Aug 26, 2023

The recession in the distance

• A twenty-month rate hike cycle hasn’t triggered a recession.

• The US economy is defying all odds.

• Past recessions give cues about the severity of market decline from an economic downturn.

• Growth in earnings along with correction has improved valuations of Indian equities.

• The valuations now are back to long-term averages and not excessive.

• Markets would now focus on earnings and fundamentals.

The headline indices continued their momentum in the month, closing with gains of ~3%, while the mid-and-small-cap indices outperformed with gains of 5.5% to 8%.

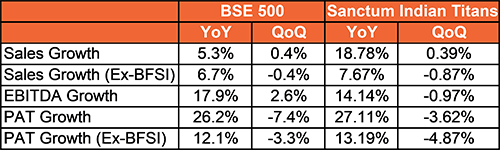

The June quarter earnings are also out, and while the topline growth for the BSE 500 index was slow, EBITDA jumped by 18%, led by moderating input costs. Net income has also seen a decent 26% jump in the quarter. Although, Sanctum Indian Titans’ topline growth was high at 19%, the EBITDA growth lagged because of a high base in a couple of portfolio companies. The net profit growth, however, continues to be robust at 27%, led by a good show by financials.

Q1FY Earnings Overview

Source: Ace Equity, Sanctum Wealth Research

The ongoing momentum, especially in the mid-and-small caps, has got investors concerned about the sustainability of the rally. Despite several indicators suggesting the continued strength of the US economy, concerns of an imminent recession persist due to the compressed rate hike cycle and high inflation. Consequently, worries about the sustainability of the Indian equity rally have been further amplified. Therefore, the most pressing question now is whether the markets have gotten ahead of themselves in the wake of continued macro concerns in the US.

To get some perspective, we delved a little bit into the history to find out how the markets have reacted to previous recessions and what the markets were doing 1) when the economists were anticipating a recession, 2) when the recessions happened, and 3) when the economy recovered.

It’s important to note here that determining a recession is complex, and the outcome is visible with a lag. The official scorekeeper of recession in the US – The National Bureau of Economic Research (NBER) – defines a recession as “a significant decline in economic activity that is spread across the economy and that lasts more than a few months.” The committee tracks various data points, including real personal income minus government transfers, employment, various forms of real consumer spending, and industrial production. However, there are no fixed rules and thresholds that prompt the reviewers to classify a specific period as a recession.

As market participants, we are more concerned about the market reaction to these recessions. Of course, there are economic and social aspects, but given that our local economy isn’t witnessing macro hurdles, we are looking for rub-off effects from global markets.

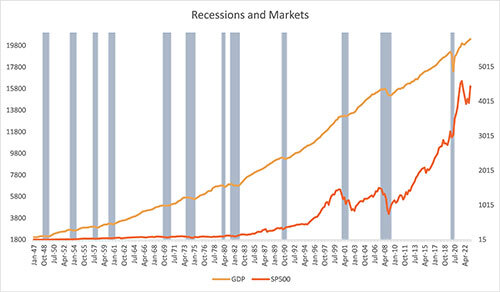

To study these recessions and their market reactions in some detail, here is a chart showing the US recessions plotted alongside the S&P500. To study these recessions and their market reactions in some detail, here is a chart showing the US recessions plotted alongside the S&P500.

Source: Sanctum Wealth Research

The shaded areas in the chart show 12 recessions in the past 75 years, as declared by NBER. The pertinent point is that the market reaction was always determined by the severity of the recession, especially its effects on income and employment. It is also worth noting that the severity of the market fall was also a function of excesses built in the preceding bull run. Whenever these excesses were neutralized before the recession settled in, the market impact was less severe when the actual recession happened. or example, the recession in 2001 was one of the shortest and mildest recessions the US ever witnessed when the economy contracted by 0.3% and the unemployment rate peaked at 5.5%. However, the peak-to-trough market decline in the same period was over 50% because massive excesses were built in the dot com boom.

The next recession in 2008-2009 was much more severe and prolonged, with a GDP decline of 4.3% and a peak unemployment rate of 9.5%. The market decline was also quite severe, with a peak-to-trough decline of 58% in the S&P 500.

The closest to the current economic situation was the double-dip recession of the 1980s. In the early part of the decade, a short six months recession was followed by another sixteen months. The GDP decline in the first dip was 2.2% and in the second dip was 2.9%. However, the overall peak-to-trough decline in the GDP was 2.1% as the economy surpassed the previous peak between the dips.

