Jun 11, 2024

• Geopolitical challenges so far have not stirred exaggerated volatility in the equity markets

• India’s election results, an initial shock, but likely still constructive for markets

• The bitterness of US elections to increasingly worry markets as the months go by

• The 80 year cycle of “The Fourth Turning”

• Europe challenged by the ‘right’ but still staying centrist

We – and many others – had always seen 2024 as a year when the political cycle of elections would prove potentially challenging for the markets. Elections in the world’s two largest democracies in these past days – India and Europe – have both sprung surprises and hope as far as markets are concerned. The build up to the US elections later this year has thrown up many stress points that are only antagonising both sides of the political divide.

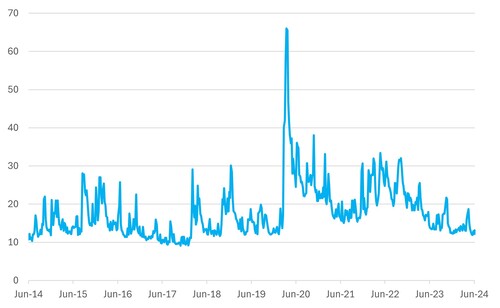

Translating politics into potential outcomes for asset classes is always a hazardous call. Maybe the easiest conclusion to draw is that the current volatility in the US equity market looks out of sync with reality.

Chart 1: US Equity Market Volatility Index Close to Lows

US VIX Index

Source: Bloomberg

India – It’s no disaster, it’s democracy

A third successive term for Prime Minister Narendra Modi was never going to be easy; global political history is replete with instances where prime ministers struggled during their third term, with Margaret Thatcher being a notable example. The BJP, the party that Narendra Modi represents, will need to navigate challenges and setbacks, but it will likely forge deals state by state to ensure continuity.

We expect the Indian stock market to remain resilient despite its stretched valuation.

Typically, a burst of popular policymaking aligns with bull markets unless the government compromises growth with higher inflation and/or a weak currency. We believe Prime Minister Modi will not squander the structural progress made over the past eight years. However, given the current circumstances and compulsions of coalition politics, broader populism is clearly necessary. The good news is that India can afford a phase of populism. Government finances are in good order, and the independence of the Reserve Bank of India, the country’s central bank, will ensure responsible handling of any fiscal overreach that might create inflation.

We anticipate that PM Modi will provide targeted relief to the agriculture sector and enhance plans for job creation, particularly in manufacturing. The lack of quality job creation in the manufacturing sector and the low levels of highly paid jobs in the services sector are holding back income growth and the general well-being of the middle class. According to current projections, the middle class is expected to reach 41% of the country’s population by 2031. A growing middle class will certainly not like to be merely exploited as a source of cheap labour. Rather, it will expect its aspirations to be fulfilled by the government’s conscious efforts on, for instance, creating avenues for more investments into the country.

Active equity funds in India may find life easier in the coming years. Recently, active managers have experienced broad-based underperformance, which contrasts with the historical trend of consistent outperformance by market gurus in the Indian equity space. Much of this historical outperformance has come from judicious stock-picking in the mid- and small-cap sectors.

If the new Modi government focuses on boosting consumer spending with subsidies in the agriculture sector and supporting income gains for the middle class, domestically focused small- and mid-cap stocks that have underperformed could see a significant catch-up. This renewed focus on consumer spending and income growth could provide the necessary tailwind for active equity funds to regain their historical outperformance.

US elections a major concern

Thankfully, India, the world’s largest democracy, was never going to deliver results that would lead to a wobble in global markets. But the exercise may have redrawn investors’ focus to the United States where elections are due at the end of the year. Although the polls have seen a marginal narrowing of the gap between Donald Trump and President Biden, the most likely outcome remains a new Trump administration. The inability of the US presidential election to be a catalyst for any kind of public debate about the need for fiscal consolidation through spending cuts and tax increases is worrying. This past week the IMF reemphasised its worries about the lack of progress on deficit reduction – in April it forecast a 2025 US fiscal deficit of 7.1% of GDP. Donald Trump is currently committed to making 2017 tax cuts permanent.

Meanwhile, Trump also threatens revenge on his domestic rivals – many commentators may see those developments as merely a reflection of his bombastic nature, but at some stage the markets may worry that the events could impact the country called the ‘leader of the free world’. The trashing of the judicial system, for instance, could jeopardise law and order. As Ian Bremner, the notable political analyst pointed out at the start of 2024, ‘no matter who wins, many Americans will not accept the legitimacy of the US election’.

Donald Trump may also backtrack on the US commitment to support Ukraine. Such an outcome could lead to the early capitulation of the Ukrainian armed forces who are already struggling to contain Russian advances. A fully armed and belligerent Russian force could then be sitting at the doorstep of Europe at a time when leadership in Europe seems to be at sea. The EU elections are again bringing a real assortment of political strands pulling in different directions. Meanwhile in the UK Prime Minister Rishi Sunak seems to be doing everything possible to ensure he loses the election badly. The curtailing of his visit to the D-day landing memorial to film an election TV skit beggar’s belief.

Europe – On an 80-year cycle?

In a week when leaders commemorated the 80th anniversary of the D-day landings when Allied forces moved to crush the Nazi forces, it is a sad irony that the EU elections have delivered results that indicate a sharp move to the right in European politics. The 80th anniversary packs a lot of symbolism. In 1997, William Strauss and Neil Howe published the book “The Fourth Turning”, which details how history moves in 80-year cycles. Strauss and Howe’s hypothesis states that US history moves in 80-year cycles – four generations of 20 years – with each generation moving through a 20-year period of influence. The four cycles were named High, Awakening, Unravelling, and Crisis. While we analyse that hypothesis, it would be not be an exaggeration to ascribe the word ‘crisis’ to Europe’s current political situation. The previous Brexit event was undoubtedly an upheaval, but various lurches to the right in several European countries were further evidence that all was not well. A war in Ukraine can only be deemed a crisis.

The good news from the EU elections is that the mainstream parties of Christian Democrats and Socialists remain the dominant force; however, the rise of the extreme right parties is a concern. The rise in the share of the vote of the right-wing parties in France has led to President Macron calling early and rapid national elections. The National Rally party of Marine Le Pen won more than 30% of the votes, about twice as much as Macron’s European centrist Renew party. In Germany, the extreme right party of AfD became the second-largest party ahead of Chancellor Scholz’s Social Democratic party.

The European equity markets have understandably reacted with some trepidation to the election results. However, we suspect that the angst should dissipate as investors become more comfortable that the mainstream parties will continue to hold the whip hand on policy making.