Apr 15, 2026

• The Middle East conflict remains a near-term market trigger.

• Higher oil prices may weigh on Indian corporate earnings in the coming quarters if geopolitical tensions re-escalate.

• Equity valuations have moderated, time to reduce underweight.

• Bond yields could remain volatile; shorter-duration instruments are preferred.

The Epic Flip Flop

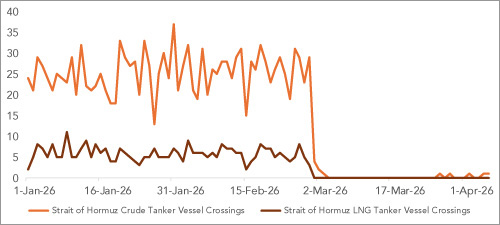

Talks over the weekend between the U.S., Israel, and Iran have broken down, following a brief two-week ceasefire between the warring sides. While the truce provided some respite after a period of escalating tensions, the Strait of Hormuz remained largely restricted despite the pause. With negotiations now failing, the situation has turned fragile again, and uncertainty continues to persist.

The near closure of the Strait of Hormuz has had a significant impact on global energy prices, the broader economy, and financial markets—developments we examine in the sections that follow.

Strait of Hormuz near fully closed

Source: Bloomberg, Sanctum Wealth

Impact of Middle East Conflict

The conflict has caused material disruptions in the supply of oil, helium, and fertilizers, affecting much of Asia (ex-China) and Europe economically. While the ceasefire should ease some of the pressure, even as the war de-escalates into a lower-intensity conflict, the next couple of quarters are likely to remain impacted.

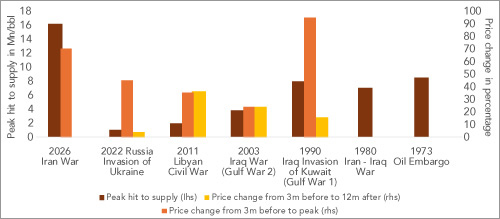

Tail risk will persist. Alternative supply routes offer limited relief. The Saudi and UAE bypass pipelines together can redirect only about 1.8 mb/d, a fraction of the potential disruption. Strategic petroleum reserves (SPRs) can cushion the shock for a few weeks, but logistical constraints limit the speed of withdrawals, and governments are unlikely to fully deplete reserves given tail risks.

This leaves demand destruction as the primary balancing mechanism if transit through the Strait were to remain disrupted. Historically, meaningful demand adjustment has required sharply higher prices, and analysts believe oil may need to rise well beyond the 2008 peak of ~$150/bbl to materially curb consumption and restore equilibrium in the current environment.

Historical oil supply hit across different crisis

Source: Goldman Sachs GIR, IEA, ICE

From Goldman Sachs Top of the Mind Report dated March 20, 2026

In the most adverse scenario, the conflict escalates again, reaches new heights, and damages critical energy infrastructure. The consequences could be long-lasting, as restoring production may take years, and some supply losses could even become permanent. In this situation, the energy shock would extend well beyond oil and gas prices, potentially triggering a global recession through sustained inflation, supply shortages, and a sharp slowdown in economic activity. Global financial markets would face significant downside risks under such a scenario. However, at this stage, the probability of this extreme outcome appears relatively low.

Global Macro Update

Global economic data increasingly points to a more challenging macroeconomic environment ahead. Growth in the U.S. and Europe is expected to soften, while China’s recovery is grinding slowly.

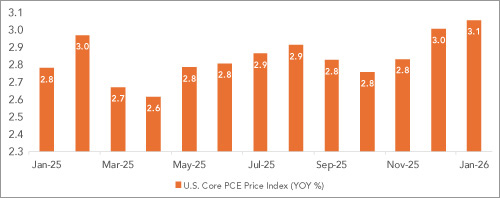

While the U.S. March jobs report surprised on the upside, overall hiring momentum has remained weak, with little expansion in employment since last April. Other labour market indicators, including long-term unemployment and wage growth, suggest a gradual but clear softening in underlying conditions. Easing of rates needs to be temporarily paused as the ongoing Middle East crisis adds a significant layer of uncertainty, making monetary policy decisions more complex.

