Apr 3, 2018

Performance review and attribution for Sanctum’s in-house flagship DPMS portfolios as well as broad-based market.

Sanctum Fundamental DPMS Performance Attribution

Sanctum Indian Titans Performance

All good things must come to an end. We are referring to the streak of seven consecutive quarters of gains in Sanctum Titans, starting with the quarter of our inception as a company, coming to an end.

The March 2018 quarter failed to breach the highs of the previous quarter. During the quarter ended March 2018, the Nifty was down 4%, and down 9.1% from intra quarter highs, while the Nifty Midcap 100 Index was down 12%.

While Sanctum Titans Outperformed by 18%+ in CY 2017 vs the NSE 200…

….It is Just 1% Below the Benchmark During the Recent Sell-off

Hedging

We entered hedges in Sanctum Titans on January 25th, 2018, and managed to arrest some impact of the deep cuts in the market post budget. Our stated intention was to utilize 70-80 bps of performance to hedge the portfolio. In addition, we were at approximately 12-13% cash. Our effective hedge amounted to 60-65% of the portfolio.

Sanctum Titans finished the quarter down 6.5%, 1.0% worse than the benchmark NSE 200. Considering we outperformed by 18% over CY 2017 on the upside, we would posit that a 1% underperformance should be acceptable on the downside.

We’re on our way to outperforming YTD based on recent action in April. However, we’re not satisfied. Going forward, we will be evaluating higher levels of protection via puts as well as evaluating alternative methods of protection should the markets demonstrate continued weakness.

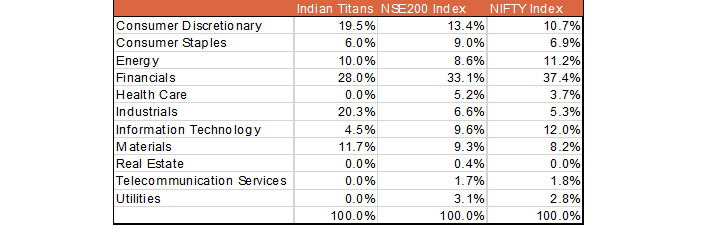

Sectoral allocation

The portfolio construct is to benefit from the thematic trends that provide strong tailwinds. Since some of our themes are driven by strong domestic fundamentals, our portfolio has tended to be domestic focused in nature, and heavily under-weight the export-oriented sectors like Information Technology and Healthcare.

While the portfolio is under-weight on Financials, it has zero exposure to PSU banks, while is overweight Private Banks and NBFCs.

Sanctum Titans Has Zero Weight to Health Care and Only 4.5% to Mid Cap IT

Positioning

The recent action in the market suggests that dispersion in performance is likely to be wider this year. Stock selection will play a crucial role in delivering performance. We continue to remain protected to the downside, with put protection at levels around 10,000 on the Nifty. Should the market have room to run, we will participate on the upside.

We remain confident that over time, the stocks in our portfolio will generate substantial, predictable and consistent earnings growth. That will lead to outperformance relative to the benchmark and attractive returns over longer horizons.

Sanctum Indian Olympians Performance

Sanctum Olympians Remains Flat YTD Despite a Strong Sell-off…

…While Outperforming the Nifty50 by 9.9% in the Past Year…

Sanctum Olympians is our large-cap, quality growth portfolio from the Sanctum stable, a concentrated strategy with just 12-15 quality large cap ideas. The strategy has benefitted with its low allocation to cyclicals and export-oriented sectors.

Here as well we had taken effective hedges during the quarter, which aided the out performance of the portfolio.

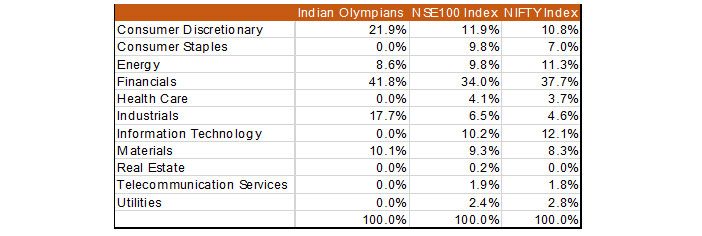

Sectoral allocation

Our strategy remains the same here as well in terms of portfolio construct with key contributors from the consumption and financials sectors. Though we are over-weight financials, we are zero weight on PSU banks and over-weight on Private banks and NBFCs. In addition, we are overweight Autos, Industrials and Consumer Discretionary, while market weight Energy and underweight Health Care and Telecomm.

