Jul 9, 2018

“Buy when most people, including experts, are pessimistic, and sell when they are actively optimistic” – Ben Graham

Equities

What’s Leading to the Surprising Uptick in Domestic Growth

While investors have been focusing on a slew of worries ranging from a U.S. China trade war, central banks withdrawing liquidity, FI outflows, a flattening yield curve in the U.S., to crude oil, a depreciating Rupee, RBI rate hikes, inflation and valuations, the recent economic data has been surprisingly resilient. PMI manufacturing and services are at multi-month highs, credit to the retail and services sector continues to grow double digits, automobile and commercial vehicle sales remain surprisingly strong, cement demand is surging and travel and consumption trends remain strong.

What’s leading to the surprising uptick in economic data?

A Third Attempt at an Economic Growth Breakout

Structural forces clearly appear to be at play. The PMI Manufacturing chart below highlights that the two slowdowns in the past couple of years came due to demonetization and GST, and aborted smart pickups in growth each time. This is the third time in three years that economic growth is spurting ahead, this time aided by the reforms implemented by the government.

Despite growth in the global and domestic economy, equity investors remain focused on the risks. Are investors falling victim to negativity bias? Negativity bias is a human tendency to over-react to negative events, and studies have highlighted the human brain reacts more strongly to negative events than positive stimuli.

Structural Factors

What’s clear is that consumption is driving growth in India. Drivers, maids and delivery boys are purchasing smartphones costing INR 10,000 and higher. This wouldn’t have been possible as recently as 3 years back. It’s safe to say this story is repeating itself around the country. Disposable income is rising for the BOP (bottom of the pyramid), alongside the availability of credit, and is expanding consumption. Emerging India has genuine aspirations and is now able to fulfill them.

The Jio Effect

Access to smartphones has democratized access to information. We refer to this as the Jio Effect, and it has helped democratize access to information and drive consumption and economic growth. Rural consumers can order goods from e-commerce sites and the availability of online information is a great equalizer. While we may debate the job growth numbers, the workforce is growing and driving GDP growth.

Manufacturing and Services PMI Are in a Third Attempt in Three Years at an Upside Breakout…

…Hindered in the Past by Demonetisation and GST

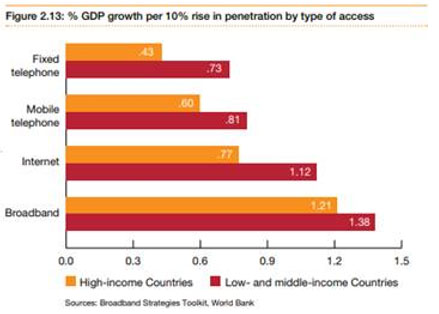

Every 10% rise in penetration by smart phones, internet, and broadband raises GDP growth by an average of 0.8%, according to a PWC research report. We call this the Reliance Jio effect in India. Reliance has been a godsend in accelerating Indian economic growth.

Online penetration Is Contributing to GDP growth

Highway connectivity is also correlated to growth. States with high connectivity such as Maharashtra, Tamil Nadu, Gujarat, Kerala, Karnataka experienced growth rates of 8.5% to 11% in the past decade, while states such as Assam, Himachal, Orissa, J&K, Uttarakhand with limited connectivity averaged less than 7.0%. A massive investment in infrastructure will yield benefits, alongside productivity benefits of GST and move to an organized economy.

Auto sales have surprised investors. When viewed from a demographic perspective, it’s not surprising. Passenger car ownership in India is roughly 50 cars per 1000. China has 154 cars per 1000. It’s bound to rise for many years. Home and appliance purchases are likely to follow similar trends. By 2025, India’s workforce will be larger than China’s.

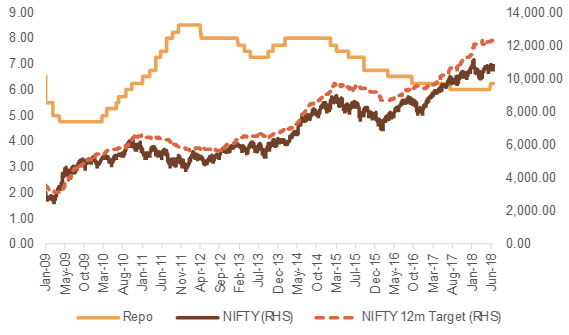

Minimal Rate Hikes by RBI Looking More Like 2013 Than 2010-11

While rate hikes are a headwind for the economy, when hikes are pre-emptive on rising inflationary pressures, positive benefits accrue to investors and savers in real terms. It is sustained rate hike cycles such as those witnessed in 2007 and 2010-11 that lead to a marked slowdown in economic activity and a bear market, as witnessed in 2011 and 2008. By comparison, the Nifty 50 consolidated in late 2013 before exploding to the upside in 2014.