U.S. core inflation above target and already rising

Source: Bloomberg, Sanctum Wealth

Accelerating inflation owing to higher energy prices in Europe is renewing stagflation concerns. Similar to the Fed, the ECB now faces a difficult trade-off: tightening policy to anchor inflation expectations risks further slowing an already fragile economy, while delaying action could allow energy-driven price pressures to become entrenched.

China, by contrast, showed a modest improvement in factory activity toward the end of the quarter, with manufacturing PMI returning to expansion and broader business indicators strengthening. However, the recovery remains fragile and policy-dependent. If geopolitical tensions resurface, the recovery is likely to remain gradual and uneven rather than durable.

The global economy was resilient before the conflict, though growth was modest, and with inflation easing, most central banks had maintained an accommodative stance. If the war and consequently higher energy prices persist, slowing growth will increasingly dominate the policy agenda, further challenging central bankers’ decision-making.

Global Market Update

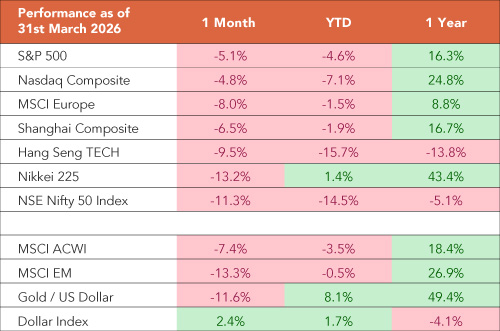

Global equities corrected last month, with declines largely reflecting the impact of higher energy prices. The U.S., a net energy exporter, saw limited losses, while energy-importing markets, Japan, India, Europe, and South Korea, experienced sharper corrections. Emerging markets underperformed developed markets overall, though energy exporters like Brazil held up in local currency terms. If the conflict persists, such divergences are likely to continue.

Source: Bloomberg, Sanctum Wealth

Above returns are only price change and not total returns

The U.S. dollar strengthened on safe-haven demand, even as broader structural questions persist. Emerging market currencies, hit by a stronger dollar, higher energy prices, and a risk-off mood, saw sharp declines.

India Macro Update

India entered the Middle East conflict on a relatively stronger macro footing, with economic activity gradually recovering and inflation well below the RBI’s 4% target. However, the surge in energy prices has introduced fresh uncertainty. It is widely expected that the impact of higher oil costs could filter through the economy post some of the key state elections. For now the government announced a INR 10/litre excise duty cut on petrol and diesel, keeping retail pump prices largely stable.

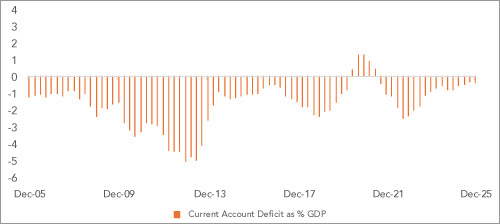

We are therefore likely to experience inflation with a lag. Also, an adverse base effect is expected to kick-in. The current account deficit may drift toward ~2% of GDP, elevated, but still well below the ~5% peak seen during the 2013 taper tantrum. Meanwhile, the INR has weakened over the past year and appears undervalued on a REER basis.

India’s CAD to widen but likely to be below taper tantrum levels

Source: Bloomberg, Sanctum Wealth

The excise duty cut hurts the exchequer. Higher urea, phosphate, and gas prices are also expected to push up fertilizer subsidies. Second-order effects, such as weaker tax collections from slower growth, could further strain government finances. Estimates suggest that every month of oil prices near USD 100/bbl could add roughly INR 30,000 crore to the fiscal burden, highlighting the sensitivity of India’s fiscal position to sustained elevated crude prices.

Like other central banks, the RBI faces a delicate balancing act: anchoring inflation, maintaining currency stability, and supporting growth. In the near term, we expect the RBI to prioritize inflation and the currency, keeping rates on hold till there is more clarity.