Positioning

Sanctum Olympians is a concentrated strategy with the highest quality large caps, with reasonable valuations and strong track record of earnings growth, superior competitive positioning and strong earnings visibility. It has held up in performance during the recent correction admirably. For investors with concerns about exposure to mid or small caps, Sanctum Olympians delivers strong steady returns, that would be in excess of benchmark. With an earnings growth profile of roughly 18% CAGR, plus hedging, we are confident that these names will generate outperformance over the benchmark in coming quarters.

Investment Outlook

Petro Yuan, China’s Response and Positioning Spell Concern

The launch of the petro yuan oil futures contract in Shanghai is part of the master plan that China has launched to challenge the dominant positioning of the dollar, ergo the U.S. The recent trade war rhetoric targeting China makes more sense when viewed in this context. Transacting via yuan for crude purchases is a direct assault on a system that has been in place for decades, and afforded the U.S. the luxury of issuing currency as and when desired.

We’re hard-pressed to view the petro-yuan gaining meaningful acceptance in a true global sense; however, the symbolism of the move is worrisome. In combination with the tariffs announced overnight, we’re now of the view that this is likely to elicit further response from the U.S. The add on worries are the rise in input costs that are already making their way into the U.S. data, which suggests a worrisome factor on the inflation front.

Three Steps and a Stumble…

Edson Gould in a study of Fed hikes from the 1930s to the 1970s suggested that three rate rises by the Fed usually led to a stock market correction. The simple rule is still relevant, and we’re in the midst of a correction, post three Fed hikes. That being said, it’s also true that the stock market has predicted 9 of the past 5 recessions. That’s a quote by the famous economist and nobel prize winners Paul Samuelson.

It’s difficult to find signs of oncoming recession. While the European PMI disappointed last month, it remains at healthy levels signifying growth. Domestically, there’s no sign that things are worsening. We expect earnings season to deliver along the lines of the prior quarter: good numbers in most consumer facing sectors, and Industrials, but weighed down by losses from PSU banks and telecom.

What’s incontrovertible, however, is that valuations remain high by historical measures, and markets are adjusting to the new reality: a Fed that is hiking, a Fed that is reducing its balance sheet, embedded volatility and leverage in parts of the global financial system, and trade war worries. So while an economic recession may not be visible on the horizon, a reset on valuations is a healthy path for the markets.

Indicators at Crossroads

All manner of indicators are now sitting on crossover edges, meaning on the edge of a breakdown or possible reversal. Gold appears ready for an upside breakout. Our equity markets on the other hand, are desperately trying to claw back above the 200 day moving average. Bond fund king Gundlach recently pointed out that the Finance and Tech ETFs in the U.S. have only recently approached highs made in prior recessions. With Tech breaking down in the U.S., these ETFs could provide meaningful information on the the direction of markets.

Focus Shifts to Earnings

All eyes shift to Q1 CY18 earnings. Stocks with strong fundamentals are likely to be handsomely rewarded and disappointments likely to be punished. 2018 looks to be very different from 2017. We think quality, predictability and stability will be the factors that receive a premium. Mid and large caps are likely to receive equal interest, but the environment for small caps is decidedly murkier. Divergence versus the index is likely to be much wider than 2017.

Is This Time Different?

Over the past few years, it was around these times with rising fear and uncertainty that the Fed would announce a QE package and markets would roar higher. We wonder if we’re likely to see a repeat. Powell seems to be giving signals that he’s comfortable with deflating some of the euphoria around equities. However, one cannot dismiss this as a possible outcome, with yet another hurrah for the markets.

Equity

The predominance of indicators continue to lead us to prefer defensive positioning. That means hedging the downside while leaving exposure to the upside. There’s a few different ways to play this, via puts, long dated puts and futures. We believe all three scenarios have merit, and are different enough to meet most investors risk exposure preferences.

Gold

We raised our Gold weighting in our asset allocation profiles last fortnight, but remain marginally underweight Gold versus our strategic asset allocation weight of 10%. Gold could certainly have some upside based on the charts, but we don’t see an explosive move in the offing.

Fixed Income

Over the past few weeks, and in our last fortnightly, we indicated that interest rates looked like they were peaking. The recent action in the bond market seems to suggest that rates have likely seen a top for the near to mid term.

