Mar 22, 2023

Weathering the Storm

It hasn’t been the best of times for equity investors. Twelve months index returns to end February were 3%

for the Nifty, 6.7% for the Midcap 100 Index, and a negative 7% for the small-cap index. The broader

indices – Nifty 200 and Nifty 500 – delivered marginally positive, low single-digit returns.

In the backdrop of severe macroeconomic crosswinds, the low-yet-positive returns on indices mask a lot of mayhem that many individual stocks have gone through in the past year, which made eking out returns even more difficult for investors and portfolio managers. In such periods, risk management becomes more important than chasing returns for equity investors. The old winners rarely come to lead the next rally and, therefore, the badly bruised portfolios that hold the old winners take a long time to come back.

At Sanctum, taking cognizance of these risks in late 2021, we have positioned our portfolios accordingly. Our risk-first approach and thoughtful stock selection helped us deliver stable post-fee performance in our flagship schemes as can be seen in the table below.

Performance is calculated using Time Weighted Returns, net of fees and expenses. Returns over one year are compounded annually; returns for less than one year are absolute. Please note that SEBI does not verify the performance information provided above. Please note that past performance is not a guarantee of future performance.

The Winners and the Laggards

In the last year, half of our portfolio stocks in both Titans and Olympians delivered positive returns, while a

third delivered returns of more than 10%. On the other hand, a fifth of our portfolio stocks delivered a 10%

or more negative return.

Some of the names that stood out were KEI Industries, Schaeffler India, Craftsman Automation, and APL Apollo Tubes. The ones that dented the performance were Infosys, Info Edge and Divis Laboratories.

Apart from the stocks in the table above, banking stocks also led to positive performance as we were overweight the banking sector from the beginning of 2022.

The following table shows the top five winners and laggards in the Olympians’ portfolio.

The Winners

KEI Industries

KEI is a leading supplier of wires and cables to institutional and retail clients in India. It is one of our oldest

holdings in the Titans portfolio and has been a phenomenal compounding story for the last ten years. Its

topline and bottom-line have grown at a CAGR of 12% and 32% in the last ten years, with significant

heavy-lifting in the past five years.

The company fits well in the housing and industrial/capex theme that we have been bullish on since early 2021. KEI has done well in its B2C wires business over the years by focusing on improving its retail presence and brand awareness. It has also robustly grown its institutional business by becoming one of the preferred suppliers of quality wires and cables.

KEI’s stock price has also done well, delivering over 4x returns in the last five years. As the business continues to do well and the market opportunity is huge, we remain confident in the company and believe that the robust compounding will continue.

Schaeffler India

Schaeffler became a part of the Titans’ portfolio in July 2021. The company is a part of Schaeffler Global

and is a leading ball and rolling bearing manufacturer servicing the automotive OEM, aftermarket, and

multiple core industrial segments.

We invested in Schaeffler India due to our bullish view on the industrials segment, which was ~42% of the company’s revenue in FY21. The other part of Schaeffler’s business – automotive – was grappling with headwinds such as chip shortages and input cost inflation, and thus wasn’t performing at its full potential. Schaeffler caught our eye because the company has a good earnings track record and has also expanded its capabilities, product profile, and capacities through a major capex drive from FY19 to FY21 to cater to domestic and export markets.

Schaeffler’s capacity and capability expansion helped it gain local and export business as industrial activity picked up and auto industry woes subsided. Driven by buoyancy in both businesses, the company has performed well operationally and financially in the last two years, delivering a robust revenue CAGR of 35% and an even better EPS CAGR of 74%.

Going forward, Schaeffler continues to invest in product profile expansion, especially in the automotive segment, to increase its content per vehicle. It also continues to expand its focus on the export markets. The company has also upped its capex intensity recently to make the most of the momentum it has gained in recent times. With increasing localization in sourcing, there are tailwinds in margins as well, which should help it post better earnings growth.

Though we have pruned some exposure in Schaeffler for portfolio rebalancing purposes, we continue to hold the stock in the Titans’ portfolio. We remain positive about the company, given that the business traction we are seeing is more structural than cyclical.

APL Apollo Tubes

APL Apollo Tubes is a leader in the branded structural steel tube segment. The company’s installed

capacity is more than double that of its nearest competitor, giving it a lead in the rapidly expanding

structural tube market. In addition to the largest manufacturing capacity, it has a wide distribution network,

which is 4x that of its nearest competitor.

APL was in a sweet spot being a leader in structural tubes that are now being extensively used in construction projects due to their affordability, ease of installation, and durability.

APL has demonstrated superior execution capabilities by developing new products and devising new use cases for structural tubes, which has helped it post ~30% revenue CAGR from 9MFY19 to 9MFY23. High revenue growth and a high share of value-added products have led to better margins, helping the company deliver 53% EPS CAGR in the same period. This is despite being impacted by inflationary cost pressures in 2021 and 2022. Its balance sheet has also seen a marked improvement with working capital days declining to 7 days in FY22 from 27 in FY19.

We remain positive on APL as it has further strengthened its leadership position in the last two years by adding capacity for value-added products and expanding its product profile and reach.

