Jun 21, 2023

The Valuation Conundrum

• Nifty seems to be following the valuation discipline quite well.

• Buy-at-any-price is losing steam.

• Entry valuations matter a lot while constructing portfolios.

• Portfolio outcomes are generally better when one doesn’t pay too much.

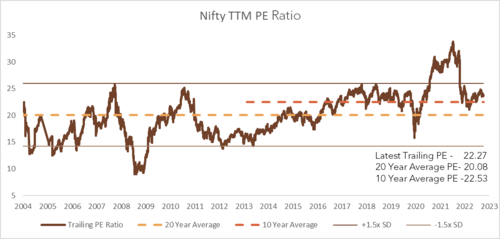

Headline indices ended last month with respectable gains of over 2%, while small and midcap indices closed with robust gains of over 5%. The midcap index surpassed its previous highs and is now trading at its all-time high.

From a valuation perspective, the Nifty is now trading near its 10-year average PE, and above its 20-year average PE as seen in the following chart.

Source: Bloomberg, Sanctum Wealth Research

The chart shows that the index seems to be adhering to its valuation discipline effectively. Generally, it retraces when the valuation approaches 1.5x standard deviation from the mean on either side, excluding black swan events.

When it comes to investing in individual stocks and portfolios, there is an ongoing debate on whether valuations should matter when investing in fundamentally strong companies with competent management. Investors often view these companies as perpetual compounders and believe investing in them anytime can lead to favourable outcomes.

While it is generally true that these companies tend to perform well over the long term, the results can vary significantly depending on the valuations at the time of investment. To assess this, we conducted a study starting from the year 2003, wherein we created portfolios consisting of fundamentally strong companies. We elected the top performers in the past 20 years and filtered them based on the following fundamental parameters:

1.Starting market cap above Rs. 500 crores.

2.Return on Capital Employed (ROCE) above 12%.

3.Last five years’ sales growth above 10%.

4.Product/Service leadership.

5.High promoter integrity.

The resultant portfolio, consisting of some of the most reputable and well-established companies, was assumed to be constructed at the beginning of 2003.

Before analyzing the performance of this portfolio, there are three important points to consider:

Survivorship Bias:It is important to note that this portfolio and its exceptional returns may suffer from survivorship bias. Many companies that initially showed characteristics of perpetual compounders were not included in the portfolios because they dropped off the radar during the study period.

Recency and Familiarity Bias:All the companies included in the portfolio are now well-known brands with a reputation for significant compounding over the years. Therefore, the sample may exhibit a bias towards recent and familiar companies.

Rear-View Mirror Perspective:This exercise is based on historical data and lacks the complexities and emotional aspects involved in real-world investing. It does not account for the challenges and emotions that investors experience during portfolio construction.

Having acknowledged these points, we can proceed to examine the performance of the portfolio.

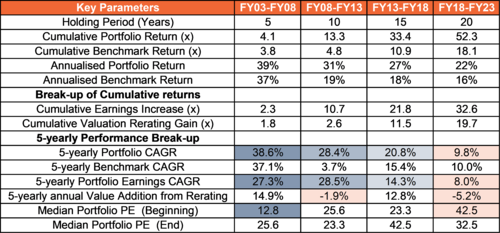

The findings of this portfolio are in the table below.

Source: ACE Equity, Sanctum Wealth Research

The 25-stock portfolio has shown remarkable performance over the past two decades, multiplying approximately 55 times. While a significant portion of this growth can be attributed to earnings growth, a considerable part has also come from valuation re-rating, thanks to the reasonable entry valuations.

However, it’s important to note that most of these returns were concentrated in the first decade, while the later decade witnessed lower annualized returns. The moderation in returns can be attributed to an increase in valuations.

Interestingly, the stocks initially considered to be long-term compounders lost their return potential in the last five years, underperforming the benchmark index (Nifty50). In fact, the valuation aspect hurt returns during this period. This highlights that the entry valuations did impact the returns of these stocks in the recent years.

There are several key points to consider regarding this portfolio and the underlying philosophy of buying at any price.

Firstly, these stocks have evolved into well-established and large-cap companies. Many of these companies were small caps in the early 2000s, experiencing robust growth during their nascent expansion phase. However, as these companies matured and their businesses reached saturation, their growth slowed significantly. Additionally, the expanding valuations made it challenging to replicate the exceptional returns seen in the past.

The initial low valuations were crucial to these companies’ ability to compound effectively. It is unwise to assume that these past winners will continue to deliver the same level of performance or outperform relative to the index, especially considering the significant increase in average valuations.

In the Indian context, another factor contributing to high valuations was the scarcity of businesses with honest promoters. Companies that demonstrated integrity commanded a premium due to the limited availability of such enterprises. However, while dishonesty has not been completely eradicated, it has significantly reduced in corporate India, leading to a dissipation of these scarcity premiums.

In conclusion, blindly buying previous winners at any price may not be the most effective strategy for long- term compounding. Entry valuations play a crucial role, and even with average earnings growth, decent results can be achieved if the entry valuations are reasonable.

It’s a stock picker’s game.

As investing can’t be done by looking in the rear-view mirror, it is essential to continuously explore new ideas that can become future compounders. While this approach may increase the failure rate in the portfolio, there is scope for significant alpha generation if some of those new entrants deliver multi-bagger returns. This outcome predominantly occurs when one avoids overpaying for valuations at the outset.

Most new ideas that are unresearched don’t trade at inflated valuations, therefore, provide a huge head start to the portfolio manager. The same was the case with most of the stocks in the portfolio above in the initial years of compounding.

To identify rapid compounders, one needs a combination of a commendable track record, potential for explosive earnings growth, and an affordable valuation. Careful selection of just 3-4 promising picks in the portfolio can significantly contribute to delivering respectable returns.

Striking a balance

At Sanctum, we try and get the best of both worlds. To deliver less volatile returns to our investors, we have dedicated a part of our portfolios to well-known brands that are still outperforming on the growth front, and there is another part where we strive to find future compounders that can add alpha to portfolio performance.

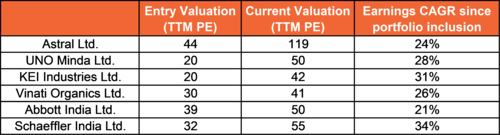

In the Indian Titans portfolio, we have identified several notable compounders, such as Vinati Organics, KEI Industries, Schaeffler India, Astral, Abbott India, and UNO Minda. These stocks were initially acquired at reasonable valuations and have since experienced significant valuation re-ratings due to their impressive earnings growth over the years. The entry valuations and subsequent earnings growth of these stocks are presented in the table below.

Certain stocks from this selection demonstrated exceptional performance amidst the turbulence of the previous year, thereby contributing to our ability to deliver consistent results during this period.

A well-balanced portfolio and a preference for reasonable entry valuations not only help us maintain a decent margin of safety, but also facilitate a stable performance in our flagship strategies.

Renowned investor and author, Philip Fisher, eloquently expressed the essence of true investment objectives, “the true investment objective of growth is not just to make gains but avoid loss.” With our risk- first approach and commitment to growth at reasonable prices, we diligently strive to achieve this objective.

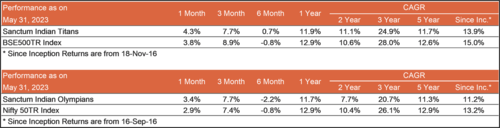

Portfolio Performance