On debt, duration was the best performing asset category last week on the massive move of roughly 30 bps~ on yields. We don’t think this downtrend has legs though. The government has kicked the can down the road a few months.

The Finance ministry should be lauded for taking an out of the box approach to debt management and demonstrating sensitivity to market participants demand. The government chose to borrow only 52% in the first half; versus the 60 – 65% that should normally be the case. We’d agree with the assessment that if the ministry had not come forward with the debt plan, the 10 year could easily have risen higher towards 8%.

Challenges remain. In particular, the implementation of the e-way bill could lead to significant and continued teething problems. That’s what we’re hearing in conversations with business operators. Should the e-way bill create inefficiencies, or GST borrowings not come through at higher levels, the government could again witness pressure on rates later this year.

We continue to believe corporate credit is the safest place to park funds. There is a possibility that the government could further act on releasing pressure on yields by increasing the FI investment limits on debt. We’re most comfortable sticking with corporate credit.

We expect the RBI to stay on hold in the upcoming monetary policy meet. The case for raising rates appears thin with inflation within the range of comfort. The case for lowering rates isn’t strong either.

Broad Market Performance Attribution

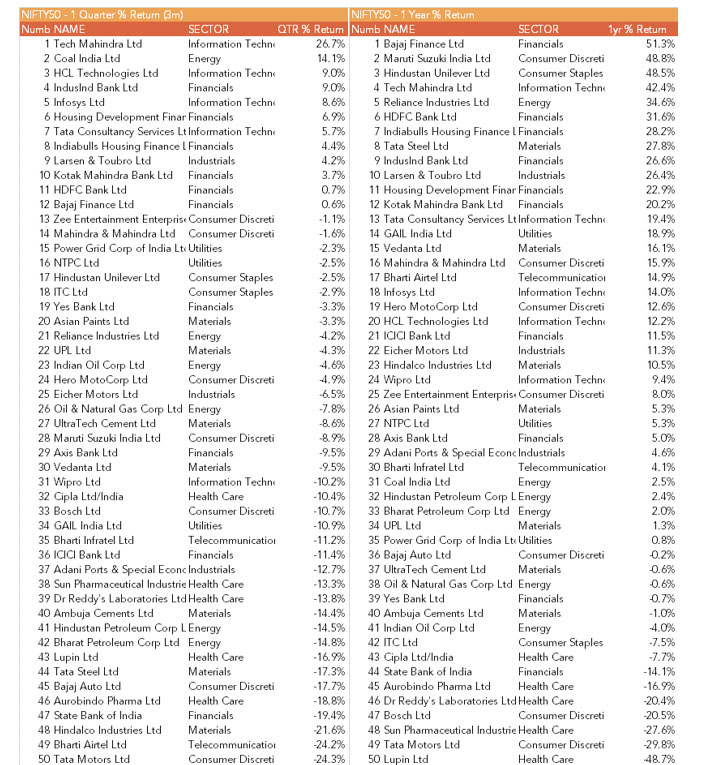

Nifty 50

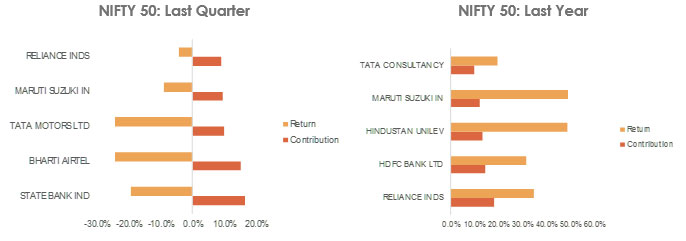

In the quarter gone by (and CYTD), mainly Information Technology (IT) and Financials claimed the top 10 spots as the market flavor shifted towards under-owned large-cap IT stocks and the non-PSU entities in the Financials space rallied. Tech Mahindra, IndusInd Bank and Coal India were the major winners. At the bottom of the pack were mainly Health Care, Materials (chiefly on account of global trade wars), Energy and Consumer Discretionary names such as the OMCs (HPCL and BPCL), Lupin, Tata Motors and Hindalco.

For the year over year period, only 20 of the 50 stocks delivered hurdle returns of 12% or higher. Financials and Consumer names broadly claimed the top 10 positions. The bottom of the pack constituted mainly Health Care (the usual suspect) and certain Consumer stocks (such as Bosch and ITC).

