Aug 16, 2024

• Global markets turn volatile amid concerns around Yen carry trade, earnings and Fed actions.

• Indian macroeconomic strength also starting to moderate.

• We turn underweight Indian equities amid elevated valuations, moderating macro strength, downward earnings revision and unfavourable technical momentum.

• We add to gold as its fundamentals are intact.

Exercicing Caution

It has been 18 months since ChatGPT stormed into our lives and captured the imagination of the average internet user. Artificial Intelligence has transitioned from geeky to a household term. The ‘Magnificent 7,’ a group of dominant tech companies, have rallied hard to deliver nearly a 200% return (as represented by the CNBC Magnificent 7 index) since the beginning of last year. However, during the current earnings season, it has become apparent that despite spending billions on AI, these companies are uncertain about the timelines for achieving significant revenue gains or profitable new products. This uncertainty has led investors to question these expenditures, resulting in a correction in these stocks.

The correction in US Stocks was also compounded by jitters surrounding the yen carry trade. In this strategy, investors borrow in yen and invest in other currencies, such as the USD. This approach remains profitable as long as Japanese interest rates and the yen are stable or declining. But the yen appreciated swiftly, and the Bank of Japan hiked rates, forcing borrowers to unwind some carry trades. The repercussions of this reversal were felt in Asian markets, with indices falling sharply that day. The Bank of Japan has since said it will refrain from sudden moves.

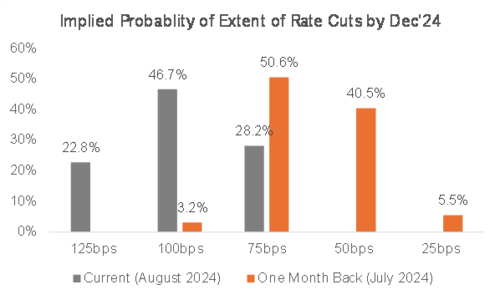

The significance of this development is tied to the Fed’s actions too. The Fed held the rates steady yet again, stating that inflation was still somewhat elevated. Fed Chair Powell emphasised their dual mandate of managing employment and inflation, given the recent softening in the labour market. He signalled a possibility of cuts in September. However, markets are clamouring for a larger rate cut of 50 bps, although this may not set off the expected rally in equity markets. Lower interest rates in the US may result in a weaker USD and a corresponding stronger Yen, which, as explained above, is not favourable for equities. More gradual moves by the Fed could give markets time to adjust without knee-jerk corrections.

Market clamouring for larger rate cuts by the Fed

Source: CME Group, Fed Watch Tool

Turning to geopolitics, tensions have been fluctuating since the onset of conflicts in Ukraine and the Middle East. Recent developments include Ukraine’s first incursion into Russian territory and escalating preparations by Iran and Hezbollah to retaliate against Israel following the recent assassinations of Hamas and Hezbollah leaders. This is another factor that the market will be closely watching.

Global Market Update

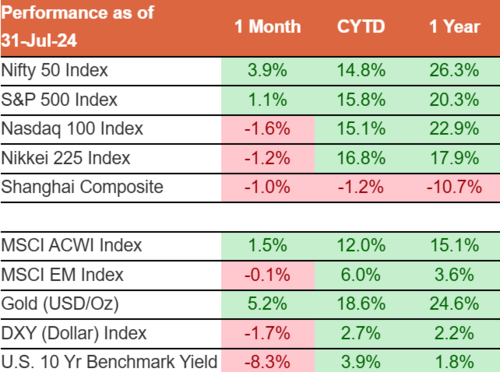

Global equity markets tumbled due to concerns about the unwinding of the yen carry trade and weak economic data in the U.S. Japanese equities fell more than 12% in a single day in local currency terms. Since then, the market has bounced back and recovered most of its losses. U.S. government bond yields declined on expectations of further interest rate cuts by the Fed.

