May 28, 2024

• Market debate remains on stickiness of inflation and slow pace of US rate cuts

• US market concentration in big tech signals potential problems, but the sector continues to deliver

• Old economy stocks struggle

• UK’s Independence Day general election

US bank leaders’ statements of caution

We generally don’t echo the opinions of others’ in the market. However, in the past week, we’ve been struck by comments made by the CEOs of JPMorgan and Goldman Sachs about the current state of inflation and future rate cuts.The market’s performance continues to swing between the view that the Fed will cut rates as soon as there’s any clear sign of slowing growth or inflation unexpectedly trending downwards. On our part, we have consistently stated that inflation will remain stubbornly low and that the Fed will be slow to cut interest rates.

Last week, Jamie Dimon of JP Morgan Chase stated that investors are underestimating the strength of inflationand the potential for the Federal Reserve to raise interest rates. JP Morgan also suspended a share buyback program, indicating that the bank’s stock price at 2.3x book value seems fairly valued.

Joining Jamie Dimon in presenting a more sober view of the US economic outlook was the CEO of Goldman Sachs, who appeared more candid in his assessment, suggesting that the US central bank may not cut interest rates at all in 2024.He cited the significant increases in government spending and the general commitment to investments on AI as two decisive factors leading to a less interest rate-sensitive economy than we have seen in the past. Hence, it is taking higher interest rates than we would typically expect to bring about a slowdown in the economy.

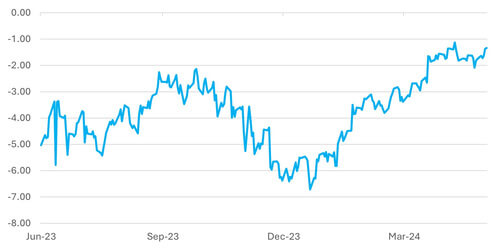

Chart 1: Market Trims Expectation for 2024 Rate Cuts Back to Approx. Just One

Source: Bloomberg

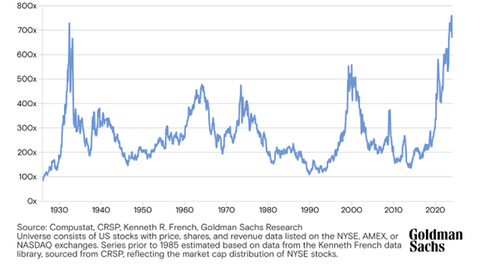

The risks of concentrated markets

On a related note, Goldman produced a detailed chart on the highly concentrated nature of the US equity market.Several media reports covered the story by implying that a 1930-like collapse is potentially around the corner – something that we don’t agree with. However, the marked outperformance of some of the largest stocks is emblematic of the narrow focus of growth in the economy (Chart 2).

Chart 2: Ratio of the Market Value of the Largest US Company to the 75th Percentile Stock

Source: Bloomberg

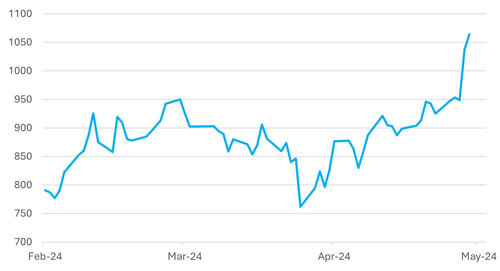

The story is about the tech revolution that continues to benefit from a structural acceleration in the advancement of AI. Meanwhile, we witnessed another set of impressive quarterly results from NVIDIA ($1064) last week. As is usual with these kind of growth stocks, target prices tend to move in tandem with the market price; hence, analysts on average have a target price of $1160.

Chart 3: NVIDIA’s Results Surprise…Again

Source: Bloomberg

We remain overweight tech (by design) in our model portfolios.We are of the view that investors should maintain a distinct holding in the tech sector. In the first instance that would be by including a line in the strategic asset allocation for the NASDAQ index. Based both on historic and projected returns a distinct line for tech stocks adds to the quality of the portfolio with a higher expected return and lower risk.