Craftsman Automation

Craftsman Automation is a diversified engineering company engaged in automotive and industrial

segments. The company’s product profile includes machined products and components for MHCVs,

Aluminium products for 2W and 4W, and industrial customers.

In FY22, Craftsman completed a large capex drive that started in FY14, increasing its capacities by 2.5x. It also showed remarkable resilience in performance in the slow auto cycle 2018-2022, growing better than the industry. With new capacities and an expanded product profile, Craftsman was poised for good growth as both its business segments were seeing buoyancy in 2022.

While quarterly earnings have been decent of late, the hypothesis is yet to play out fully in Craftsman. We continue to be positive on the company and believe that there is a lot more steam left in the industrial and auto cycle.

Mahindra & Mahindra Ltd.

M&M was the top performer in the Olympians’ portfolio. The company saw a significant revival in fortunes

after it received a strong response for most of its new launches in the automotive segment. The automotive

segment revenue grew 42% YoY in FY22 and 76% in 9MFY23. The company also benefitted from 9% and

15% growth in tractor volumes in FY22 and 9MFY23. The growth came on stably increasing margins led by

better realisations, operating leverage, and cost controls.

We continue to be positive on M&M as the company has chalked down its capital allocation strategy along with capacity enhancement to fulfil its strong order book. It is also developing EVs, which would help boost sales in the automotive segment.

The laggards

As it goes, no equity portfolio can have only winners, and there will always be laggards. Therefore, the

portfolio manager’s job is to minimize the damage from them. We believe that our risk management

emphasis has helped us in this regard in the past year.

Infosys

While maintaining an underweight position in IT, we continued to hold the bellwether due to its superior

earnings profile and better growth. The stock underperformed in the last year mainly due to concerns about

a demand slowdown in the IT industry.

Despite a lot of noise of a recession in the company’s major markets, Infosys has maintained a high-teens growth rate led by its record deal wins. It continued to up its revenue growth guidance for FY23 and delivered on all fronts including margins and attrition. As a result, the company still outperformed the broader IT pack in the year.

We believe that once noise around recession settles down and the business picks up again, the IT story will be back to the fore. With valuations looking much better now as compared to a year ago, the earnings performance could lead to decent stock returns.

Info Edge

We held Info Edge for its rock-solid core business and continued thrust on divesting the new age

investments through the stock market and other routes.

The start-up funding winter has led to a general decline in new-age companies’ valuations. The same happened to Info Edge’s portfolio companies as well and as a result, the stock price suffered.

We believe that the overhang in the new-age businesses will continue for some time, which is why we have continued pruning our exposure to Info Edge.

Divi’s Labs

Divi’s faced significant headwinds on the earnings front as the COVID-related revenue started declining last

year. Given the high earnings base of FY22, it will be hard for the company to post any growth in FY23. As

the company commanded very high valuations at the beginning of the year, a year of earnings decline has

caused a significant de-rating, leading to negative stock returns in the year.

We pruned our holding in Divis by half during the year and continue to monitor the fundamental developments for further actions in the stock.

Summing up

It’s been a challenging year for equity returns and there doesn’t appear to be a pivot in the short run.

However, in the past, such periods of non-performance have proved to be extremely effective in building

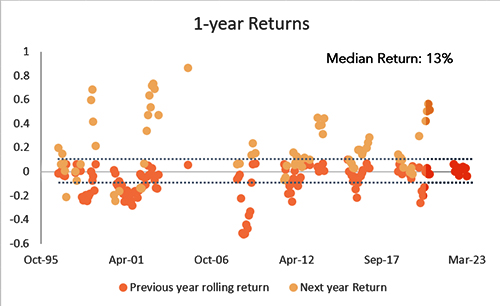

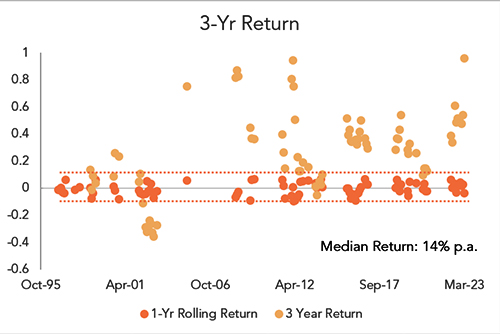

bases for powerful rallies as mean reversion happens in succeeding years. Market data from 1995 says the

same thing. When the Nifty returns ranged between -10% to 7% in the past year, the following year’s

median returns have been 13%, and 3-year median returns have been 14% per annum.

The following charts show one-year and three-year returns distribution of Nifty 50

Source: NSE, Sanctum Wealth

Since we have already witnessed a long correction and sideways action, we believe it’s a good time to start deploying additional funds from a medium to long-term perspective to benefit from the price action that follows such painful periods.

For us at Sanctum, it’s business as usual as we continue to find and back structural themes that we believe will lead the markets. We look for these themes because even with a slow pace of change in some of them, the outcomes are more sustainable and rewarding in the long run.

The past year has been somewhat reassuring as most themes that we were bullish on- banking, capital goods, industrials and manufacturing – ended up doing well. We believe the current themes have a lot of steam left as we continue to study the merits of newer themes to build investment cases for all our portfolio strategies.