May 16, 2017

What is the Right Risk Mitigation Strategy?

As valuations rise and investors sit on attractive returns for the year, we have been pondering the following: If everyone insures homes, lives, cars, health and many insure cell phones, travel and even pets, why don’t investors insure portfolios?

If an investor is clear that they are in the markets for the long term, and today, almost every investor is clear theyare in the markets for the long term, is 60/40 an appropriate return maximising strategy?

Investors inherently understand that asset allocation is at the end of the day a trade-off that lowers expected returns for lower volatility. The underlying principle is that risk and return always go hand in hand. Again, we ask, what if there were more effective ways to manage volatility?

Over the past fifteen odd years, equities in India have delivered 18-24% in quality mutual funds and PMS schemes. Meanwhile the comparable return in bonds has ranged in the 7-9% neighbourhood. That is a significant 11-15% differential in expected returns.

Further, the correlation of the major asset classes has tended towards 1 in recent sell-offs, which raises doubts about the efficacy of efficient markets and optimal portfolio concepts.

There is also the issue of investor risk appetite and appropriateness. Appropriate risk is the risk that the investor should be taking to maximise long term returns. Meanwhile, actual risk could be a far lower number, as some investors may be quite risk averse.

The asset allocation construct is structured around the developed markets, with equities delivering 12% a year and bonds 6% a year. However, what if the expected return is 18% for equities and 6% for bonds? How does that impact strategy?

The fact remains, that no one answer is the right answer. These are, however, questions worth asking and debates worth having. We, for one, believe traditional asset allocation strategy can be improved upon.

Which brings us to tactical asset allocation. Does a travel insurance concept make sense for investments? In other words, are there times where selective protection is a worthwhile decision that can actually enhance returns and reduce volatility?

We think the answer to this last question is selectively yes, while acknowledging each situation is complex and different.

Mitigating losses is a worthwhile objective in investment management. It is certainly a discussion worth having.

Can Valuations Stay Higher Longer?

The second item that has been on our minds lately, and we are starting to mull the possibility cautiously, is whether we are in a period of declining cost of capital, globally and domestically, which argues for extended valuations longer than historical patterns would suggest. There are additional factors beyond cost of capital at play. More on this in the future.

Equities

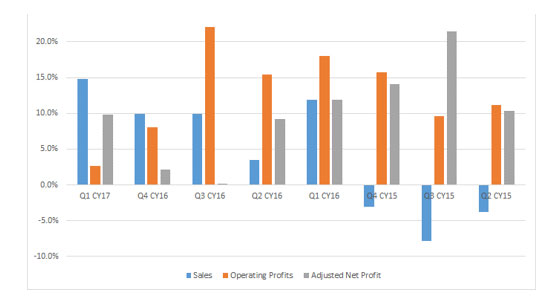

CNX 500 Companies Reporting Highest Sales Growth +10.9% In 8 Quarters

The current earnings season has played out well so far. Sales growth is up 10.9% year over year for the 166 companies that have reported earnings results to date. A same on same comparison over prior quarters demonstrates a rising trend on sales growth, ergo the economic recovery does seem to be picking up momentum. With positive drivers for the second half of the year, this is good news indeed!

CNX 500 Companies Net Profits Are Up 14.6%, Again the Best Showing in 8 Quarters

While operating leverage has certainly not kicked in yet, profits after taxes are doing fine. This may be due to reduced interest expenses, and net profits are at an 8 quarter high, again demonstrating a positive trend in earnings growth momentum.

Nifty 50 Sales Growth a Terrific 14.8%, While Net Profits Are Up a Less Impressive 9.8%

24 Nifty 50 companies have reported earnings to date, and sales growth is an impressive 14.8%. Meanwhile, earnings are once again impacted by one-offs such as Bharti Airtel, which distorts the performance of the index.