The recession was caused by an oil price shock from the Iranian revolution that led to a significant increase in inflation, which was already elevated due to accommodative monetary policy at that time. The Fed increased rates from 10.5% to 17.5% in a few months and then dropped them swiftly back to 9.5%, which led to the end of the first recession dip. However, the inflation turned out to be stickier, prompting the Fed to raise rates again by ten percentage points. As the rates were kept higher for longer to tame inflation, it resulted in a prolonged recession, with the peak unemployment rate climbing to 10.8%. Had the Fed not given up on the fight with inflation the first time, the first dip would have been severe, and the second dip wouldn’t have been that severe or may not have happened at all.

When economic downturns were caused by tight monetary policies, in most cases, the recession started mid-way or towards the end of the rate hike cycle and lasted a maximum of three quarters after the end of the rate hike cycle.

Market Reactions

In most cases, the fall in the market preceded the onset of recession, which is natural due to the forward-looking nature of the market. The market bottoms were also made before the economic bottoms. The intensity of fall, as mentioned earlier, was always dependent on previous excesses and the extent of underlying economic weaknesses.

In case of mild recessions, such as the one in 1991, the market saw close to a 20% dip in 3 months, anticipating a recession, and bounced right back, taking to new highs in the next four months even when the recession was underway.

The markets also saw several dips on recession predictions that never materialized. Due to the complexity of recession predictions, most forecasters get their recession predictions wrong. The sheer number of variables impacting an economy and the interlinkages within them are too complex to put in a prediction model. Therefore, most of these predictions turn out to be mirages, and markets shrug them off, focusing on high-frequency indicators and earnings instead.

The current situation

The calls of the current recession were based on the theory that the concerted efforts by the Central Banks to cripple the economies and control inflation by increasing borrowing costs for consumers and businesses would haunt consumption, lead to job losses, and reduce incomes. However, the economy has refused to cooperate so far, even when we are twenty months into the rate hike cycle.

Job growth remains strong in the US, with low unemployment and steady consumer spending. A major saving grace for consumer spending despite high inflation has been the excess pandemic savings that were estimated at $2.1 trillion in the Pandemic, which has dwindled to $500 billion in March 2023.

Therefore, the onset of recession keeps on getting pushed and has now turned into calls for growth slowdown in the last Fed meeting and in the economist circles. The reduced excess savings can be a headwind for spending going forward, however, receding inflation and upbeat employment shall cushion any significant decline.

The markets saw a large correction anticipating a recession, which has neutralized the excesses, especially in the tech sector. With the excesses gone, the market reaction will now depend on the intensity of the recession or slowdown.

Sanctum’s Take

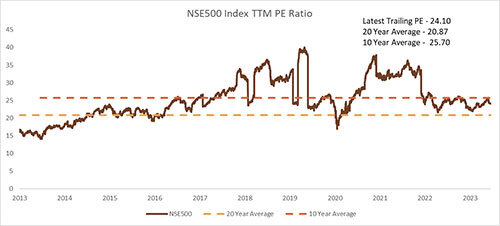

The Indian markets have also seen a one-and-half-year lull when the earnings growth continued to be decent. Nifty earnings grew at a 22% CAGR over FY20-FY23, while the index peaked in October 2021 and slid 18% to its June 2022 bottom. The non-movement in prices and increase in earnings had led to moderation in valuations. After the current rally, the valuations have reached their long-term averages and yet are still not excessive. The following chart shows that Nifty 500 PE has come up but is still hovering below the 10-year average.

Source: Bloomberg, Sanctum Wealth Research

The correction was mainly led by global macro concerns, supply chain issues, inflation and geopolitical concerns. As the world has adjusted to the war, supply chains have been restored, inflation is receding, and the US recession hasn’t materialized, markets would now focus on earnings and fundamentals.

In our portfolio strategies, we navigated through these challenging times by backing the right themes, thereby containing portfolio volatility. In some of the themes we backed in late 2021, like financials and industrials, we monetized the low-hanging fruits. Those themes are now entering a normalization phase and may deliver steady returns but not significant alpha over the benchmark. We are pruning names in the themes and looking at other themes to add to the portfolio.

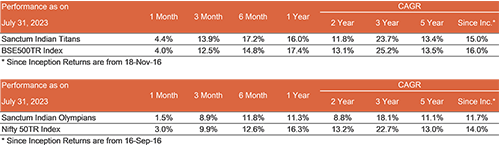

Here is how our portfolio strategies have done in different time frames.

Portfolio Performance