Equity Outlook

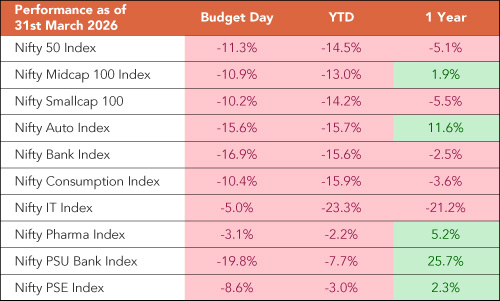

Indian equities have fallen over 10% in March 2026. Year-to-date, the Nifty is down around 15%, while mid- and small-caps have held up slightly better, reflecting the underperformance of large-cap-heavy sectors like Banks, Auto, and FMCG.

Source: Bloomberg, Sanctum Wealth

Above returns are only price change and not total returns

Looking ahead, the full impact of higher energy prices is unlikely to be visible in the upcoming earnings season, as OMCs absorbed part of the pressure and retail fuel prices remained stable. However, earnings estimates are expected to be downgraded. Goldman Sachs estimates that a USD 45/bbl increase in oil prices for three months could lower earnings growth by nearly 9%. FY27 earnings, earlier expected to grow in the mid-teens, could now slip to single digits if oil prices remain elevated, raising the risk of back-to-back years of muted corporate earnings.

Weaker earnings and a deteriorating macro backdrop could also delay the return of foreign investors. Foreign portfolio investors (FPIs) have already sold a record USD 42bn since the September 2024 market peak, with March alone witnessing nearly USD 12bn of outflows, the highest monthly outflow in India’s history.

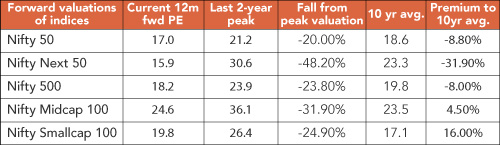

The valuations have come down and are now below historic averages. There may be some reduction earnings expectations, but for now the base assumption is that even if the conflict re-ignites, the kinetic action may not last very long. Therefore, this could be an opportune time to add to equities. Since, volatility is unlikely to subside any time soon, we suggest staggering addition over 6-8 weeks. Mid- and small-cap indices, which were already lagging large caps before the conflict, have corrected sharply. We recommend gradually overweighting them.

Source: Bloomberg, Sanctum Wealth

Fixed Income Outlook

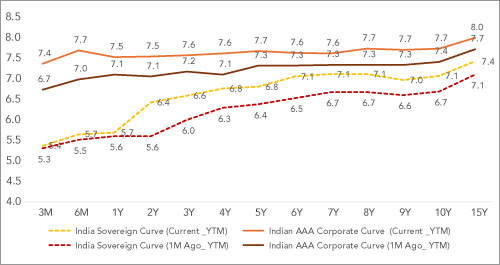

Indian bond yields have risen across the curve, tracking global trends, with the increase most visible in money market rates, short-term government securities, and corporate bonds. Fiscal concerns and tighter liquidity have driven the move. Although the RBI injected significant liquidity between December 2024 and March 2026 via CRR cuts, OMOs, and FX swaps, much has been absorbed by currency leakage and capital outflows, leaving system liquidity modest.

Bond yields across the yield curve have moved higher

Source: Bloomberg, Sanctum Wealth

Bond yields are likely to remain under pressure if the conflict re-escalates, resulting in fiscal pressures, persistent inflation, and a weaker rupee. Meanwhile, the RBI is expected to maintain a cautious, wait-and-watch stance. In this environment, we prefer locking into higher yields but continue to stay away from duration.

Gold and Silver Outlook

The recent surge in gold and silver was largely driven by euphoria and speculative demand. This explains the recent movement where it did not act like a safe haven but corrected sharply along side equities.

A stagflation-like environment in large parts of the globe, driven by higher oil prices, should benefit gold. Near-term volatility is likely, but we continue to view gold as a strategic allocation for long-term portfolio protection and diversification. We recommend that investors underweight in gold consider adding gradually, while those with adequate allocations should maintain their positions.

In contrast, we remain cautious on silver. Its industrial demand is cyclical and likely to slow if global growth softens, and it has already shown signs of weakening due to price sensitivity. At the same time, silver mine output is rising, and the supply-demand gap is expected to narrow through 2026–27. Given silver’s high-beta nature, we recommend limiting exposure unless investors have a high-risk appetite.

Overall, we have moved from cheering for cash to carefully allocating to equities and high yield debt.