While Sustained Rate Hike Campaigns Are Negative for Equity Markets…

…The Current Hiking Campaign Looks More Like 2013 Than 2010-11

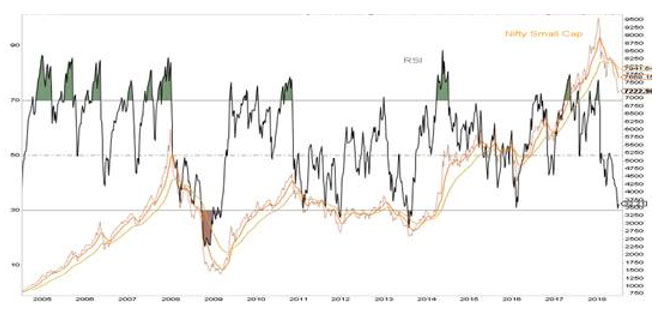

The Nifty Small Cap Index is Down 24.4% From It’s Highs in Late January…

…the Severity of the Selloff Is Approaching Past Cycle Troughs

Midcaps Are Down 16.2% YTD But Up +176% Since 2014

Meanwhile, the Nifty 50 Remains Amongst the Top Performing Indices in the World…

Similar to 2013, We’ve Had A Sharp Selloff Already and a Bear Market in Small Caps

While it feels like the markets are at highs, the reality is quite different. The market indices – Sensex or Nifty 50 – have diverged from the broader market in a manner that hasn’t happened in the past 25 years. We’re in a bear market in small caps. The CNX Small Cap index made a high at 9559.15 in late January 2018. Today, at 7222.90, it’s down 24.4%.

The Nifty Midcap 100 index is down 16.2% from its highs and close to a bear market as well. In comparing the current RSI of the small cap index, it’s clearly approaching levels seen during previous selloffs in 2011, 2013 and 2015. We’d rather be thinking about buying the small cap index, not selling at these levels. (see chart below)

A Challenging Year for Fund Managers

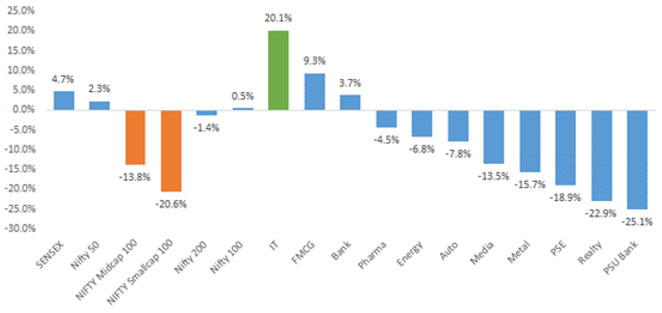

The chart below highlights the difficult year that fund managers have had to navigate. Information Technology is the only sector with a meaningful positive return YTD, up 20.1%., and under-owned by most portfolios. PSUs, Realty, Metals, Media, Auto, Energy and Pharma have been significant negative contributors.

IT is the Only Sector That’s Made Investors Substantial Profits This Year…

…While Small Caps, PSUs, Realty, Metals, and Energy Have Delivered Losses

Fixed Income

Bonds Attractive with Yields at Historical Spreads Over Equities

The yield spread has been a reliable indicator for bond market entries over the past few years (see chart below). The absolute high level of yields are reasonably attractive as well. From an asset allocation perspective, we may well be revisiting 2013 with currency volatility, FI outflows, fears on inflation. Both bonds and equities performed well during the ensuing year.

The yield differential between equities and bonds has fallen to 11-year lows. The 10y g-sec has risen on inflationary fears stemming from the rise in crude, fiscal concerns and MSP price increases. On the other hand, equity yields have not risen as much as the indices have held their ground. From a medium term perspective, the relative – and absolute – yield on bonds has now reached levels that have traditionally led to attractive bond returns.

Bonds Yields Are at Historically Wide Premium to Equities Signaling a Buy for Gilts…

Previous Buy Signals Have Been Meaningful in Terms of Entry Timing…

Outlook

Today Looks Somewhat Like 2013

The number of RBI hikes will be critical in determining the impact of rising interest rates on equities and the economy. It’s looking a lot more like 2013 where a short rate hike campaign assuaged concerns around a weakening currency and markets had a short albeit painful correction.

Economic Growth Remains Healthy, With Signs of a Strong Pickup in India

Structural trends, government reforms and government stimulus seem to be having a beneficial effect on the economy. Meanwhile, central bank balance sheets contraction and Fed / RBI rate hikes are headwinds. This trend is likely to persist but reduction of leverage is a positive for the global economy.