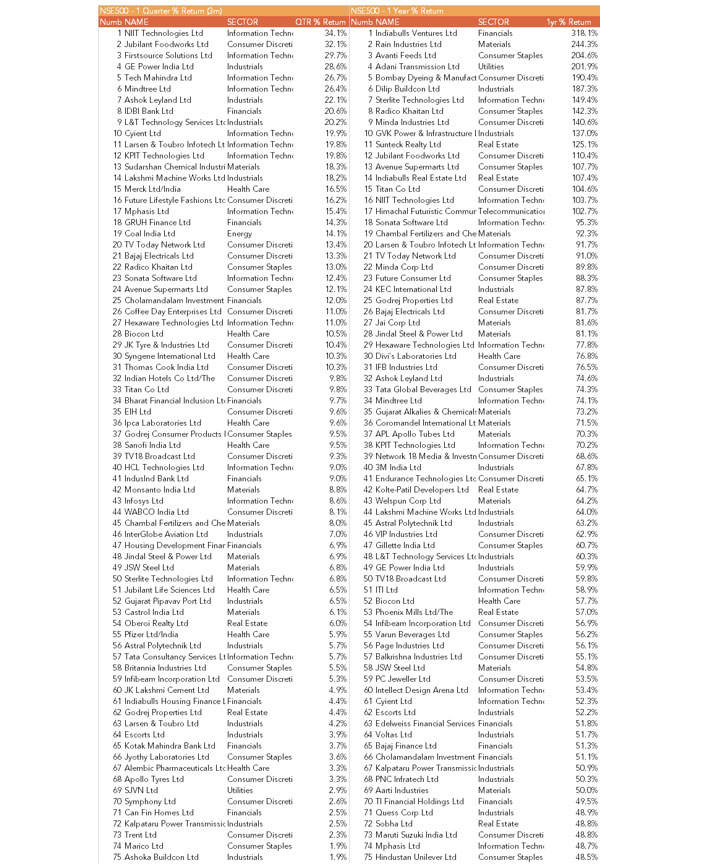

CNX 500

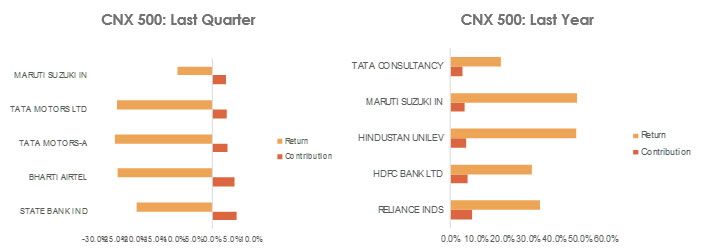

From a quarterly perspective, the CNX 500 top 10 demonstrated much more vigor vs. the NIFTY top 10. Mid-cap IT stocks dominated the top performers.

In the last 1 year, the Consumption theme yet again dominated in the top performers. Indiabulls Ventures was the lone representative in the Financials pack. Only 174 of the 500 stocks delivered 20% or more gains last year, with much of the rally fueled by mid-caps. Select Consumer names constituted the bottom of the pack.

Fundamental Strength Ratings

Based on growth, profitability, margins and valuations we score each company.

Nifty 50

GAIL, Reliance Industries, Yes Bank and IndiaBulls Housing Finance were some of the prime performers in the top 10 fundamentally sound Nifty 50 companies. SBI, Cipla, ITC and Bharti Airtel scored lowest on our fundamental scoring mainly weighed down by poor top and bottom-line performances.

CNX 500

Financials (mainly NBFCs and other related non-banking entities) and Gas and Chemicals affiliated pockets fared extremely well on fundamentals coupled with decently priced valuations.

