May 11, 2026

• Global markets have rebounded sharply on hopes of easing Middle East tensions.

• AI-led capex continues to support global growth even as inflation pressures re-emerge.

• India’s economic activity remains resilient despite higher energy prices.

• Q4FY26 earnings have broadly met expectations, with estimates remaining stable.

• We remain constructive on equities and are gradually increasing allocations.

• Within equities, we prefer mid- and small-caps given stronger earnings growth and improved valuations after the recent correction.

Turning the Page

April 2026 will likely be remembered as a month that confounded the pessimists. Global equity markets delivered a strong rebound, with developed markets rising 10%, the MSCI Emerging Markets Index advancing 14.5%, and the Nifty 50 gaining 7.5%. Mid- and small-cap segments posted double-digit returns, even as the Strait of Hormuz remained effectively shut.

Source: Bloomberg, Sanctum Wealth

Above returns are only price change in local currency terms and not total returns

As of writing, however, fault lines appear to be re-emerging in what has been a fragile, nearly month-long ceasefire between the US-Israel bloc and Iran. On the other hand, peace talks are taking place. Markets seem to be pricing in a swift resolution and the normalization of flows through the Strait. While such an outcome would allow markets to look through near-term disruptions, the risk of escalation remains, and volatility could therefore persist in the near term. On the other hand, a prolonged closure could have meaningful implications for the global economy and financial markets. Although a resolution is in the collective interest of all parties, geopolitical dynamics do not always follow economic logic, and this remains the key risk.

However, as April demonstrated, remaining on the sidelines is not a viable strategy; a staggered approach to deployment over the coming weeks remains the prudent course.

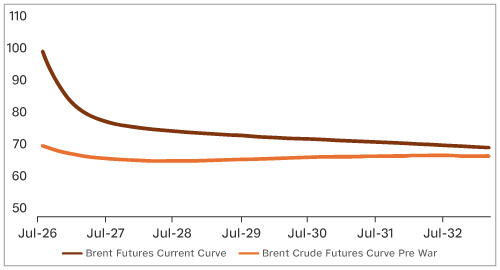

Crude futures signal a sharp price correction in coming months

Source: Bloomberg, Sanctum Wealth

Global Macro Update

Rising oil prices are beginning to weigh on global growth while keeping inflation elevated, a combination markets typically view unfavourably. That said, conditions do not yet point to a sustained stagflationary environment. If oil supply normalises and prices ease in the coming months, a severe stagflationary outcome can be avoided.

In the U.S., real consumer spending has moderated, wage growth is easing, consumer confidence has weakened, and labour market momentum is slowing. However, latest job reports suggests that the labour market momentum has softened, yet conditions do not point to a sharp deterioration as of now.

Consumer spending growth slowed to 1.6% in the last quarter, while the household saving rate declined to 3.6%, indicating that consumption is increasingly being supported by lower savings. At the margin, this raises questions on the sustainability of demand. Meanwhile, U.S. economic momentum continues to be underpinned by a narrow set of drivers, namely AI-led capital expenditure and government spending, highlighting a degree of concentration in the current expansion.

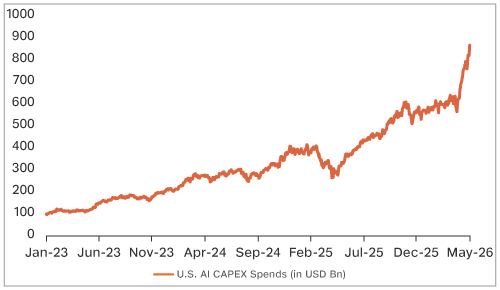

AI spends by U.S. Hyperscalers to cross USD 1tn in 2027

Source: Bloomberg, Sanctum Wealth

The Fed held rates unchanged in one of the most divided votes since October 1992, with the decision passing 8–4 and three dissenters objecting even to the easing bias in the statement. The outcome suggests a high bar for rate cuts this year amid inflation concerns.

Unlike the U.S., Europe lacks the offset of AI-led investment and significant fiscal support, leaving it more exposed to weak industrial activity and subdued demand. Its higher dependence on energy imports further amplifies the impact of elevated oil prices. While the ECB has been easing policy to support growth, persistent inflation complicates the outlook. A prolonged disruption in oil supply would deepen this challenge, entrenching weak demand alongside supply-driven inflation that monetary policy is ill-equipped to address. Germany’s EUR 500bn infrastructure and climate programme offers a meaningful structural tailwind, but its impact will materialise gradually.

