May 19, 2026

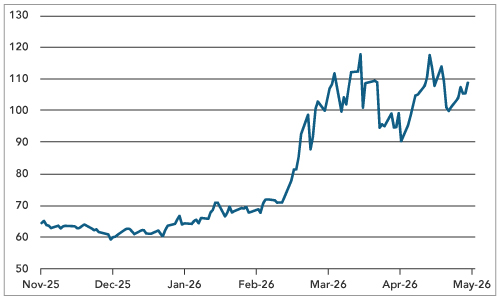

The stabilisation we currently see in the market is built on the belief that sense will prevail in the Strait of Hormuz. In fact, a Brent oil price near $110 is consistent with managed stress and has kept us away from expecting the worst. It is, however, not consistent with a standoff where both sides believe the other will blink first and neither does. Global inventories, meanwhile, have fallen roughly 400 million barrels (approximately four days of global supply) since the disruption began. A reopening of the Strait requires more than diplomacy. It requires a credible, jointly ratified announcement, the kind that can only be sustained with institutional backing. Without that, any partial move risks being reversed, and the market remains in a reflexive loop that it is not yet pricing the risk – or the lack of it – correctly.

Chart 1: Brent Oil Price Still Pricing Hope ($ bbl)

Source: Bloomberg

A difficult scenario is not just a dramatic escalation. It is a standoff that lingers on. In that environment, the energy shock will not fade. Rather, it will feed into core prices, wages, inflation expectations, and currency markets simultaneously — and that is the path to macro problem from oil problem. The equity indices looked generally solid last week because they were not pricing the fragility underneath. We would like to note here that JP Morgan has a baseline call for a June reopening driven by inventory depletion. That’s not really an analytical insight, it’s a hope!

While the macro backdrop remains relatively strong, it makes complacency about oil particularly dangerous. Global core inflation excluding China has held close to 3% annualised since the second half of 2023, even as above-potential growth and tight labour markets persist. Global real retail sales ex-China accelerated to a 2.7% annualised pace through March, and April US retail sales remained solid with core PCE above 2.8% and services inflation near 4%. This is not a fragile economy waiting to be knocked over. It is a resilient economy with no buffer for a second inflation shock. The Fed debate has already shifted: markets now price in a Fed funds rate hike no later than early next year, with the risk of an earlier move if data remain firm.

European fixed income: the first proper entry point

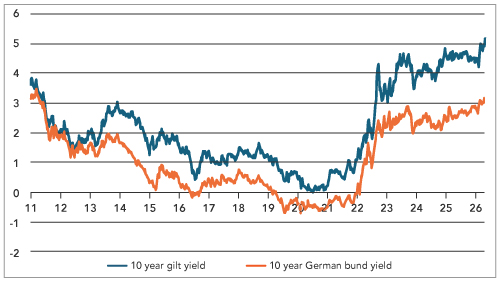

Investors have struggled to find value in asset markets despite the war in the Middle East. However, selective fixed-income markets are starting to offer some value. While equity markets have held up well, last week fixed income markets caved. Bund yields have risen nearly 80 basis points from their early-year lows, and German 10-year real yields are sustainably positive for the first time since the pre-zero-rate era. We believe this provides a tactical opportunity in eurozone government debt. Eurozone core inflation was running at approximately 2.7% in April, versus above 3% in the US. German GDP grew just 0.2% in Q1. Also, the market prices an early ECB rate rise, which may have an immediate negative impact on the economy. The 10-year Bunds at 3.12% and 10-year gilts at 5.16% appear to be offering value.

Chart 2: UK and German 10-year Government Bond Yield (%)

Source: Bloomberg

Yields have advanced far enough to compensate long-term investors for uncertainty, particularly in Europe, where growth is softer and the policy path is far more pronounced than in the US The risks are that an escalation in the Middle East pushes energy prices higher again, or the ECB and BoE are forced to tighten rates more than expected. We acknowledge those risks with respect. At these levels, the risk-reward has shifted.

The UK is more complicated. Gilts at 5.16% now carry a genuine political risk premium — the market is pricing in some probability of a disruption in the Labour leadership, and a policy shift toward higher spending. That does not make gilts uninvestable. It is partly why the entry point is interesting. But we treat UK long-term debt as a political trade as much as a macro one. Investors might look to accumulate on weakness.

The generational shift: why this matters for portfolios

While we are on UK politics, it’s worthy of discussion on a theme that is increasingly a feature of global geopolitics in many democracies. The old party politics does not align with the emerging Next Gen voters. We are seeing political voices in the UK starting to take up the mantra of the younger voters. While the ironically named Reform party continues to barrel on with an agenda to sway baby boomers, some of the potential leaders of the Labour government – and therefore the contenders for the prime minister’s post – are adopting New Gen agendas. A Labour party that pivots toward that vision, toward a more European outlook, toward investment in housing, clean infrastructure, and opportunity rather than austerity management, could lock in a governing coalition that outlasts anything Reform can build. The party is sitting on a generational coalition it has not yet fully claimed. Gen X and Gen Z voters — the cohorts that did not vote for Brexit, that carry its opportunity cost in stagnant wages, unaffordable housing, and constrained career mobility — are looking for a political home that articulates their reality.

