Nov 27, 2017

“I have a high tolerance for pain” – Elon Musk

Elon Musk’s quote has relevance to this week’s commentary. There’s been an ongoing debate about index valuations and forward return expectations. To gain some insight, we study the past 8 years of index returns versus the rest of the market, and put to test the common refrain that small caps – and to a lesser extent mid caps – are risky and should be avoided. Along the way, we review sectoral and stock specific data for additional insights.

Market Capitalization

Index Returns Since 2010 Are Much Lower Than the Broader Market’s Performance

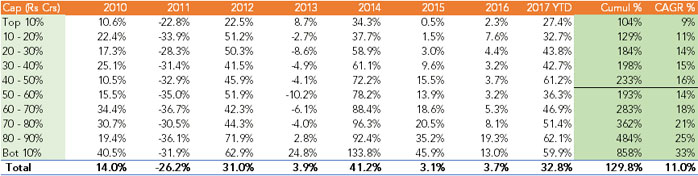

We categorized the CNX 500 at the beginning of each year by market cap into 10 buckets. What’s clearly evident in the table below is that investing in smaller cap stocks has proven tremendously profitable.

The Largest Decile Has Delivered a CAGR of 9% Versus the Smallest Decile a CAGR of 33%

The absolute return from the largest 50 stocks in the CNX 500 is a paltry 9% per year, since 2010. Individual year returns are also provided in the table below. The largest decile had three good years and five sub par years.

In comparison, mid caps – represented by deciles 3 through 6 – have delivered respectable CAGR ranging from 14% to 16%. Finally, small caps – represented by deciles 7 – 10 – have delivered a CAGR of 18 – 33%. Further, the returns are well diversified and not the result of any outliers.

Additionally, the smaller the cap, the larger the return. Returns rise from 9% for the largest decile, to 33% for the smallest. Individual year returns by decile also display the same trend. Given the perception of risk and volatility associated with small caps, one would expect the downside volatility of small caps to be significantly high.

While the Largest Decile by Market Cap Delivered a CAGR of 9%…

… Mid Caps Have Delivered a CAGR of 15%…

And the Smallest Decile Has Delivered a CAGR of 33%

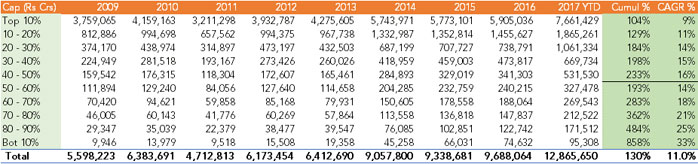

Investing 1 Crore in the Top 100 Stocks in the CNX 500 Would Have Grown to 2.2 Cr in 8 Years…

…If Invested in the Bottom 100 Stocks, It Would Have Grown to 7.7 Cr

However, small caps had only one negative year of performance, 2011, and the 31.9% loss of the smallest decile was quite reasonable relative to the 22% drop in the largest decile. Cap appears to have a strong negative correlation to returns. Surprisingly, the 31.9% is lesser than or in-line with most other deciles.

Clearly, the Market’s Preference For Large Caps Appears to Be Driven by Perceived Safety

Mutual funds structure portfolios around large caps. Research houses devote resources to large cap coverage. So does a small cap strategy lead to higher volatility?

Small Caps Are Not As Volatile As Perceived With Long Look Back Periods

Certainly, with annual reviews, the volatility of small caps is not markedly worse than large caps, and well worth taking on, given the very large upside. Longer review periods make the volatility of small caps palatable.

Value to Adding Small Cap Exposure in Portfolios

While acknowledging the study does not take into account a 100 year event like 2008, it does clearly demonstrate value in adding small cap exposure to portfolios. For risk seeking investors, with the willingness to suffer drawdowns slightly in excess of large caps, over longer look back periods, a small cap portfolio will significantly outperform its larger cap peers over longer time horizons, by large margins.

This confirms the view held by John Templeton, Peter Lynch and other legendary small cap stalwarts. To build meaningful wealth, small caps are indeed the largest wealth creators.

Next we consider what sectoral insights can be gleaned from the data. Turns out a few key ones.