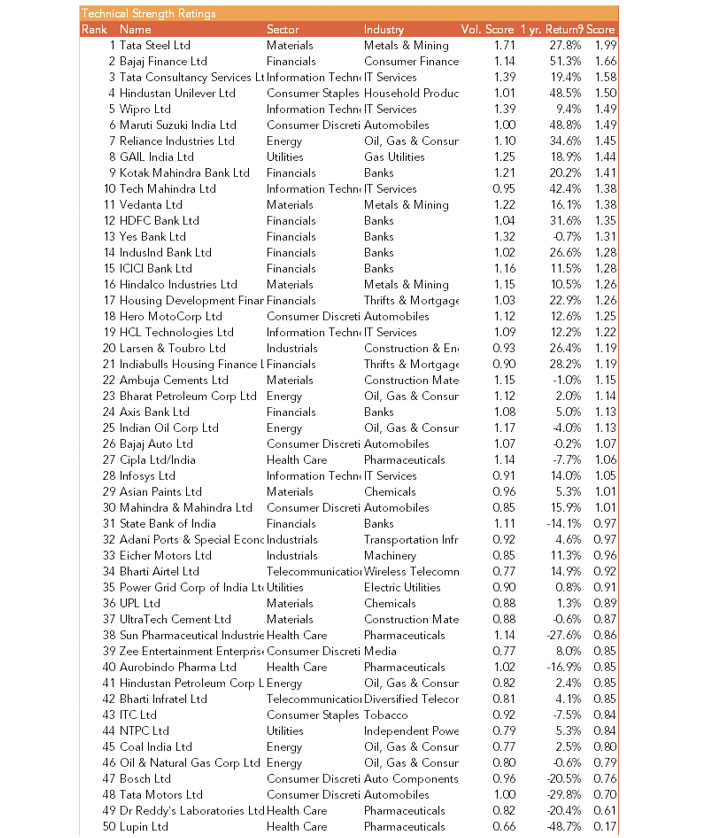

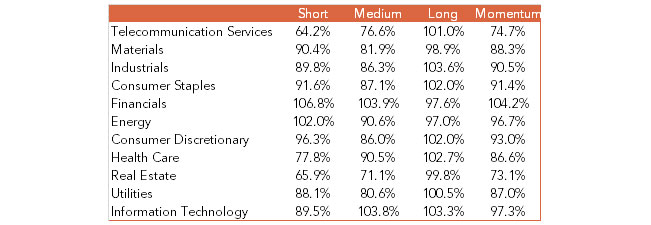

Technical Strength

Our technical ratings tracks technical factors such as volume and momentum as well as returns to come up with a technical score for each company.

Nifty 50

Financials (Yes Bank, Kotak Bank, ICICI Bank and Bajaj Finance – likely a shift in funds from suspected “bad quality” institutions to “high quality ones”) and IT (Wipro and TCS – on the block deal) exhibited strong technical momentum.

On the other hand, negative momentum plagued certain stocks broadly in Health Care (Sun Pharma and Cipla).

CNX 500

Investors chased Consumer Discretionary (Future LifeStyle) and IT (NIIT Tech) though fair amount of selling was witnessed in Financials space (Central Bank of India and Canara Bank on fears of linked frauds).

Much of the action in CNX 500 volumes was seen in the Large cap space on a relative basis compared to mid and small caps.

