May 2, 2017

Summary

Global

Domestic

Global

Global markets have been volatile recently, primarily because two major events. One is the crucial French elections and the other is President Donald Trump’s long overdue “corporate-friendly” tax proposal.

French Elections Have Markets Breathing a Sigh of Relief

The primaries of the French elections were broadly interpreted by markets as a positive outcome. Initially, the far-right nationalist Marine Le Pen had appeared to emerge as the strongest Presidential candidate. Since then, pro-EU centrist candidate Emanuel Macron has garnered momentum with convincing debate performances.

In the recently concluded first round, Macron amassed 24.01% votes vs. 21.3% for Le Pen. This has allayed fears of a Brexit-like fall-out on the French elections and a cloud over the future of the Euro zone. All eyes now focus on the second round to be held on 7-May-17 with markets pricing in a Macron win, evident particularly in the recent strength in the Euro.

An Aggressive Tax Plan Proposal in the U.S.

While there was cheer on the Euro front, President Trump sprung a modest surprise by coming forth with plans of a corporate-friendly tax culture in the U.S. In a nutshell, the tax proposals appear to benefit businesses, the middle class and high-earning individuals. Digging deeper into the numbers:

Markets Remain Skeptical of the Plan’s Passing and Viability

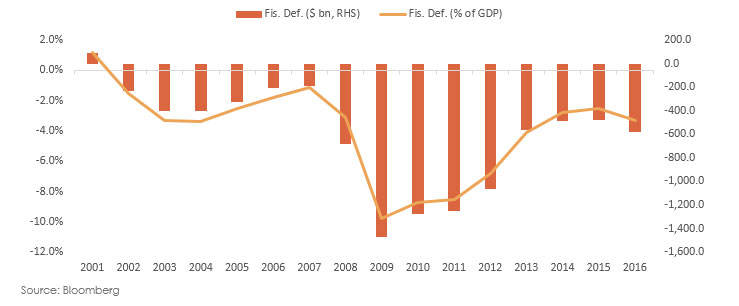

The U.S. Fiscal Deficit Currently at ~$600B Would Balloon Dramatically Under the Proposed Tax Plan

Equities

Early Earnings Score Card for Q4FY17

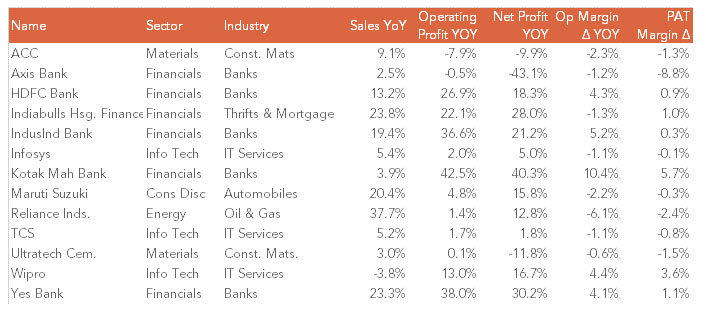

The earnings finale for the year has kicked off with most flagship companies of the NIFTY 50 reporting strong top-line growth barring IT majors, which is understandable given the broad slow down seen in the sector in terms of painful revenue transition from deal pipelines.

Performance Amongst the Nifty 50 Has Been On the Whole Quite Solid, Giving the Markets Cheer

Sector Performance

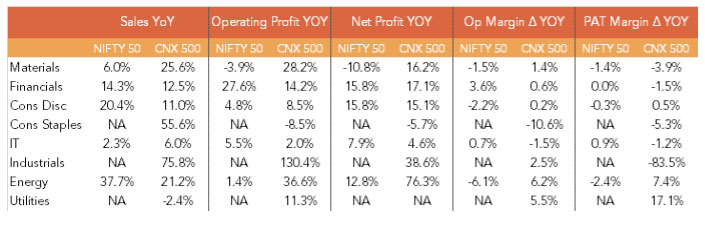

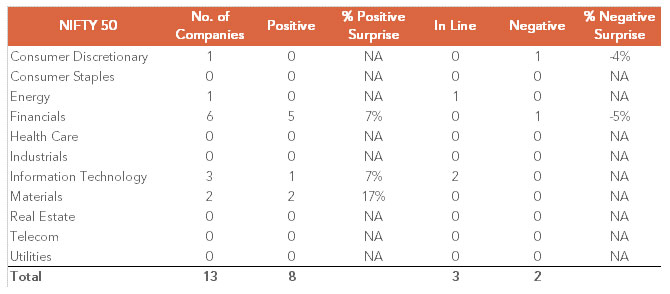

So far, 13 companies from the NIFTY 50 and 47 from the CNX 500 have reported earnings. From this limited set, a top-down sectoral perspective suggests the broader market is doing better than the NIFTY 50, driven by strong top-line growth in Materials, Financials and Consumer Discretionary.