China appears relatively insulated from the disruption. Beijing has moved swifty to secure energy flows, cushioning the impact of the Hormuz situation. Growth has also surprised on the upside, with Q1 GDP at 5.0% year-on-year, supported by exports and early fiscal support. That said, the recovery remains uneven. Strength is concentrated in AI and other new-economy sectors, while property and consumption continue to lag, with household confidence still subdued. Policy focus remains on supply-side priorities rather than broad demand revival. this suggests that while headline growth may hold, the underlying recovery may remain narrow.

The AI buildout remains a key driver of growth globally, and even in countries like South Korea, roughly half of the GDP growth is currently being driven by demand for memory chips. Hence, while developments in the Middle East remain a key near-term focus, global economic growth is also heavily reliant on continued AI-related capital expenditure at this stage.

Global Market Outlook

Global equities staged a strong and broad-based rally in April, led by emerging markets and Asia ex-Japan, with the U.S. and Japan also posting solid gains. The rebound was driven by two key factors: easing fears of a wider regional conflict in the Middle East and continued momentum in AI-led capital expenditure. In the U.S., gains were concentrated in AI leaders and the semiconductor ecosystem, a trend mirrored in Asia, where markets such as Korea rallied on the back of robust AI-driven semiconductor demand.

The U.S. Q1 2026 earnings season has been robust, with 84% of reporting S&P 500 companies delivering positive EPS surprises as of May 1, according to FactSet. Blended YoY earnings growth stands at a strong 27.1%, led by technology and communication services. However, the scale of AI-related capital expenditure by large technology firms is drawing increasing scrutiny. A key risk is a potential reversal in the AI trade if investors begin to question the returns on these investments.

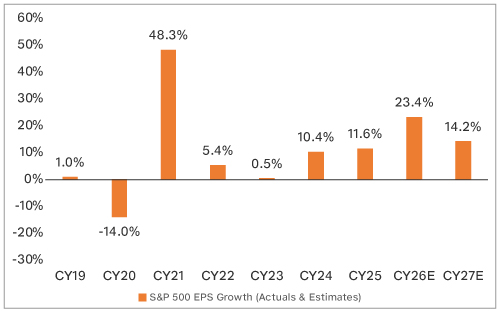

U.S. earnings growth strong

Source: Bloomberg, Sanctum Wealth

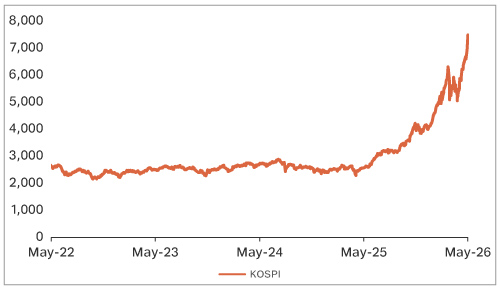

The AI-led rally has broadened to Asia, with gains in China, Taiwan and Korea largely anchored in the AI buildout cycle. In China, however, the market still lacks a meaningful domestic demand impulse. Korea’s rally has been driven primarily by Samsung and SK Hynix, both key beneficiaries of AI-related chip demand. The government’s “value-up” programme, focused on improving governance and shareholder returns, has further supported investor interest in a market that has long traded at a discount. That said, after a sharp re-rating, valuations in Korea no longer appear cheap.

Korea equities rally on AI-driven semiconductor demand

Source: Bloomberg, Sanctum Wealth

Japanese equities remain relatively resilient, supported by ongoing corporate reforms, improving domestic reflation dynamics and sustained foreign inflows. Expectations around the government’s fiscal stance add to the constructive outlook, while gradual monetary normalisation is aiding earnings momentum, helping offset near-term pressures from higher energy costs.

Global equity momentum remains closely tied to the AI-driven cycle, which has already extended beyond platform companies into the broader semiconductor and supply chain ecosystem. A further broadening into AI adopters would help sustain the rally. Conversely, any loss of momentum in the AI trade could have wider repercussions, not just for U.S. markets, but for global equities more broadly.

On the other hand, commodities continue to act as an effective hedge during periods of macro uncertainty, with broad-based strength seen both in April and over the past year. While oil, gold and silver have led gains, metals like copper have also performed well, supported by rising demand from electrification, power infrastructure and data centres, along with limited supply. Gold continues to serve as a hedge against geopolitical, fiscal and policy uncertainty, but the investment case for commodities more broadly is also improving. For Indian investors, however, access to this theme remains limited due to the lack of INR-denominated investment options, making offshore routes such as LRS a more practical way to gain exposure.

