Oct 13, 2023

• Global economy faces headwinds.

• India growth resilient despite global challenges.

• Indian bonds likely to be range bound as RBI counterbalances bond inclusion cheer.

• Better value in large cap relative to mid and small cap stocks in the medium term.

Odd Man Out

Mixed global macro-economic data has now been crying wolf for several months in a row. We believed

there was a higher market risk emanating from data getting weaker, and it turned out to be a humbling

experience. And yet, when we went back to the drawing board to review the data, we are unable to shake

off the unease when we see the global markets rally. Except India. We have believed that after the spate of

reforms, we are setting ourselves up for sustainable growth over the next few years. Of course, there will

be some cyclical elements, but that doesn't distract us from the longer-term growth prospects.

Global Update

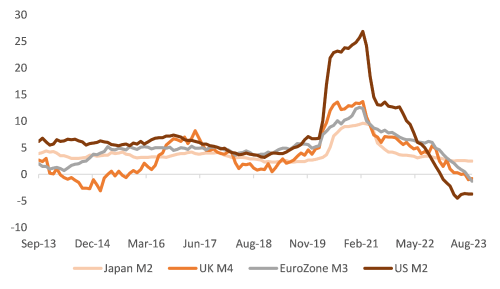

But first, about what we’re seeing globally. Earlier this year, in May, the US government was on the verge

of a shutdown. They ran down their treasury government balance (equivalent of the US government’s

savings account with the Fed) to USD 87 billion. To put the number in perspective, the targeted year-end

balance was USD 600 billion. Between rebuilding treasury balances, financing fiscal deficits and

quantitative tightening by the Fed, the liquidity is being sucked out of their system briskly.

Change in global money supply

Source: Bloomberg, Sanctum Wealth

This has an impact on the bond as well as equity markets. The beginning of October has already seen some of the worst trading days in the US bond markets in years.

Higher rates, tightening lending standards and the onset of a bankruptcy cycle don’t bode well for US economic growth. (As we write this, S&P 500 is considering cutting Brookfield to junk status because the company has substantial amounts of maturing debt to refinance during a time of higher interest rates and lower property values.)

DSP MF’s Netra makes a pertinent point: “History shows that whenever US interest rates have risen beyond the long-term nominal GDP growth rate (4.5% CAGR), corporate profitability suffers a significant slowdown”.

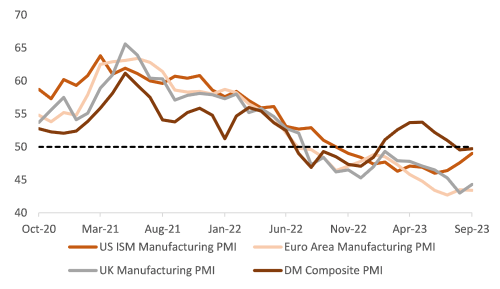

We watch for and acknowledge positive data as well. For instance, the manufacturing sector in the US has been under pressure while services has been holding up. However, the recent DM manufacturing reading indicates some respite, although it is still in the contractionary zone.

Some respite in DM manufacturing activity, yet in contraction zone

Source: Bloomberg, Sanctum Wealth

The obvious response we get to our concerns is that the Fed will bail the US economy out. We can’t disagree, but timing is key. Fed chair Jerome Powell has been constantly hawkish even when data demonstrates a build-up in undercurrents that indicate a weakening economy. In fact, in the last meeting, they dropped their recessionary outlook. So, we looked at the Fed’s forecasting track record, which is not impressive. From 2008-2018, both growth and inflation undershot the Fed’s expectations consistently. In the 1973-75 recession, they were sanguine for most of 73 and did not acknowledge much later that the economy was in recession. The story wasn’t different in 2008 either. The over-tightening/over-easing can be attributed to these forecasting issues. This explains why, in the past 25 years, the Fed hasn’t started a rate cut cycle unless something broke. We think history in 2023 will rhyme again, if not repeat.

Germany, the world’s third-largest exporting country, is in recession.

China’s property slump is gaining salience again as Country Garden, a property giant, warned it could default on its debt. The combined outstanding debt of Evergrande (already defaulted) and Country Garden, is over USD 500 billion. The wealth effect is deeply impacted because property accounts for over 65% of household wealth in China. Hence, despite policy support, economic recovery could remain fragile. These woes already reflect in the performance of Chinese equities. The MSCI China index is the worst performing so far, and the index is down 20% from its 2022 peak. It is worth noting that China valuations are fairly cheap at roughly 10x and a contrarian call could play out favourably.