Looking at profits, things look decidedly impressive, so far, for the CNX 500. Sales growth is double digits or higher for all sectors except IT and Utilities. Net profit growth is also similarly strong for Materials, Financials, Discretionary and Industrials.

Performance Has Been Stronger and More Consistent On the Broader CNX 500

Earnings Scorecard

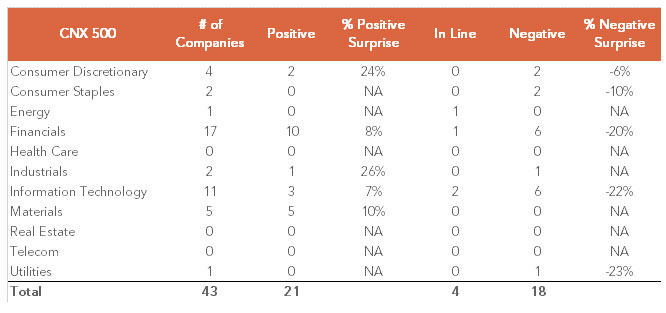

While earnings have in general been positive so far, the same has been reflected in earnings surprises as well. The most striking being the resilient bottom-line delivery of Materials in both the mid and large cap space which has been driven by strong top-line beats. Financials have been another positive surprise as banks have delivered strong loan book growth (for instance, sustained stellar advances growth at Yes Bank) alongside hopes of potential resolution of the NPAs.

Net-net, the earnings results have so far been robust. We note that the first set of numbers are usually strong, and further clarity will emerge over the month. The bright spot so far has certainly remained the Materials space.

Overall bottom-lines (net income margins) have appeared a tad depressed. Despite this, most the CNX 500 companies (58%) have not disappointed. On the large cap front, India Inc. has fared even better with only 15% falling short of expectations.

58% of CNX 500 Companies Have Met or Exceeded Expectations

85% of Nifty 50 Companies Have Met or Exceeded Expectations

Political Stability And a Pickup in Fiscal Spend

With earnings season off to a cheerful start, the results of the recent elections provide further comfort to the markets. With the Government now entering its 4th year in office, and eyeing re-election in 2019, we expect a pickup in spending in H1FY18. Thus, we would expect infra spending to assist Industrials and Capital Goods related sectors in the Infra value chain. Materials have already started showing signs of good earnings performance.

Markets were further comforted by the BJP’s win in the Delhi Municipal Elections. The Delhi civic elections only add to the ruling party’s image of invincibility and leaves a divided opposition further demoralised in the run up to the national elections in 2019. The BJP has held its stronghold in the MCD elections continuing its winning streak last seen here 5 years ago.

Fixed Income

The major needle-mover for the 10-Yr G-Sec here was the heightened anticipation of inflation rearing its head as 2 members of the RBI’s MPC had hawkish views on the growth of the economy. In fact, Michael Patra, explicitly favoured a pre-emptive 25bps increase in the policy rate at the MPC’s last April meet to help attain the 4% target. This, in his opinion, would have obviated the need for a back-loaded policy action later when inflation would be unacceptably high and entrenched. As a result, G-Sec yields have moved slightly higher and now trade at 6.96% levels.

Outlook

Trailing P/E valuations on the CNX 500 have reached 27.6x, still below Sep-16 levels of 28.6x. Arguably, this expensive 15% valuation premium to historical 3-year levels seems justified as earnings growth momentum has been gathering steam recently.

While over the last 3 years, CNX 500 earnings have grown ~3% p.a., the majority of this growth is back end loaded. In other words, growth has been coming through in the last 3 months (7% unannualised) and last 1 year (5.3%). The growth momentum in fundamentals is likely to continue.

Going forward, we expect markets to continue to gradually climb the wall of worry, which is a healthy sign. Index level appreciation going forward is likely to be driven by continued growth in earnings, with valuations playing second fiddle.

Technical Strategy

The Nifty witnessed a 2% gain for the week to close at 9304. After the last six weeks of range bound action, the index is seeing a breakout from sideways consolidation with good price action to close above 9300 levels.

On the upside, the next technical level for the index is at 9570. In Nifty Call options, the highest open interest was at 9500 strike thus suggesting market is likely to head towards 9500-9570 levels. Though momentum indicators have flattened out or turned down from higher levels on the weekly chart, as long as price continues to make new highs and higher lows, the uptrend still remains intact. Hence only a breach of the previous swing low levels 9075-9024 would be a sign of caution in the market.

In Nifty Put options, the 9000 Strike price has the highest open interest followed by 9100 strike suggesting that 9100-9000 is the base for the market. FPIs have been negative for April with an outflow of Rs. 2245 crores (provisional) and domestic inflow of Rs. 11845 crores (provisional) for the month, which has taken the market higher.

Negative correlation between Nifty and India VIX continues to hold as market is hitting new highs while volatility is hitting multi years low. But any sharp spike in VIX or divergence in correlation would worry the market. Until then the market uptrend is likely to continue.