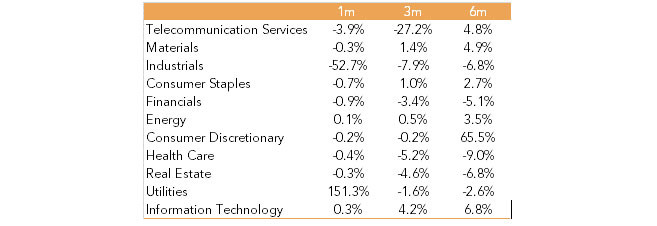

Earnings Revisions

Nifty 50

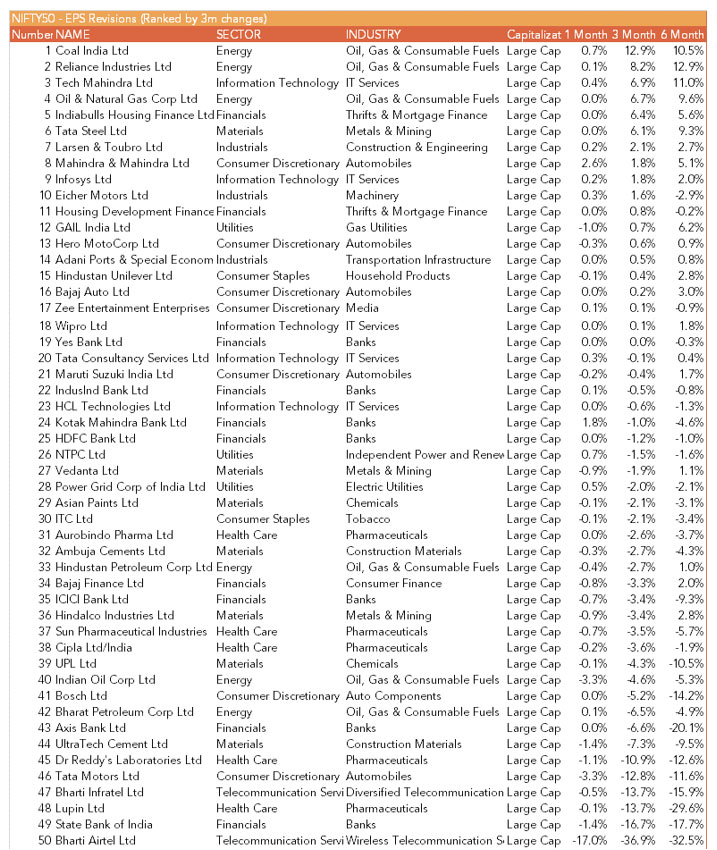

Earnings revisions have been negative on average for Nifty 50 in the last 1 month, though seem to be bottoming out as the last 3 and 6 months have seen much stronger downgrades.

Energy saw the most positive 3m revisions (led by Coal India, Reliance Industries and ONGC likely on the back of a rising Crude environment). IT as well experienced strong bottom line upgrades in the last quarter. Conversely, OMCs and Telecom formed the bottom of the back suffering steep earnings estimates cuts.

CNX 500

The index witnessed a slight tapering of expectations with earnings estimates pulling off highs in the last 1 and 3m, though still above 6m prior estimates.

Mid-cap IT (primarily Internet Software and Services) and Materials (mainly Metals and Mining) led the pack in EPS upgrades in the quarter gone by. On the other hand, analysts have severely cut expectations in Telecom, Industrials (tempering of estimates in Construction, Air Freight and Logistics and Transport Infra) and Health Care CYTD.

Performance Attribution Q1 CY 2018

A deeper analysis of the two flagship indices, the Nifty 50 and CNX 500 across stocks, sectors, industries and market caps reveals insights and implications in terms of portfolio performance.

Nifty 50 Performance – Quarter, YOY

Source: Bloomberg, ACE Equity

CNX 500 Performance – Quarter, YOY

Source: Bloomberg, ACE Equity

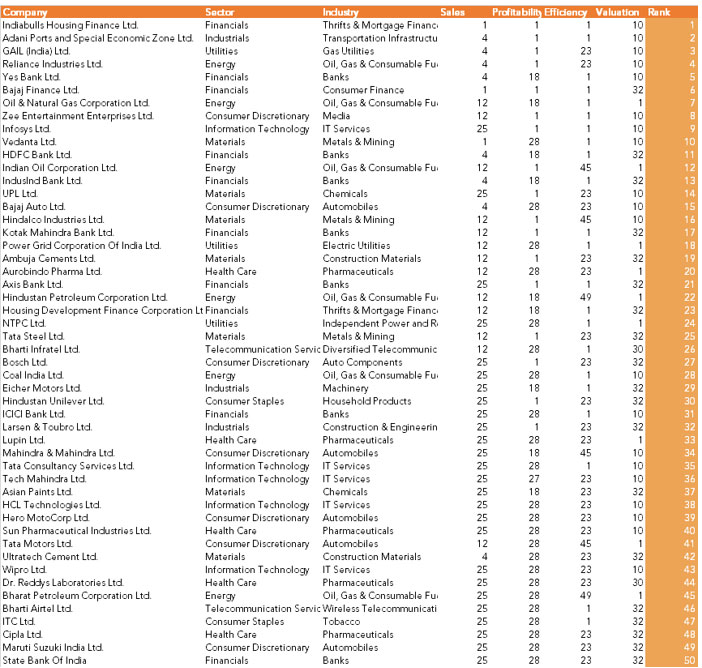

Fundamental Strength Rating – Nifty 50

We rank the Nifty 50 by growth, profitability, margins and valuation below to come up with a fundamental strength ranking.