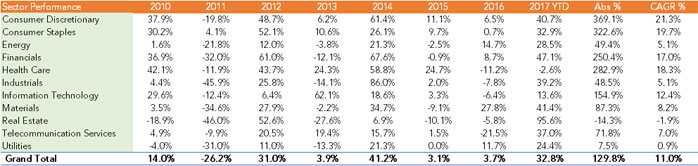

The Consistency in Performance of the Consumer Sectors Stands Out

First, the consistency of high returns by the Consumer sectors stands out. The top performing sectors are Consumer Staples, Discretionary, Health Care and Financials. All other sector returns are sub-par, with IT being only average.

Consistency & Predictability Lead to Performance

Consumer Sectors Have Delivered 20% CAGR, And Consistent Annual Performance…

…Health Care Delivered Consistent Performance But Has Faltered of Late

As investors, we seek consistent, high returns, and the data validate exposure to Consumer and Financials (ex PSU). Other sectors have delivered returns, but sporadically, and entries have to be timed.

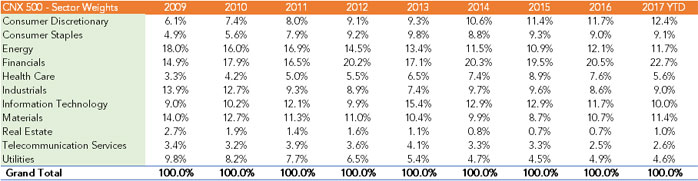

The Market Is Migrating Away from Energy Towards Services

At the start of 2010, Energy was the largest weight in the CNX 500. Since then, the Consumer sectors have roughly doubled in size. Financials ex PSU have also likely doubled. Materials appear to have seen the worst and bottomed. Health Care, despite recent pains, has grown. IT has remained steady. Telecomm has lost a third of its weight, but looks to be bottoming. What’s been decimated? Real Estate, down to 1% from 2.7%. Utilities have been unable to deliver, and have seen their representation halved.

Consumer, Financials (ex PSU) and Health Care Have Dominated Sectoral Weightings

Stock Perspective

Small Cap Performance Dominates Again

The data yet again provides a clear conclusion. In reviewing the top performers over the 8 year period, i.e., the winners and largest wealth creators, it’s noteworthy that 19 of the 25 top stocks were small caps with a capitalization under INR 460 crores.

19 of 25 Top Performing Stocks Had a Starting Market Cap Under INR 460 Cr …

…The Average Market Cap Was INR 460 Cr and Average CAGR of 61% p.a.

Key Observations and Conclusions

A few observations and conclusions can be made:

First, index returns are largely uncorrelated with small and mid cap returns over longer time horizons. During the past three years, the index has been stuck in a high valuation range, peaked at around 9,000 a couple of times and sold off and finally pushed through to 10,300. In that same time, small caps have delivered 35-45% returns in 2015, 13.0 – 19.0% in 2016, and 51-62% in 2017.

The corollary is that portfolio returns of multi-cap, mid-cap and smaller cap portfolios over longer time horizons are unlikely to be correlated with index returns.

Third, adding small cap exposure to portfolios is a worthwhile portfolio optimization exercise, as it raises expected returns without elevating an equivalent measure of risk in the portfolio over annual review periods.

Fourth, the market’s focus on the top 100 names seems misplaced, and there are obviously reasons for this. The alpha opportunity remains most evident in small caps and to a lesser extent mid caps. It would appear that nimble portfolio managers, with rational assets under management, remain better positioned for performance.

Outlook

Fixed Income

It’s been a tough few weeks in the bond market. The sharp rise in crude and the implications of rising borrowing costs, and hawkish Fed speak have spooked investors.

RBI Policy – OMO Cancellation a Relief, Rate Cuts Unlikely, Rate Hikes Unlikely

While the RBI stepping back from OMO bond sales certainly gave the market some respite, yields have again bounced back to 7% levels. While some market participants were vehement about a rate cut in December, that expectation appears to be clearly off the table. With looming pressures related to crude, inflation and market borrowings, it is highly unlikely that the RBI will stoke the inflationary fires with a rate cut. Nor can we see any case for a rate hike, which would be even more perplexing. A wait and see approach by the RBI seems reasonable and likely.

Fiscal Policy

With the Finance Minister communicating a strong intent of adhering to the fiscal glide path, one would think the markets would feel more sanguine, but the market is doing the math and challenges remain evident. With heightened risks, a heightened trading range on G-Secs seems to be the net result.