Source: Bloomberg, Sanctum Wealth. Above returns are price returns in local currency terms

India Market Update

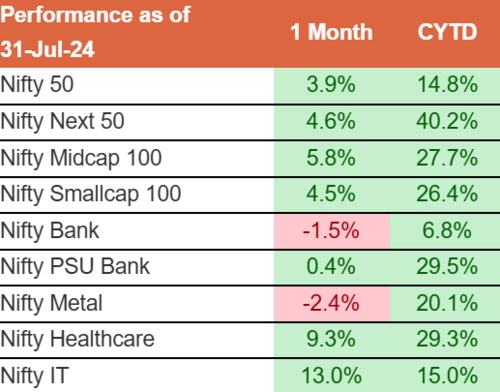

Indian equities experienced a correction following the union budget’s increase in capital gains tax on Indian equities. However, the market quickly adjusted and moved higher. The global risk-off sentiment also affected Indian equities, causing volatility in line with the international markets. Mid and small caps continue to outperform large caps, while more defensive sectors, such as healthcare and IT, performed well.

Source: Bloomberg, Sanctum Wealth

The above returns are price returns

India Macro Update

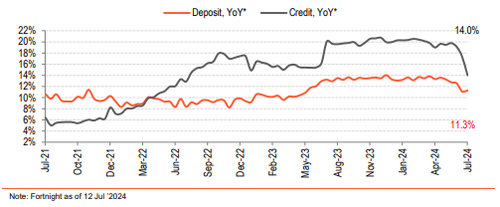

India’s macroeconomic indicators have been strong for several years. However, we are now observing some softness in certain numbers. This could be due to reduced government spending in the run up to the elections and needs to be tracked. Credit growth, a key indicator, has moderated, as have port cargo volumes and air passenger traffic. On the other hand, acreage for Kharif sowing increased, thanks to favourable monsoon trends.

Credit growth starting to moderate

Government Spending (12 Month moving average)

Outlook

Equities:

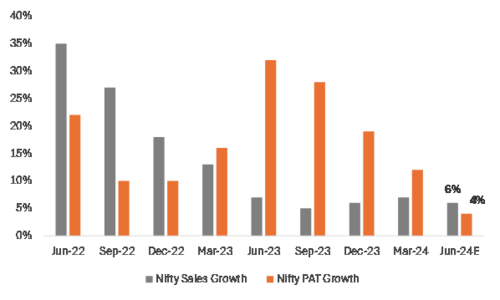

While building our view, consider various factors, such as macroeconomic trends, corporate earnings, valuations, flows and technical indicators. While most factors, aside from valuation, have been favourable to varying degrees, recent earnings releases and management commentaries suggest that peak margins may be behind us, and volume growth is somewhat tepid. Effectively, fundamentals haven’t caught up with expectations built into valuations. Additionally, technical indicators also point towards a potential grind down in the markets.

PAT growth likely to be muted as peak margins are behind us

Source: Bloomberg, Sanctum Wealth

In summary, we are dealing with some softness in macro factors, downward earnings revision, expensive valuations, and unfavourable technical indicators on one hand and exceptionally strong flows on the other. On balance, we believe it is time to re-assess our weights into equities. We plan to gradually reduce our exposure to equities by ten percentage points in our model portfolio for aggressive clients.

We also believe that, over the next few months, markets may rotate away from all the themes that have run up significantly (mid and small, PSUs, infrastructure). Therefore, exposures to these segments need to be rebalanced.

Fixed Income:

In its recent statement, the RBI has downgraded its growth forecast for Q1 FY25. At last week’s MPC meeting, rates were held steady, in line with expectations. The RBI remains cautious about food inflation and has revised its CPI expectations for the current and next quarters upwards by 60bps and 10bps, respectively.

Our previous notes highlighted that bond yields might drift lower before rate cuts become apparent. This scenario has already unfolded. We believe the rate-cut cycle in India is likely to be shallow, with the RBI potentially lagging the Fed in reducing rates. However, due to the increased liquidity from bond index inclusion, there could be sufficient yield compression to justify duration exposure. As a result, we have been recommending such exposure.

Indian bond yields have drifted lower

Source: Bloomberg, Sanctum Wealth

Gold:

The recent price correction in gold in India was due to a change in customs duty, not a shift in fundamentals, which remain intact. Central bank buying, inflation hedge, and elevated geopolitical risks all favour gold. Rate cuts in the U.S. should weaken the USD, leading to an appreciation of gold as a currency. Therefore, we will allocate some portions we reduce from equities to gold.

We are fully aware that both actions may take a few quarters to play out and could cause intermittent pain. However, Indian equities have delivered strong returns over the past four years, creating a cushion in client portfolios. Given the current situation, we prefer to focus on protecting the downside rather than maximizing returns. These adjustments are tactical; for the long term, we remain positive about India’s potential for wealth creation.