Fundamental Strength Rating – Nifty 50

Source: Bloomberg, ACE Equity

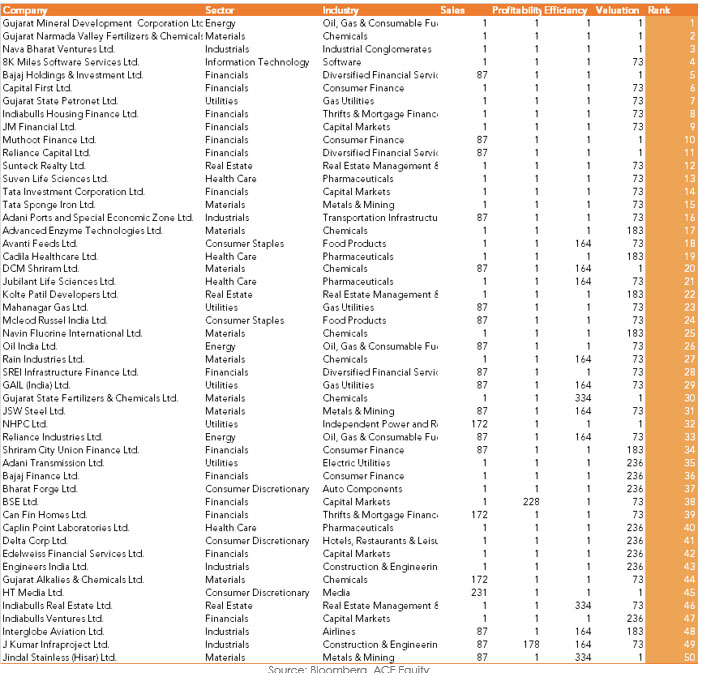

Fundamental Strength Ratings CNX 500

We rank the CNX 500 by the same methodology.