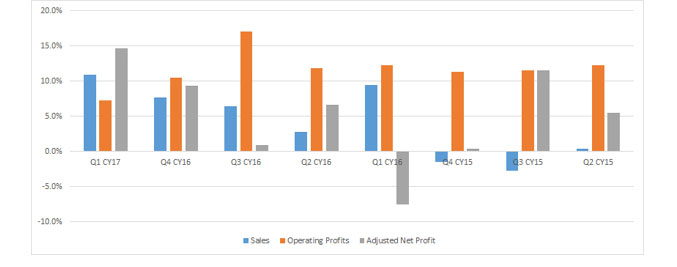

With 166 Companies Reporting in the CNX 500…

Sales Growth Has Posted Its Best Result in 8 Quarters, +10.9%

And Net Profits Are Up 14.6%, The Best Showing Also in 8 Quarters

With 24 Companies Reporting in the Nifty 50…

Sales Growth Has Posted Its Best Result in 8 Quarters, +14.8%

And Net Profits Have Rebounded From Demonetisation, Up +9.8%,

Driven by Earnings, the Market’s Moved Higher

While PE Expansion Has Driven the Index Over the Prior Two Years, Earnings Growth Is Finally Kicking In

While PE expansion drove market returns over the past one year and three years, in the past three months, we are finally noticing a pickup in earnings over the past three months. Earnings growth is finally starting to kick in and driving price appreciation, and PE expansion has not been a contributor in the recent up move in the broader index.

Sector Performance

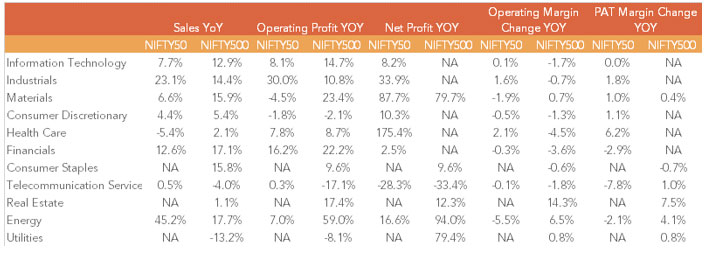

From the set of Nifty 50 and CNX 500 companies that have reported, a top-down sectoral perspective suggests the broader market is doing better than the NIFTY 50 on the top-line. Multi-cap Materials, Financials, IT, Health Care and Consumer Discretionary reported far more robust top-lines than their large-cap cousins.

Sectoral Sales Growth Led by Energy +17.7%, Financials +17.1%

Energy and Financials have so far been the leaders in top line sales growth, posting impressive high teens sales growth for the broader CNX 500 to date. Meanwhile, for the Nifty 50, performance is being led by Energy and Industrials.

Sectoral Profit Growth Led by Energy

Multi-cap materials stocks have delivered better operating margins than large caps though the trend here persists of not-so-stellar margin performance as compared to revenue growth. This can be expected as multi-caps should have lesser economies of scale than large caps.

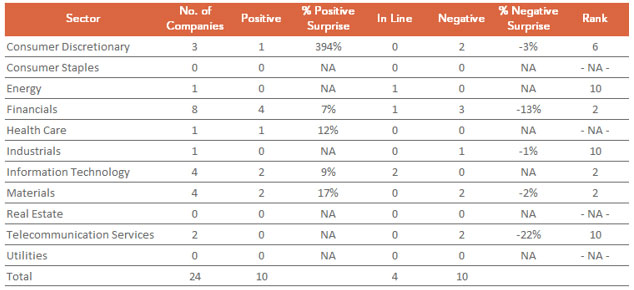

At a Sectoral Level, Performance Is Mixed On the Broader CNX 500:

Better Sales, But Muted Margins

However, Performance Has Been Largely Meeting Expectations, Not Exceeding Them

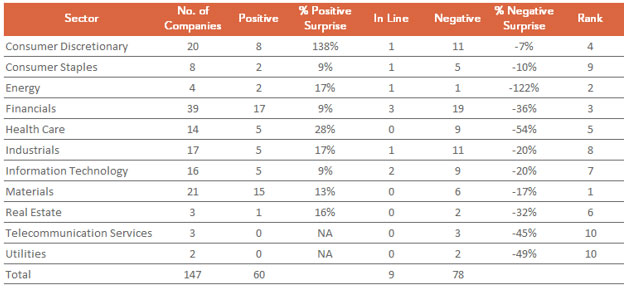

47% of CNX 500 companies reporting and 58% of Nifty 50 companies have met or exceeded expectations. Generally speaking, at a 50/50 split, this is slightly below what we would historically consider a good performance.

