MARKING THE HEADLINES

Humble SIPs rush in as HNIs begin their exit

Live Mint, Dec 16, 2019

• The number of SIP folios has increased since April, with about 29.4 million folios active at the end of November

• Systematic investment plans are likely to keep the mutual fund fire burning for sometime, at least among small investors

Systematic Investment PlanHigh Net Worth IndividualMutual Fund

Mumbai: Stock investments are subject to market risks and historically, flows into equity mutual funds tend to taper off when risks are perceived to be high. But, ever since the systematic investment plan (SIP) phenomenon gained momentum, some of these long-established norms are being tested.

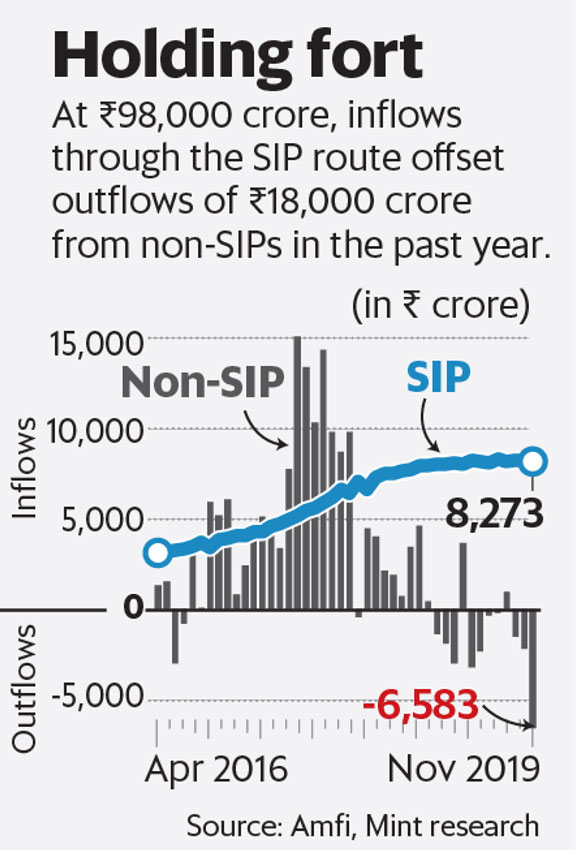

Smaller investors are continuing to invest in the market through SIPs, resulting in a net positive inflow into equity funds. But here is the troubling bit. High net worth individuals (HNIs) are increasingly redeeming their mutual fund holdings. Latest data from the Association of Mutual Funds in India shows that SIPs have garnered about ₹8,278 crore in November. Net inflows into equity funds, though, dropped to about ₹1,311 crore. The difference between the two amounts, seen as a rough proxy for non-SIP investment flows, works out to a net outflow of nearly ₹7,000 crore in November.

Mutual fund distributors and industry executives say this largely comprises redemptions by HNIs.

So why are some large investors cashing out? Big investors are perhaps getting a tad frustrated with many fund managers for not being able to outperform benchmark indices in a big way. The mean return of large and mid-cap funds has been 9.7%, while for mid-cap funds it has been just 1% in the past one year.

“Macroeconomic data continues to be weak. Therefore, there is a disconnect between the performances of the real economy and the financial markets,” said Vishal Dhawan, founder of Plan Ahead Wealth Advisors. “Many investors who put in lump sums are pulling out as their funds are not doing well, or they are worried about the economic situation. That’s why net inflows have reduced.”

Even with SIPs, growth seems to have plateaued as inflows have not increased in a major way for several months. For instance, SIP inflows at the beginning of this fiscal were about ₹8,238 crore. In November they increased by only about ₹35 crore to ₹8,273 crore. Dhawan attributes this slack in SIP growth to the stress in the economy and on the job front. “You are seeing some stress on the employment side and, therefore, the ability of households to invest has reduced. Besides, salary growth has not been happening, which means there is not much investible surplus available for investors,” he said.

Fund managers have been found wanting, especially after the reclassification of equity funds, according to Prateek Pant, co-founder and head of products and solutions at Sanctum Wealth Management. “Last month, we have seen outflows in four of the 10 equity categories such as thematic and value.” Earlier, fund managers could follow a so-called index hugging strategy to ensure it does not underperform the benchmark. This has become difficult in some categories after the reclassification exercise.

Between them, value and contra funds and thematic funds saw outflows of nearly ₹1,600 crore. The mean one-year performance of value-contra funds has been about 2%. For thematic funds it is about 6.9%. In the current market, funds with a concentrated portfolio are doing well as the market rally has been restricted to a few stocks. However, as the number of funds is restricted to one per category, the ability of fund houses to run a concentrated portfolio to suit the market is restricted.

Higher inflows into large-cap funds are making scheme sizes of these funds larger that naturally drives fund managers to run a benchmark-hugging strategy, which results in them mimicking the portfolios of the indices. This does not add much differentiation to their portfolio strategy.

Some large investors looking for differentiated investment themes are moving to portfolio management services or alternative investment funds.

Small investors prefer SIPs. The number of SIP folios has increased since April, with about 29.4 million folios active at the end of November. About 1 million SIP folios are added every month, while 500,000 SIPs folios on average are being discontinued.

Last month, the average investment amount in SIPs was down to about ₹2,810 per folio a month from ₹3,100 in April. “What distributors have realized is that managing investor expectations can be more easily done through a SIP than a lump-sum,” said Sunil Subramaniam, managing director and CEO of Sundaram Mutual Fund. “Given the outlook, distributors may not have the same degree of conviction to make lump sum investments. Hence, they are telling investors to stagger their investments.”

SIPs are likely to keep the mutual fund fire burning for sometime, at least among small investors. “Around 65% of the industry’s SIPs have been contracted for five years and more,” said Subramaniam. “So money flows will continue. At present, there is some profit-booking, but with the alternatives, real estate and gold, not giving returns, large lump sums will come back to mutual funds once they see the stock market performing.”