Credit Rating Futility

One development that failed to create any response in bonds was Moody’s sovereign debt upgrade. Foreign institutional investors have already exhausted their limits on domestic bond purchases.

Outlook

Fiscal risk and crude have led to the recent sell off in bonds. With regards to fiscal slippage, a substantially higher bond supply on higher borrowing would certainly be a cause for worry. However, if the slippage is to the order of what the market was absorbing via OMO bond sales, then it’s likely to be absorbed in stride. The market has absorbed INR 90,000 crores of OMO bond sales from the RBI so far. This would be equivalent to a 0.5% expansion in fiscal deficit. Thus the fact that OMOs are likely to stall from here should at least partly serve to offset any concerns around fiscal slippage.

Spreads & Positioning

With the removal of OMO supply, and spreads between 80 – 125 basis points in the under 10 year segment, we remain comfortable with our positioning in corporate bonds.

Our view from a fortnight ago remains unchanged. We favor conservative corporate bond funds, select actively managed AT-1 bonds and well-priced high yield opportunities. We’ve stayed away from duration and would continue to stay away until clarity on crude, inflation and fiscal policy emerges. At some point in coming months, duration and the long end may start to look attractive.

Equities

The analysis this week is instructive in another way. A basket of the top 100 stocks in the CNX 500 earned a mediocre 10% CAGR with three good years, 2012, 2014 and 2017. Alternatively, the bottom 100 stocks in the CNX 500 earned a 29% CAGR. To earn the additional 19% CAGR, all one had to do was be willing to accept an additional 5.7% downside in 2011.

Further, the annual average upside differential in returns between small and large caps is in the double digits. With the exception of 2011, small caps returned at least 13.8% each year.

Smaller Cap in the CNX Has Outperformed Large Caps By At Least 11.2% Each Year Except 2011…

Many Ways to Skin a Cat

Pardon the gory cliché. Stock selection is the third arrow in an investment manager’s arsenal, alongside asset allocation and sector. While there are many ways to earn outsized returns, small caps deserve a place in equity portfolios, obviously according to risk appetite. Mr. Musk’s refrain is meaningful. To achieve outsized performance, some tolerance for pain is necessary.

Index returns are likely to be mediocre from elevated levels. We note, though, that valuations have remained high and index returns remained mediocre for 3 years now. In that same time, small and mid caps have continued to deliver strong performance, as evidenced in the study.

We expect much of the same going into 2018.

Structural Bull Market Remains Intact, Reform Multipliers Ahead, Crude on the Watch List

What’s not being recognized by market participants is that government reforms are likely to kick in meaningfully over the next few quarters. A spike in crude remains a worrisome albeit, low probability event, with painful consequences should it occur. Government response will be critical. Until then, the structural bull market continues apace.

We end with this thought. A patient investor that rebalanced their portfolio annually, could simply buy the bottom decile and earn 29% a year. There is definitely something to be said for a buy it and forget it approach and for not getting too caught up in index performance.

Technical Outlook

A positive week for the market with the Nifty50 gaining for the seventh consecutive session to close at 10390 up by a percent for the week. Index was facing resistance around 10360, but managed to close above marginally in Friday’s session. Now recent rising gap low of 10230 levels will be the immediate support for the market. In Nifty options, strike price 10300 put has highest open interest and will act as support for the market. Thus, index has support at 10260-10230 levels. Holding above 10230 levels index can rally towards 10540 and then 10650 levels on the upside. But in Nifty call options, strike price 10500 has the highest open interest which will act as resistance in the near term for the market. Thus, heading into November series expiry this week, market is likely to trade in a range between 10230-10500 levels. Below 10230 level, 10085-10000 zone is an important support for the market. After couple of months selling, FIIs turned net buyers in equity segment last month and continue to be buyers this month also with nearly Rs. 16,000 crore inflows. But in index futures they have been net sellers in November series suggesting hedging of long positions. While Domestic institutional flows continue to be strong and support the market. INDIA VIX measure of volatility has increased this month by 8.6% to 13.71 levels and holds above 13 levels. Thus, further spike in VIX will be cause of concern and can lead to pressure in the market.

Nifty Daily chart