Moving to a sectoral view, materials have delivered the most consistent performance in the CNX 500, followed by Financials. Also notable is that 11 out of 20 companies in the consumer discretionary sector have not met expectations.

47% of CNX 500 Companies Have Met or Exceeded Expectations

58% of Nifty 50 Companies Have Met or Exceeded Expectations

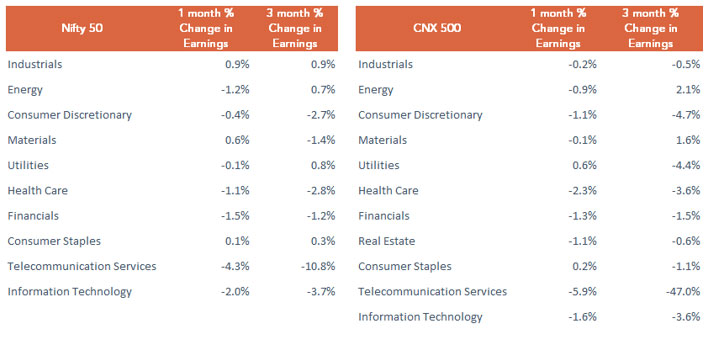

Further, Earnings Revisions Remain Muted

Despite the strong performance, earnings revisions remain surprisingly muted. Revisions have risen slightly in Energy +2.1% over the past 3 months, and Materials +1.6%. Other than these sectors, revisions appear to be adjusting EPS estimates slightly lower.

Earnings Revisions Though Remain Muted Suggesting Conservatism Amongst Managements

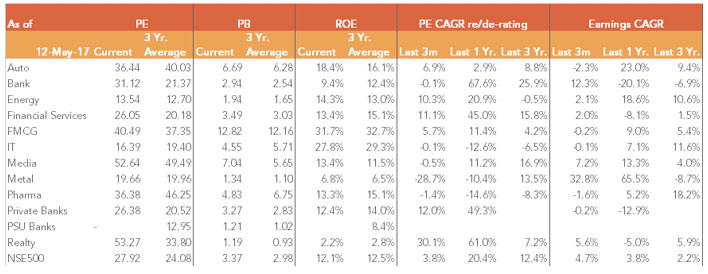

Sectoral Valuations Are Elevated in Financials, Banks, FMCG and Realty

While broadly, the CNX 500 is trading at a premium to 3 year averages, there do exist certain pockets of relative cheapness, autos being one such prominent space. Interestingly, the sector has remained hinged on fundamental delivery and consequently is fairly attractive.

Energy Attractive, While Media, FMCG and Realty Expensive

Fixed Income

Positive Surprise on CPI

CPI for Apr-17 came in at 2.99%, which was surprisingly lower than expected, and should lay to rest hawkish tendencies recently surfacing amidst the MPC members. Prior readings for Mar-17 had increased to 3.81% and expectations for Apr-17 were also elevated at 3.3%. The reading was lower primarily on account of lesser than expected price increases in the food basket.

This softening should potentially lead to a downward bias on G-Sec yields bucking the recent yield expansion seen over the past couple of months.

The CPI Just Hit a Multi Year Low

Tax Filers Rise by 9.5 Million

Further adding to downward bias on G-secs is news that the government added 9.1 million new taxpayers in 2016-17, a nearly 80% increase, driven largely by efforts around demonetisation and post demonetisation follow through. This is expected to significantly boost the government’s tax revenue.

India had 55.9 million individual tax payers in 2015-16, so this is a substantial rise in the tax base. The government is also targeting 1.5 lakh accounts with average deposits around Rs. 3.3 Cr. A back of the envelope calculation suggests the added revenues could be significant, ranging Rs. 40,000 Cr. and upwards.

