Jun 9, 2022

We started 2022 on a cautious note. The global economy was firmly on the path of normalization post covid but so was liquidity. Withdrawal of excess global liquidity was the antidote to the froth in equity markets. In our January 2022 year commentary, we wrote “While we are very constructive on the Indian equity story over the longer term, we are undoubtedly expecting headwinds in the near term”. What we hadn’t anticipated then, was the outbreak of war, and a zero covid policy by China even as the world reopened. Both these events brought to fore fundamental issues of supply chain concentration and the chronic under investment in commodities, fueling inflation. And today we deal with the possibility of several key economies of the world being on the brink of recession.

ECRI’s U.S. Weekly Leading Index (Growth Rate YoY)

The U.S. equity market moves have been closely tied to the expectations of will-he-won’t-he flip on rates. The heightened volatility is expected to persist.

As China re-opens Shanghai and Beijing in a calibrated manner, it is now taking measures to mitigate the economic ravages of the shutdown. But the recent problems are just a layer on top of very fundamental issues that were unravelling through last year – that of several trillion dollars of over-investment in real estate and infrastructure. Several watchers were expecting an implosion, but considering the tightly controlled nature of the economy, we think the economy will grind its way through at lower trend growth over the next many years.

India Update

Setting aside the sombre tone of the commentary so far, Indian GDP grew 4.1% in Q4FY22 in real terms. the number is not as high as the RBI estimates and not as low as the street estimates either. Services PMI reading at 58.9 in May, expanded the fastest in 11 years. Our optimism for the pace of further expansion is, however, checked by higher inflation.

We have maintained that India is in a relatively better position even though we are likely to grow slower than RBI estimates of 7.2% for the current year. We had covered the rationale of our constructive view in our January ’22 note.

Countries with the highest projected GDP growth in 2022

What we have to contend with in the near term is higher oil prices, greater geopolitical uncertainty, and a higher fiscal deficit as the government takes steps to cushion the masses from the impact of higher inflation.

Equities

As expected, equities markets were volatile in May. Markets corrected in the first half of the month, then recouped some losses in the second half. The extent of correction indicated by the index masks the correction some of the individual stocks / sectors have seen. Over 120 of the NSE 200 fell more than the index. Any disappointment in earnings wasn’t spared by the markets.

We just concluded the corporate results season. Considering input prices were already rising prior to the Russia-Ukraine war, we expected margins to be under pressure. However, the full impact of the rising input costs will be seen only over the next few quarters. We expect the earnings profile of financials to improve the most in the current financial year.

Below is the break-up of Nifty earnings:

Sales growth ex-BFSI was largely led by commodity companies. Total income in the BFSI sector jumped 11% led by robust growth from SBIN and top private banks. Sales including BFSI grew 21.1% YoY. EBITDA ex-BFSI grew 14% YoY, impacted by high input costs across industries. Net profit ex BFSI grew 21% YoY helped by lower increase in finance cost and depreciation. Net profit, including BFSI, grew at a better 26%, boosted by a robust 42% YoY increase in net profit in the BFSI sector, helped by lower provisioning and writebacks.

Sectoral break-down

Key sectoral trends:

Information Technology: Management commentaries indicate that the demand environment continues to be robust. Order book as well pipelines remain strong in light of resilient technology spending. Managements expect the impact of higher cost pressures to fully reflect in the next couple of quarters post which margins could stabilize.

Financials: Credit pick up in the economy will bolster profitability in the coming quarters. Further lower provisioning could add to the bottomline. Management commentaries are optimistic about loan growth led by housing, consumer, and SME banking.

Consumers oriented sectors: The performance of the sector was a mixed bag.

Discretionary goods saw both pricing and volume led growth. Urban demand is holding up with a good order book for passenger vehicles, paints & consumer durables. Relief in input prices should help profitability in the current quarter as well.