Source: Bloomberg, ACE Equity

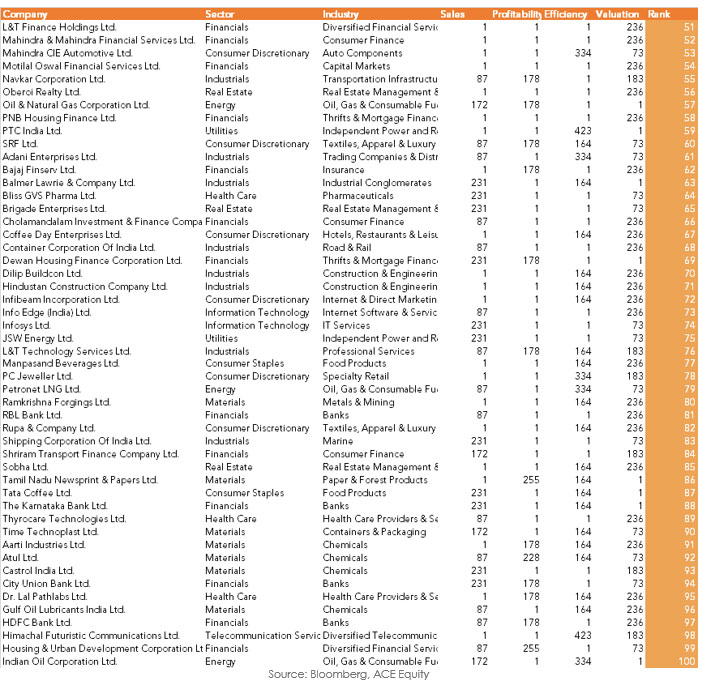

Fundamental Strength Ratings CNX 500 (continued)…

Source: Bloomberg, ACE Equity

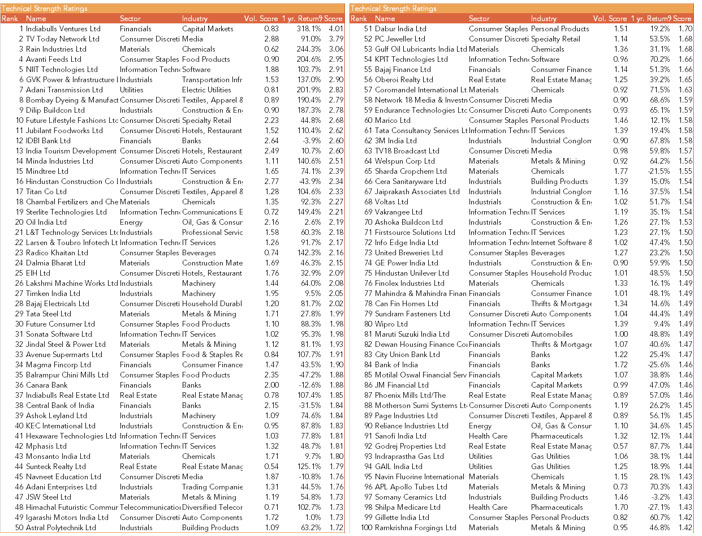

Technical Strength Ratings Nifty 50

Source: Bloomberg, ACE Equity

Technical Strength Ratings CNX 500

Source: Bloomberg, ACE Equity

Contribution Analysis – Returns & Contributions

Source: Bloomberg, ACE Equity

Earnings Revisions Nifty 50

Source: Bloomberg, ACE Equity

Earnings Revisions CNX 500

Source: Bloomberg, ACE Equity

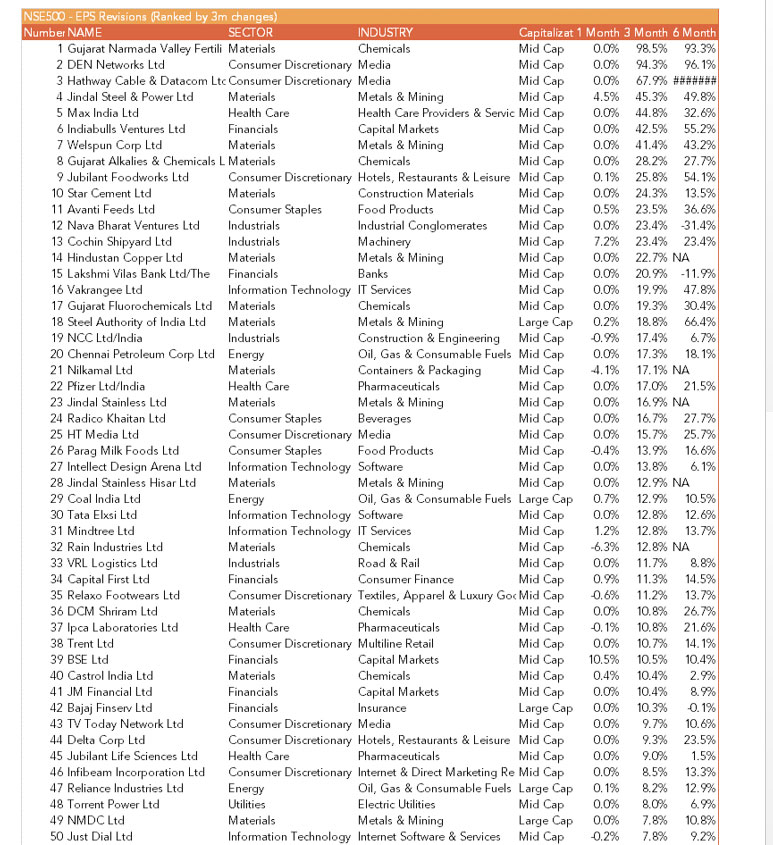

Performance By Capitalization & Sector – CNX 500

EPS Revisions

EPS Revisions at Inflection Points for Large and Mid caps

EPS Revisions Positive for IT and Negative for Telecom

Source: Bloomberg, ACE Equity

Volume

Volume Momentum Is Strongest in Large Caps compared to Mid and Small caps

Volume Momentum Is Strongest In IT (Positive) and Financials (Mixed)

Source: Bloomberg, ACE Equity

Technical Outlook

Truncated last week got off to flying start, but couldn’t make much head way as it failed to show follow-up action. For the week Nifty closed at 10114 levels up by 1.16%. Index has been trading below the 200 day moving average for last couple of weeks. The rising support trend line originating from May 2017 low of 9342 and connecting lows 9449-9775 has been broken and it is now acting as resistance for the market. Also, the 20 day moving average is acting as resistance since the decline started from all-time high of 11172. Thus, on the upside index has resistance around 10230 levels which needs to be taken out for any meaningful bounce back to be seen. Crossing above 10250 odd levels on sustainable basis, index can rally towards 10500 levels. The recent low of 9952 has almost tested the 38.2% Fibonacci retracement level of the upswing from December low of 7894 to high of 11172 which comes around 9920 levels. Index has respected 9920 support level and been holding above this level for last couple of weeks. Breaking below 9920 levels, Nifty will see continuation of decline towards 9740-9680 zone where next major supports are seen while intermediate support is seen at 9830 levels.

Nifty Daily chart