May 31, 2022

• As buy the dip gains some momentum in global equities, we look for long term value and not just tactical plays.

• We see a great opportunity in Vietnamese equities after recent poor performance. Strong future growth and a low valuation.

• We see value in Latam equities given their exposure to rising commodity prices and economic readiness to cut rates as inflation abates.

• Companies that have the know-how and technology to push the world closer to carbon neutrality will see multi-year strong growth

Last week investors showed some renewed appetite for buying the dip in the equity markets; however, we prefer to continue looking for long-term opportunities and not just tactical buys in the aftermath of the recent sell-offs. This week we highlight three opportunities that we believe offer firm long-term value and are not just tactical trades.

Vietnamese equities were one of our preferred long-term investments even before the current crisis unfolded. We believe the recent sharp setback in the equity markets offers an excellent opportunity to top-up holdings.

Vietnam is unique amongst the frontier markets and has a strong economy notwithstanding the challenges of COVID and the current global economic crisis. The IMF has projected GDP growth of 6% this year. Although that figure is lower than the 7.5% expected at the start of the year, Vietnam remains one of the strongest growing economies in Asia. Meanwhile, economists forecast that inflation will remain well within desired levels. Several factors have worked in Vietnam’s favour. Monetary policy has been prudent, with short-term interest rates being marginally above the current inflation rate of 1.5%. This has capped any rise in long-term interest rates, with the 10-year bond yield currently around the 2.3% level. Economic activity in the country remains robust; retail sales grew 12% in April, supported by a vibrant labour market.

Vietnam continues to enjoy healthy capital inflows as overseas companies seek to diversify their Asian manufacturing bases away from China. Year-to-date foreign direct inflows at the end of May stood at $7.7 billion, which is a new record high. Investment in manufacturing is around 55% of FDI.

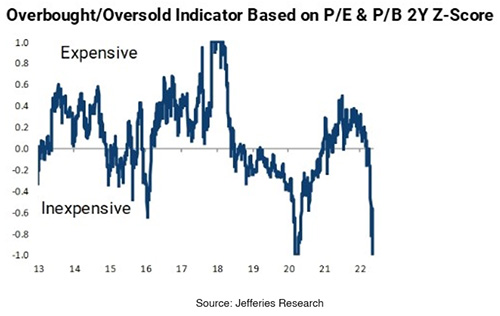

The Vietnam equity market valuation on many metrics is quite close to the cheap levels we saw during the COVID crisis. Continuous upgrades to corporate profit forecasts support those valuations. Foreign investment in the equity market has remained robust, with $170million of net investments since mid-April. The government’s decision to re-open Vietnam to foreign tourists from May 15th provides another potential catalyst for positive news flow and a recovery in the market.

Chart 1: Vietnam equities valuation close to super value

We believe that investors underappreciate the number of positives supporting Latin American equities.

Latin America for some reason always gives the impression of being a part of the world where another crisis is about to unfold. However, the region’s equity markets could be one of those that can shake off the current global economic challenges and build on their recent strength.

Unlike many, Latin America was late to emerge from its fight with COVID. However, it now finds itself with notable economic strength. Latam countries were forced to raise interest rates much earlier than their counterparts in the West. Hence, interest rates in many Latam countries are already ahead of inflation. Indeed, Latam central banks could be in the enviable position to cut interest rates earlier than most as global inflation abates.

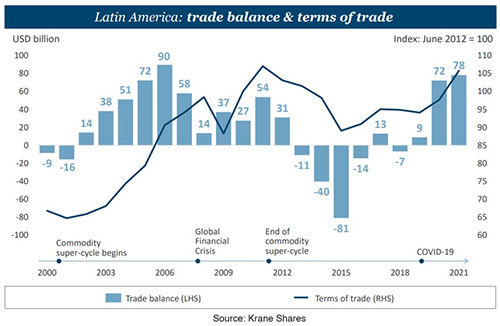

Higher commodity prices have clearly helped Latam’s cause. The region has run a significant positive trade balance over the past two years, helping to stabilise Latam currencies. We expect the region to benefit from the reshaping of trade flows as the world comes to terms with the de-globalisation of trade flows because of the trade wars with China and the marginalisation of Russia. Latam remains open for business and is likely to be a significant beneficiary of FDI flows as Western countries rejig and redirect their investment flows to countries that can supply crucial commodities amongst metals and agriculture. Latam has a huge opportunity to grab a more significant share of the global supply of agricultural products. Latam already has a strong reputation for environmentally friendly agricultural production and has access to substantial renewable freshwater resources.

Moreover, Latam appears well insulated from the current energy crisis considering about 52% of the region’s electricity production comes from hydro and renewables compared with 18% globally. The region’s impressive ESG credentials are clear to see.

Chart 2: Latin America Strong Trade Account

While global GDP growth has dipped, the commitment to ESG issues is strengthening. A secular growth strategy is investing in companies that provide the means to hit decarbonisation targets.

July 2021 marked the hottest ever month on the planet. ‘Climate-related disasters’ increased 83% from 2000 to 2019 over the preceding 20-year period (source: National Oceanic and Atmospheric Administration August 2021). The world recognises that it has a mammoth problem and has increased commitments to net-zero carbon emissions. Consequently, we see higher spending to meet the targets. KraneShares estimates that net zero-commitments cover one-fifth of the world’s largest corporations and 68% of global GDP, compared with 16% in 2019.

The secular growth companies of the future will fall into two camps: The first are those that supply the technology enablers of the decarbonisation initiative. Secondly, those companies in traditionally high emissions industries are on the cusp of the transition away from fossil fuels. The second group should benefit from taking market share from ‘dirtier’ competitors and gaining a re-rating from their improving ESG scores.

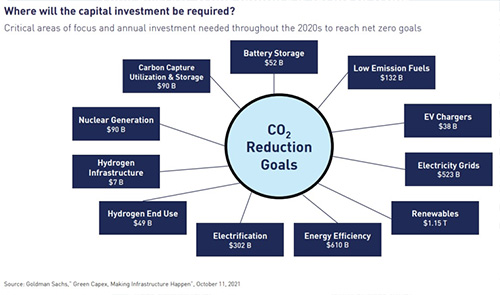

The aggregate investments estimated to be needed to achieve the decarbonisation targets are massive and imply equally massive growth in specific industries. Goldman Sachs estimates that there’s a need for investments worth $300bn per year in electrification, $500bn in electricity grids, and $50bn in battery storage.

Chart 3: Huge growth expected from investment in decarbonisation