Alongside reduced borrowing needs cited in the budget, the reduced supply from government securities is worth noting in determining the future direction of interest rates.

Benign Inflation, Reduced Supply, Increased Collections

The recent uptick in rates, benign inflation, reduced government borrowings and increased tax collections and an eventual lower cost of capital structure suggests limited bias to the upside on rates. The RBI would seem to have been caught wrongfooted on its inflation expectations.

On the other hand, if the earnings data is to be believed, and macro views incorporated, one could easily make a case for a rise in rates in coming quarters. It is worth noting that expectations for inflation range from a cut of 50 bps to a hike of 50 bps over the next twelve months.

With the surprisingly lower CPI, declining government financing, we think rates could have a bias to the downside in the short term. However, a fixed income call has to hold for 3 years. That is a much tougher forecast. An equally competent case can be made for rising or falling rates in the medium or long term and the timing of such is hard to predict. We would want a few more inputs and confirmation before committing to a direction and forecast.

In this situation, the prudent positioning is to position for yield, and away from duration. For investors with some risk appetite, corporate bond funds with the potential for rating upgrades make sense. Our preference, however, remains towards safer accrual strategies, and actively managed select AT-1 bonds.

Outlook

Positive Reforms taken by the Government

The Government has set the ball rolling with plenty of policy framework changes announced. Skimming the surface, we have the National steel policy 2017, the NPA Ordinance (on the back of recommended increased provisioning and stringent NPA divergence reporting w.r.t. RBI), RERA, pharma push for generic-generic instead of branded-generic, formation of a National Health Care Policy and finally GST.

The National Steel Policy

The National Steel Policy at first glance seems ambitious and prone to being dismissed by investors for envisaging a 7.5% CAGR pickup in steel demand and capacity over the next 15 years with a 10x demand spurt from Infrastructure; however, the policy is rational in its immediate projections till FY21.

Core Sectors’ Output and Their Main Drivers

NPA Resolutions

The banking space is fairly mixed with certain banks reporting improving profitability and incrementally lesser slippages though the improvement of their books. However, it cannot be labelled explicitly as a turnaround, Dena Bank and IDBI being case in points.

However, what is encouraging is that the RBI has consistently stepped up its efforts in resolving NPAs starting with the AQR, the CDR, the SDR, the S4A, divergence reporting, recommended increase in standard asset provisioning and finally the recent NPA Ordinance which should help in providing some immunity and empowerment to banks in resolving the bad loan mess.

Cost of Capital Trending Down

Continued pressure by the RBI to pass down interest rate cuts in the form of declining MCLRs has also led to the cost of capital coming down. This should augur well for most corporates and should serve as a much needed bolster for flagging corporate credit growth.

On debt, our preference remains towards safer accrual strategies, and actively managed select AT-1 bonds.

We continue to expect equities to ride on the back of momentum in underlying fundamentals and reasonably strong earnings witnessed thus far. The news on the CPI front is a strong positive. With lower inflation, real profits will be stronger in coming quarters.

Technical Strategy

The Nifty 50 closed at the psychological level of 9400 with a 1.24% gain for the week. While the daily candlestick was bearish, on higher time frame – the weekly chart – a bullish candlestick continues to form higher top higher bottom patterns.

FPI/FII who were net sellers for the last four weeks turned net buyers last week with Rs. 3,060 Cr. (provisional) inflows, while DIIs were net sellers to the tune of Rs. 1,037 Cr. (provisional). Momentum indicators on the weekly chart continue to be in bullish mode and again turned up.

Immediate levels on the upside for the market are seen at 9570~. Near term support levels for the index is seen at 9300-9250 level and major support levels for the market is in the region of 9100-9000 levels. In Nifty options, the 9300 put has the highest open interest, while for call options, the 9500 strike price has the highest open interest. This suggests that range bound action is likely to continue in the market. Nifty options Put/Call ratio is at 1.24 which is approaching towards higher end of the range and would be a concern if it continues upward. India VIX continues to trade at all time lows while the index is hitting new highs, maintaining the negative correlation. But any sharp spike in VIX or divergence in correlation would be a cause for worry for the market.