Policy Risk Trifecta – Trade War, Crude Oil, and the Fed

The domestic economy remains in a structural bullish cycle; however, there are risks facing the markets in the near and medium term. The risks pertain primarily to Fed policy, crude oil policy and trade war policy. A trade war with China appears to have been unleashed by the U.S. Crude was headed lower until the U.S. imposed sanctions on Iranian oil exports. Finally, the Fed appears intent in raising interest rates possibly leading to a slowdown in the U.S. economy.

Cyclical Corrections Are a Part of an Ongoing Structural Bull Market

Many investors returned to equities in mid 2014, only to see a painful 2015. A new batch of investors – the SIP buyer – have entered in the past couple of years. Meanwhile, those that stuck it out in 2014-15 have reaped rich gains. The lesson remains the same: equities are a volatile asset class, but India is a fast growth story and time in the market with an acceptance of volatility reaps outsized rewards.

The longer term call is easy to make, which is that the track record of the past 20 years demonstrates clearly that the market has withstood a great recession, technology bubble, European crisis, Chinese crisis and all manner of worries and delivered outstanding returns despite it all.

We remain in a structural bull market, with a cyclical correction that is already underway in mid caps and a bear market sell off in small caps. Investors that ignore short term volatility, time and again, emerge the largest long term wealth creators.

Tactical Strategy for the Near Medium Term

For those investors seeking to optimize the medium term, it’s always a trickier choice. On the one hand, the domestic economy is healthy, auto sales, consumption and credit trends are strong, and picking up speed, earnings are likely to be good in specific sectors and domestic flows continue to pile into equity markets. On the other, investors are faced with policy risks globally, with crude oil being a key risk. Macro trends seem to worsen and improve on a weekly basis and a tweet by tweet basis.

Ultimately, the appropriate asset allocation is the one that lets one sleep at night. Tactical asset allocation can be a particularly effective way to modify portfolio risk profiles. Portfolio protection should be viewed as portfolio insurance, a small cost that will deliver outsized protection benefits. Capital protection and hedged strategies are equally preferable. A tactical shift to fixed income is also a prudent choice.

At the portfolio level, returns will be driven by manager choice, cap choice and stock selection. We prefer diversified allocations primarily to large caps with some exposure to mid cap, as in our multi cap Titans portfolio: approximately 70% large cap, 10% cash and the balance in mid cap with minimal small cap exposure. Our sectoral preferences remain tilted towards domestic consumption, private financials, non cyclicals, and healthcare.

Indian Titans: Portfolio Performance

Sanctum Indian Titans

The current Investment Team took over Titans in January 2017, and since that time Titans is up 46.9% in absolute return. Titans outperformed the NSE 200 by 18% in CY 2017, and is under-performing the NSE 200 by -0.9% YTD. Titans is a multi-cap growth portfolio with strong growth at reasonable valuations. The portfolio currently sports a weighted top line long term growth of 24% and stronger PAT growth above 33%. We prefer to look at valuations relative to growth rates. The preferred metric is PE to growth (PEG). The PEG ratio for Titans is at 1.1-14.x depending on the growth profile considered, while it is much higher for the index; in other words, the Titans portfolio is significantly cheaper than the index on a PEG basis. (See middle chart on page 2).

Monthly PMS Performance

Absolute PMS Performance

Portfolio Metrics

Fundamental and Valuation Snapshot

Sectoral Performance Attribution for the Month

Commentary

Indian Titans, Sanctum’s multi-cap portfolio delivered a positive 4.1% return during the quarter, outperforming the benchmark NSE 200 by 0.2%. For the year, Titans remains comfortably ahead at 18.5%, 7.5% ahead of the NSE 200.

The portfolio remains anchored by high quality stocks that continue to deliver earnings growth. Bajaj Finance, Kotak Mahindra, Britannia and HDFC Bank were strong contributors. The portfolio’s underperformance during the YTD period is due to the severe selling that has occurred in mid and small caps. While mid and small caps are down 15% to 20% YTD, the portfolio has managed a low downside capture ratio, and is down in line with the NSE 200 at -2.7%.

Overall, stock selection drove portfolio performance mainly driven by solid picks in the Financials space, but missed selection in Materials and IT. Portfolio stocks in the Consumer sector as well performed strongly.

On a sectoral basis, our underweight stance on Energy helped boost performance. However this was offset by a drag from Industrials where our overweight position slightly dented allocation contribution to overall return.

Sanctum Indian Olympians Performance

Sanctum Indian Olympians: Up 38.8% Since Jan 2017

The current Investment Team took over Olympians in January 2017, and since that time Olympians is up 38.8% in absolute return. Olympians outperformed the Nifty by 5.5% in CY 2017, and is outperforming the Nifty 50 by 2.0% YTD.