India Macro Update

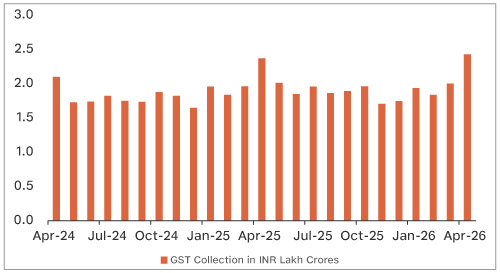

Most macro indicators continue to point towards resilient economic activity despite higher crude oil prices. High-frequency data for March and April remained encouraging, with GST collections rising to a record INR 2.4 lakh crore in April 2026. Manufacturing activity strengthened, with PMI improving to 54.7 from 53.9 in March, while services PMI also moved higher to 58.8 from 57.5. Rural demand remains healthy, reflected in strong tractor and two-wheeler sales. Meanwhile, bank credit growth has picked up to 16.9% as of March 2026, although deposit growth, at 13.5%, continues to lag despite some recovery.

India’s economic activity remains resilient

Source: Bloomberg, Sanctum Wealth

India’s CPI inflation edged up to 3.4% in March 2026 from 3.2% in February, driven largely by higher fuel prices and a modest rise in food inflation to 3.87%. Inflation is expected to inch up further in April due to elevated fuel costs. However, headline inflation remains comfortably within the RBI’s target band of 4% ±2%. Given the uncertainty around developments in the Middle East and their impact on oil prices, we believe the RBI is likely to remain on hold for now while closely monitoring the situation.

The INR depreciation has emerged as a key concern amid the current macro shock. Following weakness even before the conflict escalated and further pressure after the outbreak of war, the INR now appears meaningfully undervalued at current levels. Unless the situation in the Middle East deteriorates significantly further, the scope for sustained depreciation from here may be relatively limited.

As we had mentioned in our previous commentaries, India entered this oil shock from a position of stronger macro stability compared to previous episodes, with a manageable current account deficit, improving fiscal discipline and relatively contained inflation. This provides a better buffer against external volatility, even as higher crude oil prices remain a clear risk for growth, inflation and the currency. A swift normalization in geopolitical conditions would likely contain the macro impact, whereas a prolonged disruption could weigh more materially on growth and financial stability.

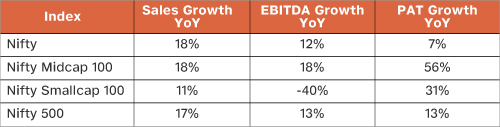

Q4FY26 Earnings Results

Q4FY26 earnings so far have been broadly in line on revenues and slightly better than expected on profitability, aided partly by low expectations heading into the season. Nifty 50 companies have reported PAT growth of around 7% against expectations of 6%, while revenue growth has remained strong at 18%. Mid-caps delivered better-than-expected numbers and small-caps posted strong but in-line results. While revenue growth was reasonable, operating leverage and premiumisation trends resulted in strong PAT growth for both mid and small-cap companies.

Q4FY26 earnings growth has been strong and in-line with estimates

Source: ICICI Securities

Earnings as of 5 May 2026 (161 out of Nifty 500 companies)

For large-caps overall earnings were weighed down by muted performance from IT majors, which saw flat to low single-digit constant currency growth. Financials, particularly NBFCs and AMCs, along with discretionary consumption, have emerged as key outperformers.

On the consumption side, both staples and discretionary companies have reported an improvement in volume growth compared to recent quarters, supported by GST cuts and channel restocking. Margins have largely remained stable despite input cost pressures, helped by strong revenue growth and limited impact of price hikes on demand. However, with the spike in crude prices largely concentrated in March, the full impact of energy price inflation and INR depreciation is yet to flow through, and management commentary suggests these could remain near-term headwinds for profitability.

So far, the impact of higher energy prices has not meaningfully reflected in earnings estimates, with the earnings upgrade-to-downgrade ratio remaining broadly balanced and keeping Nifty EPS estimates for FY26 and FY27 largely stable. However, if crude prices remain elevated for longer, some earnings downgrades cannot be ruled out. The duration and extent of the energy shock will remain a key monitorable for analysts and markets going ahead.

Equity Outlook

Indian equities rallied alongside global markets, with mid- and small-caps outperforming large caps. Within the large-cap space, the Nifty Next 50 delivered strong double-digit returns. This performance came despite heavy FPI selling through March, April and the first week of May 2026. FPIs have now sold over INR 2 lakh crore worth of Indian equities so far in 2026, taking their ownership in Indian equities to record lows. In contrast, DIIs have remained steady buyers throughout the year, supported by continued strength in retail participation. SIP inflows hit a record high of INR 32,087 crore in March 2026.