Old economy still challenged

The outperformance of tech also reflects the weakness/modest underlying growth of the old economy and the challenges from inflation on the spending power of low- and medium-income households.

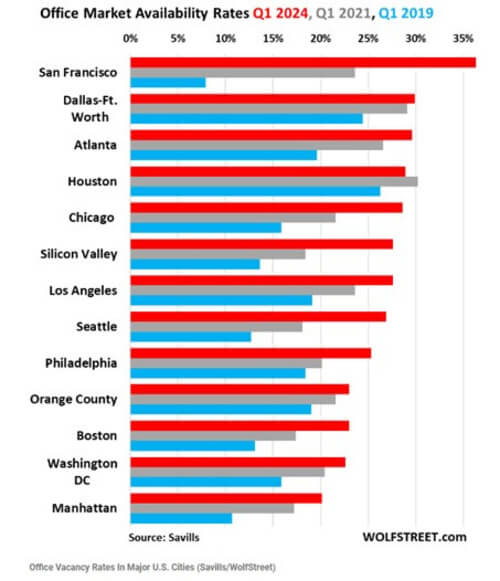

The bifurcated market in the US is particularly evident in the newsflow from the property sector. While the tech sector is enjoying upgrades to profit forecasts, the real estate market is facing serious headwinds. The latest data for commercial real estate shows further increases in US commercial real estate vacancy rates in major cities. In fact, only in Houston has the occupancy rate increased over the past year.

Chart 4: Vacancy Rates in Major US Cities

Costco’s quarterly results this week will provide another perspective on how US retail sales are holding up. The previous US retail sales figure was very disappointing and last week’s worse-than-expected earnings report from Target Corp didn’t help sentiment. The stock consequently fell 7% by the end of the week. The company admitted that it was having to cut prices to encourage cash strapped consumers to spend.

The UK’s “Independence Day” general election

With the UK economy still struggling from the fallout of the country’s “independence” from Europe in the form of Brexit, it is ironic that the UK will go to polls on the day the US celebrates its independence from the UK. With the benefit of hindsight, we can certainly conclude that the US’ break for freedom has been a smoother affair than that of the UK from Europe.

UK Prime Minister Rishi Sunak surprised the pundits last week by calling for a general election on 4th July, far earlier than expected. There are various rationales as far as the timing is concerned. Inflation, at 2.3% year-on-year in April, is finally within a whisker of the Bank of England’s target, and the UK has just exited a shallow recession. A perception holds that good news will be sparse in the future – a sticky service price inflation, for instance, undermines the chance of an early interest rate cut, and the latest public sector borrowing estimates effectively rule out any pre-election giveaway.

The Conservatives’ chances of returning to government look dire indeed.The Economist magazine’s model has the party’s probability of winning the most significant number of seats (but still short of a majority) is at 1%. The widely expected outcome is that Labour will return to power after 14 years with a working majority. Investors cry out for a stable governing majority with a clear mandate. As likely, Sir Keir Starmer, the Labour Party leader and the likely prime minister, is taking a cautious line in framing the election manifesto – commitments on workers’ rights, for instance, have already been diluted to quell business concerns. A majority of more than 60 seats looks like a hard ask, but Scotland will be crucial. Here, Labour looks to be the primary beneficiary of the collapse in popularity of the Scottish Nationalist Party. So far, at least, sterling has remained steady. The more interesting topic is any potential for a long-awaited re-rating of the local stock market post-election.

Over the past month the UK equity market has performed well, closing some of its perennial underperformance of the past few years. The bid for Anglo American and the run up in interest rate-sensitive sectors such as housebuilders has helped push the index higher in the absolute, and relative to the global index.

Chart 5: UK Equity Market’s Recent Outperformance

Source: Bloomberg