Monthly PMS Performance

Absolute PMS Performance

Portfolio Metrics

Fundamental and Valuation Snapshot

Sectoral Performance Attribution for the Month

Contribution from Sectoral and Stock Selection

A Sector overweight in Financials aided performance as did the overweight in Consumer Discretionary. Underweight positions in Consumer Staples and IT proved to be a drag on performance.

Stock selection delivered positive contributions in Energy and Consumer Staples. Olympians outperformance was driven by pure stock selection, as opposed to many large cap fund managers that have drifted towards mid caps for alpha. Olympians remains a concentrated 12-15 stock strategy that is well positioned to perform in the current market environment.

Valuation

Olympians sports a higher bottom line growth than benchmarks as a result of which the portfolio trades at inline to reasonable discount to indices, particularly on long term PEG multiples.

Performance Attribution Q2 CY 2018

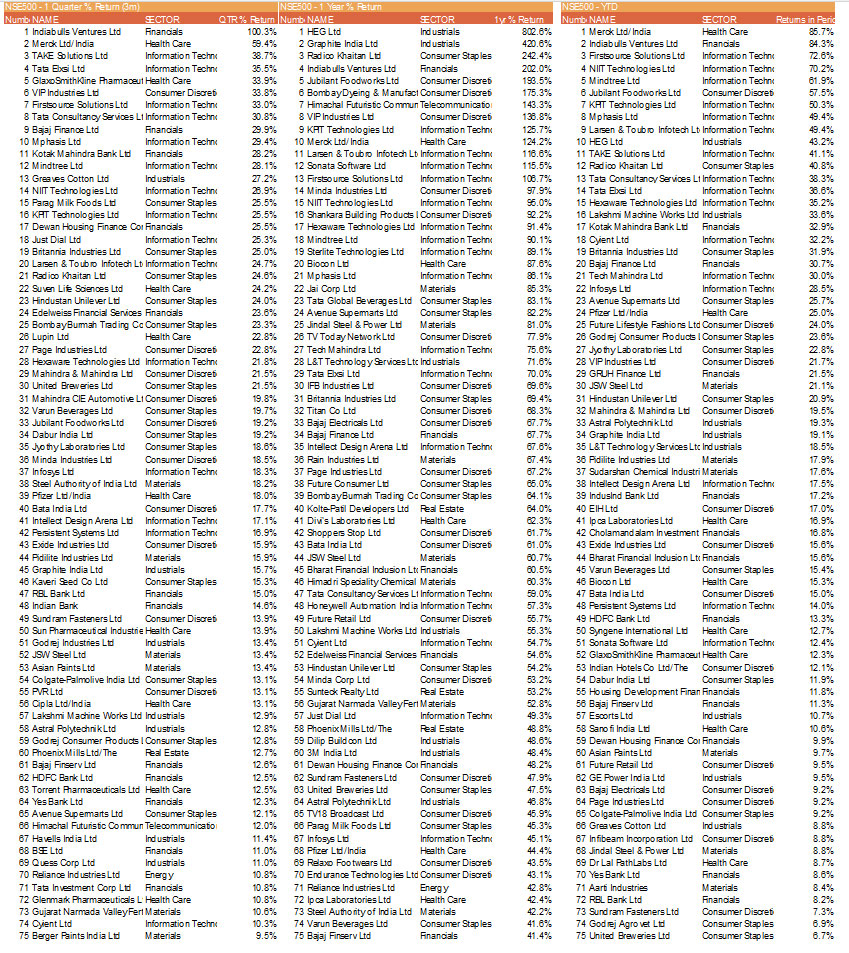

A deeper analysis of the two flagship indices, the Nifty 50 and CNX 500 across stocks, sectors, industries and market caps reveals insights and implications in terms of portfolio performance.

Nifty 50 Performance – Quarter, YOY and YTD

CNX 500 Performance – Quarter, YOY and YTD

Technical Outlook

The Nifty managed to post half a percent gain for the week to close at 10773 levels. In Friday’s session index touched high of 10816, but failed to sustain above 10800 levels. Nifty is facing resistance at falling trend line connecting highs of 11172 and 10929 for last four weeks and trading below it. Sustaining above 10800 levels on sustainable basis expect rally towards 10929 levels on the upside. On the downside immediate support is seen at 10710 levels. Breaking below this next support is seen at 10600 levels. But now critical support for the market is 10550 levels from where bounce back was seen on multiple occasions in month of June. In Nifty options, good amount of open interest addition was seen in strike price 10800 and 10700 Puts suggesting writing activity which is positive for the market. India VIX measure of volatility has seen dip in last few day down to 12.44 which is supporting the market.