Source: Bloomberg, Sanctum Wealth

Above returns are only price change and not total returns

Following the strong rally in April, valuations have moved higher but remain close to historical averages. Q4FY26 earnings have broadly met expectations, while earnings estimates have remained relatively stable so far. Our base case continues to be that tensions in the Middle East normalise over time. Accordingly, we have gradually started overweighting equity in our asset-allocated portfolios. Within equities, we are turnings overweight on mid- and small-caps which are supported by relatively stronger earnings trends and the sharp correction seen in the broader market before the conflict escalated. Any further correction driven by geopolitical volatility could provide an opportunity to increase equity allocations more quickly.

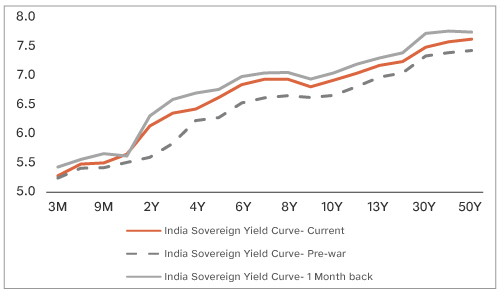

Fixed Income Outlook

Bond yields have moderated from their recent peaks but still remain above pre-conflict levels. Concerns around fiscal pressures from lower fuel excise duties, INR depreciation and rising inflation expectations have kept yields elevated. While the RBI has supported liquidity through OMOs, part of this liquidity has been absorbed through FX intervention aimed at stabilising the INR.

Bonds yields have declined, but above pre-war levels

Source: Bloomberg, Sanctum Wealth

Even if tensions in the Middle East ease, the RBI is likely to remain on hold for an extended period, limiting the scope for a sharp decline in bond yields. In this environment, taking excessive duration risk may not be rewarding given the potential for continued volatility. We continue to prefer short-duration accrual strategies, particularly in the 2–5-year segment of the yield curve, where risk-reward appears most favourable.

Within alternatives, we have seen strong gains in REITs and InvITs over the past few years and had already reduced exposure to REITs in our discretionary multi-asset portfolios earlier. We have now also exited IndiGrid InvIT. Over the last five years, the InvIT delivered returns well above what its relatively bond-like profile would typically suggest. Going forward, however, we expect returns to moderate as the interest rate cycle reverses. IndiGrid’s cash flows are largely not inflation-linked, while higher interest rates can increase interest expenses given the leverage in the structure. At the same time, investors now have access to other relatively tax-efficient options such as income plus arbitrage funds, Unifi Dynamic Asset Allocation Fund and SIFs, which may offer more stable high single-digit return potential.

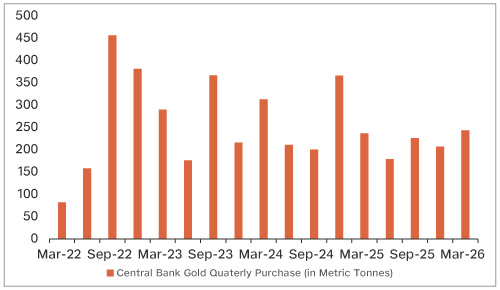

Gold and Silver Outlook

Gold remained largely range-bound in April, while silver continued to see higher volatility. In our view, the long-term fundamentals for gold remain intact. Central bank buying, which had moderated in previous months, picked up again in the March quarter.

Global central bank demand resilient

Source: Word Gold Council, Bloomberg, Sanctum Wealth

Gold as a share of reserves for emerging market central banks has risen from about 4–5% in 2010 to over 15% currently. However, this remains well below the roughly 30% average seen in developed markets, suggesting there is further room for accumulation. The Chinese central bank has continued to add gold, yet gold still makes up only around 8–9% of its reserves. Similarly, central banks in Poland, India and Brazil have also remained buyers, while still remaining below developed market reserve allocations.

Given the stretched positioning before the conflict escalated, gold did not fully play its usual role as an inflation and geopolitical hedge this time. However, we do not believe this relationship has structurally broken down. As speculative positioning normalises, we believe gold can continue to serve as an effective hedge against both inflation and geopolitical volatility over the longer term.

In the near term, gold may consolidate around current levels, but we continue to maintain a positive long-term view and believe it deserves a strategic allocation in portfolios.

We suggest avoiding silver given silver’s significantly higher volatility. The supply-demand imbalance in silver is also beginning to narrow, which could limit upside going forward. In addition, a slowdown in global growth could weigh on industrial demand for silver, while mine supply has also started to improve.