The pessimism in sentiment has spilt over to EM as a whole. Bloomberg points out that MSCI EM is at the weakest-ever level relative to the S&P 500 Index in data since 1987. Trends like these tend to mean revert and richly reward patient investors.

Emerging Markets stocks sink vs. US peers

Source: Bloomberg, Sanctum Wealth

Oil is another variable that should be closely watched. Production cuts and potential disruption due to the Israel – Palestine war could imply elevated price levels. This not only affects the Indian current account deficit and the currency but also complicates the global growth-inflation dynamic. Past Israel conflicts show that it’s not been a big mover of oil prices; hence we are not changing our overall view for now.

India Update

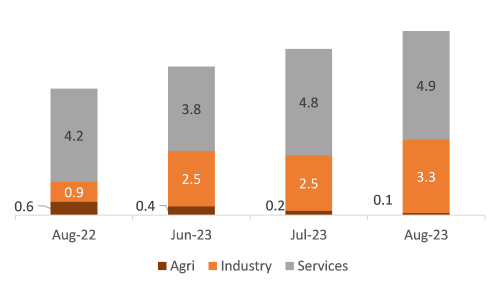

Earlier in this note, we said that India’s growth looks strong. Both industrial and service sector activity

reflects this. Manufacturing activity has been expanding for 27 straight months. But we are also noting

some softening of pace since April. Similarly, GST collections continue to be more than Rs 1.4 lakh crores

for 19 consecutive months. The September numbers are marginally lower than the April highs but strong,

nonetheless. The average monthly gross collection this fiscal is 11% higher than same period last year. Net

direct tax collections till mid-September ’23 is up roughly 24% this year.

Contributions of sectors towards growth (pp)

Source: Bloomberg, Sanctum Wealth

The much-awaited announcement of inclusion of Indian bonds in JP Morgan’s global bonds indices finally came through. Structurally, this is a positive for India. However, we believe that immediate gains might be capped due to RBI’s interventions. The RBI, in its most recent monetary policy committee meeting, decided to hold rates unchanged while continuing its stance of ‘withdrawal of accommodation’. This was largely in line with market expectations. However, there was a surprise announcement of Open market operations (OMO) through which the RBI intends to drain liquidity further. Given the global ‘high for longer’ stance, RBI is expected to choose to maintain rate differentials with developed market bonds. We expect this to be achieved by direct market interventions without further rate hikes.

Outlook

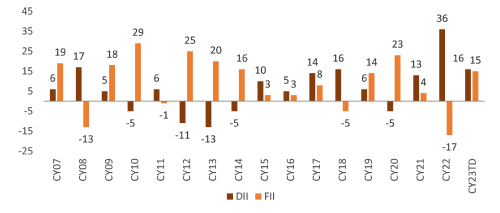

Indian equities, after touching record highs mid-month, pared gains. FIIs sold about USD 1.5 bn in Indian

equities. Domestic flows continue to be supportive. Monthly SIP flows have now touched 16,000 crores,

another all-time high.

Equity flows year on year

Source: Bloomberg, Sanctum Wealth

Mid and small caps continue to lead the market rally. NSE Small cap and NSE Midcap 150 indices have rallied over 40% and 35% respectively. Nifty 50’s 14.7% return pales in comparison. Adjusted for the expected higher growth expectation from mid and small cap companies, we continue to believe that large caps currently offer better value. Momentum may favour smaller companies, and even those that are not necessarily hallmarks of good quality, we prefer to manage risk (lower drawdowns) and are willing to sacrifice some upside in the bargain. This is a theme that reflects across our equity as well as multi-asset class portfolios.

Finally, we had downgraded gold to be closer to neutral weight. We had mentioned that we would reduce gradually based on technical cues. Our model does not incorporate geopolitical risks as these are not quantifiable easily. In light of the current situation, we are deferring further reduction in weights in our portfolios. We are circumspect in adding more weight tactically, considering the unfavourable taxation of Gold ETFs and lack of liquidity (for exit) in sovereign gold bonds.