Reform’s support base tells its own story. It is disproportionately older, disproportionately outside the major cities, and disproportionately animated by the sovereignty politics of the Brexit era. That is not a growing coalition. It is a declining one. The baby boomer demographic that drove the 2016 vote is shrinking as a share of the overall electorate with each passing year. Reform may have reached its high-water mark. What looks like a political insurgency may in fact be the last strong expression of a fading agenda rather than the beginning of a durable governing majority.

For global investors, what is happening in the UK may end up being the forerunner of something structural. The fiscal regime of the next decade may not resemble the low-tax, asset-owner-friendly environment of the preceding one. Higher taxes on wealth, property, and inheritances and corporate rents are not tail risks in this environment — they are the direction of travel as the median voter changes. The data-centre backlash fits the same frame: Gen Z and younger millennials are already disproportionately exposed to the costs of AI infrastructure buildout — higher energy bills, grid pressure, land and water competition — with limited participation in its financial returns. They are a natural political constituency for that backlash. The risk to the AI trade is not purely technological. It is political, and it is underpriced.

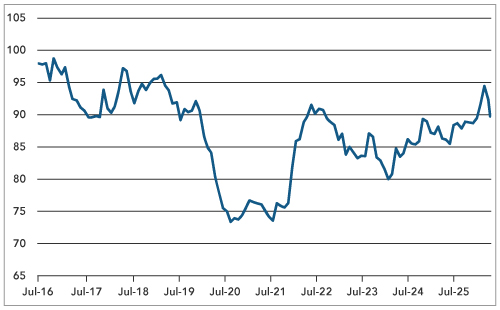

Chart 3: UK Equity Markets Performance Since the UK Voted to Leave the EU

MSCI UK TR versus MSCI Europe ex UK rebased to July 2016=100

Source: Bloomberg

China–US: who set the rhythm

The market was predictable in its conclusion: no major breakthrough, relationship rebranded as “constructive strategic stability,” commitments on soybeans, LNG, beef, and a Boeing order that came in below expectations. Both sides agreed Hormuz should reopen. That is tactically useful, but structurally inconclusive. A more comprehensive settlement will likely wait for Xi’s expected visit to Washington in September.

That is not the story that matters.

What mattered was who controlled the tempo. China arrived with discipline and a clear negotiating stance. The US side was performing — seeking visible wins, eager to demonstrate that the relationship was being managed well, presenting outcomes to a domestic audience. China used that asymmetry carefully. There were deliberate signals throughout the meetings: references to the multilateral order being disrupted by others’ unilateral decisions, the framing of China’s industrial self-sufficiency not as a defensive posture but as a long-term strategic achievement, and the quiet positioning of renminbi-denominated trade as a settled fact rather than an aspiration. These were not confrontational statements. They were the language of a power that no longer needs to argue its legitimacy.

The structural takeaway is this: China is not seeking to dismantle the old order by confrontation. It is comfortable letting the old order rearrange itself while China consolidates its position. That is a different kind of power, playing a longer game. For medium-term portfolio construction, the direction of that structural shift is not ambiguous, and the summit confirmed it.

The framework: anchor in the East, selective in the West

The China-US summit provided support for our structural shaping of portfolios. The east gives us the anchor — China’s strategic industrial depth, the continued strength of Asian supply chains, select emerging market credit where spreads have not caught up with issuer quality, and the underappreciated resilience of Asian domestic demand in a world where global goods trade is restructuring. We hold that conviction.

US equity exposure stays concentrated in earnings compounders rather than rate-sensitive or high-multiple segments. Japan remains a curve-steepening trade, with the front end already pricing Bank of Japan hikes and the long end still exposed to weak demand and fiscal pressure. We do not avoid the West, but we do not treat it as the default engine of returns.

The macro path remains narrow. Oil must stabilise. Central banks must avoid over-tightening. The US–China rivalry must stay managed. And AI infrastructure must continue scaling without any serious political disruption around power, water, and grid costs. None of these outcomes is individually implausible. Together, they require a sequence of rational political decisions in which investors are currently not being adequately compensated for the risk of failure.

The East gives us the structural confidence to stay invested. We are building from that. The West is where we are paid to be selective, and where the cost of not being selective is rising. Nvidia’s earnings this week is the marquee near-term event — the market is expecting it to not just beat numbers but to further strengthen the argument that AI can offset higher rates, higher oil, and a more difficult political environment. We would not build a portfolio based on that hope alone. We would build it around the structural shift that is already underway.