Non-discretionary (staples) witnessed largely pricing led revenue growth but saw volume pressures. Rural demand continues to be weak as reflected by the lower volumes in two-wheelers and consumer staples. Consumer staples could continue facing pressure with higher agri prices and limited ability to pass on the same to end consumers.

Commodities: Metal companies have posted peak margins and profitability. We think weakening prices on global growth concerns would mean headwinds for earnings in the upcoming quarters. Upstream energy companies posted strong earnings while downstream companies are getting hit due to a cap on marketing margins. Cost inflation continues to hurt cement companies amid flattish volumes.

Pharma: The downward trend in revenue growth reversed during this quarter, but profitability got impacted due to inflated raw material prices, price erosion in US generics and escalated logistics costs. Managements sounded positive on India as well as overseas demand.

REITs and INVITs

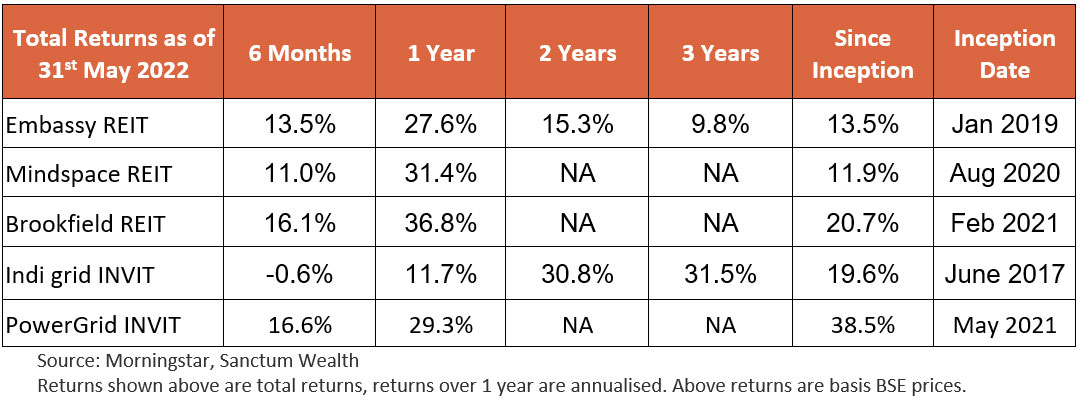

Over the last couple of years or so amid a low yield environment we had recommended investors look at fixed income alternatives like Real estate investment trusts (REITs) and Infrastructure investment trusts (INVITs). Investors that actioned upon this, have made stellar returns over the last few years as highlighted by the table below.

We think the bulk of returns for INVITs may be behind as pre-tax yields have come off highs of ~15% in 2019 to about 9-10% currently. Also, INVITs have benefitted from a fall in interest cost on debt over the last few years, those benefits will reverse as interest rates rise. Finally, with higher bond yields some money will move away from INVITs into bonds now.

REITs on the other hand are slightly better placed. Post covid, we saw rice in vacancies as employees worked from home, causing occupancy levels across REITs to decline to 80-85% vs 90-95% pre-covid. However, through these tough times, the REITs continued distributing a steady income as the decline in occupancy was offset by a fall in interest costs and general cost savings implemented by REITs. With people returning to offices, occupancy levels should rise and cross 90% this fiscal year across REITs. While some of these gains will be offset by the rise in interest costs, overall, we expect distributions to increase going forward. Some of this will get upfronted in capital gains. Hence, investors can still make high single digit post tax returns over the next 2-3 years.

In our asset allocation strategy (S-MAPS) we plan to reduce exposure to INVITs and add to REITs to reflect our views.

Conclusion

May 2022 was a volatile month for both equities and bond markets. The next few weeks could also create volatility as major events like the RBI monetary policy and the Fed policy are scheduled for the first half of this month. While the rate action by the RBI is probably priced in, commentary around inflation, growth and future rate trajectory could have implications both for equity and debt markets. We will review our view on equity and debt post the policy actions again if required.