robust 300% return in the period in local currency. This is massive outperformance when compared with the MSCI global index returns of 153% and MSCI emerging markets index returns of 35% in the same period.

A macro-level change like the formation of a business-friendly or reform-oriented government at the helm should ideally result in an expansion of the valuation multiples ascribed to the concerned market. However, in India’s case, that did not seem to move the needle much as around 80% of the index returns in the last ten years came from earnings growth. The same contribution in the UPA era of 2004-2014 was ~60%, when the index returned 370% in 10 years. In both cases, the earnings grew at a similar pace and contrary to the general belief, the multiples expanded more during the coalition era.

Therefore, if earnings continue to grow – which they have regardless of the kind of government at centre – there shouldn’t be a significant threat to long-term equity returns. In most cases after elections the volatility dies down in at most a quarter, and the discussions come back to basics.

What’s Next

The current case is more skewed towards political continuity than a drastic change in the political and economic landscape, which doesn’t give us a solid reason to be pessimistic about the opportunities in the equity markets.

However, the leading sectors going forward may be different from what they have been in the recent past. In fact, sector rotation has been a norm even when the same government has been at the helm for multiple terms. Even in PSUs – the biggest theme before elections – there may now be a polarisation, wherein investors will pick the better PSUs with earnings visibility rather than buying the entire PSU basket. This will also bring some sanity to the market, focusing on quality sectors/companies that have been overlooked so far.

The granular election results don’t look so favourable for the current dispensation, which went quite confidently into the elections expecting a bumper majority. A lukewarm mandate may force the government to look seriously into the rural distress, which has been plaguing the economy for quite some time now. Thanks to the buoyancy in premium consumption and increased infra investment – which has tripled in the last four years – the economy continued to fire despite a big COVID jolt and the subsequent K-shaped recovery.

If the government ups the social welfare expenditure or devises other schemes to address rural distress, some opportunities will emerge in the rural-focused sectors like farm equipment, two-wheelers and consumer staples.

A host of opportunities will also emerge from the government reforms as they have in the past. For example, we highlighted the government’s role in regulating and straightening the real estate sector, which now seems to be in a multi-year bull run. As we were bullish on the theme for the last 2-3 years, we invested in it through ancillaries like pipes, and wires, and cables first and recently directly through real estate developers.

Portfolio Changes

In the last quarterly note, we mentioned some other changes we made to the Titans and Olympians portfolios while also highlighting the thematic tailwinds the corresponding sectors were experiencing. We made further changes to the portfolio this quarter, adding telecom, consumer, auto and housing finance exposure.

In telecom we took direct exposure to Bharti Airtel in Indian Olympians (Olympians) and Indian Titans (Titans) and a telecom ancillary – Tejas Networks in Titans. There are several tailwinds for the sector at the current juncture. Tariffs are moving up, competition has abated, broadband penetration is improving, and consistent investments are happening in network upgrades and the rollout of advanced technologies. The government – along with the telecom PSUs – is also focusing on improving rural connectivity through BharatNet phase III, which will help improve the last mile connectivity with a capital outlay of Rs. 1.4 lakh crore.

As the competitive intensity has gone down in mobile services, Bharti’s earnings have also improved with its topline rising ~50% in the last three years and EBITDA growing 73% in the same period. As the pricing power has come back to the telecom players, another round of tariff hikes has happened, which will help the company generate strong free cash flows (FCF).

In the last quarterly note, we mentioned some other changes we made to the Titans and Olympians portfolios while also highlighting the thematic tailwinds the corresponding sectors were experiencing. We made further changes to the portfolio this quarter, adding telecom, consumer, auto and housing finance exposure.

In telecom we took direct exposure to Bharti Airtel in Indian Olympians (Olympians) and Indian Titans (Titans) and a telecom ancillary – Tejas Networks in Titans. There are several tailwinds for the sector at the current juncture. Tariffs are moving up, competition has abated, broadband penetration is improving, and consistent investments are happening in network upgrades and the rollout of advanced technologies. The government – along with the telecom PSUs – is also focusing on improving rural connectivity through BharatNet phase III, which will help improve the last mile connectivity with a capital outlay of Rs. 1.4 lakh crore.

As the competitive intensity has gone down in mobile services, Bharti’s earnings have also improved with its topline rising ~50% in the last three years and EBITDA growing 73% in the same period. As the pricing power has come back to the telecom players, another round of tariff hikes has happened, which will help the company generate strong free cash flows (FCF).

We also took exposure to housing finance in Titans, furthering our positive stance on the housing theme. We picked PNB Housing Finance – a company changing its loan mix aggressively to add affordable housing in the loan mix, which is currently tilted towards high-ticket loans. Even in its core loan book, the company is working towards reducing the ticket size. The financier also fits well in the rural theme as it is expanding heavily in tier III and IV towns to cater to the financing needs in affordable housing in the hinterland.

Summing up

Though the euphoria in the PSU stocks hasn’t died down yet, there is some evidence of sector rotation from risky sectors to safer/quality themes. A case in point is the Nifty Private Banking Index, which is touching new highs, while the PSE and PSU Bank indices are consolidating. The IT index, despite not-so-good near-term sector prospects has also outperformed the general market from the start of June. However, the torchbearer of safety and quality – the FMCG index – has settled lower after hitting new highs at the beginning of the month.

It’s too short a time to decipher a trend, but the signals currently from markets are mixed at best. As the rally in the last twelve months was mostly driven by government capex, investors are waiting to know the priorities of the current coalition government before loading up on the PSU names. While the MSP hike has given an indication, the air will be clearer at the time of the full budget that is scheduled to be presented later in the current month. If the government focus shifts from investment to boosting consumption, the set of winners will be entirely different.

At Sanctum, our mechanism builds in a lot of caution. We first take an investable theme and then select the most promising candidates from the theme with tangible business progress/earnings to show. This simple criterion filters out several trends that have little fundamental backing or are too risky to bet on. It keeps us away from low-quality themes that absorb investors’ money only in a highly risk-on environment. Many times, our selected themes play out in the long term – doing well in the short run, taking a pause and taking off again. It’s during those pauses that investors must keep patience and trust the process to get into the take-off phase.

We believe that most of our portfolio themes are in a long-term structural trend, which has taken a brief pause because the markets have become too risk-on. We have started seeing some reversal in the past few months, and we are confident that the mean reversion in markets will work in favour of our portfolio strategies.

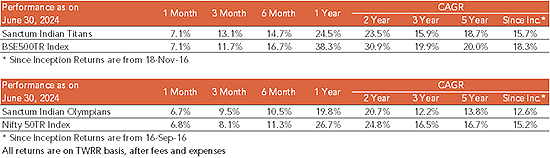

Here are our flagship portfolio strategies across short and long-term horizons.

The detailed performance can be viewed and compared with other PMS performances on this webpage.