Sep 18, 2023

• Global equity momentum moderated in August amid weak economic data.

• US economy is showing resilience, but conflicting data continues to emerge.

• Eurozone is at a greater risk of recession as it faces stagflation.

• Indian fundamentals strong; risk likely to emanate from global factors.

• We look at add equities on dips; prefer large caps over midcaps.

Still Very Fuzzy

As we enter the final quarter of this calendar year, the global financial markets find themselves at a crucial juncture. While we are nearing the end of rate hike cycle, the full impact of a very steep, synchronized global rate hike cycle has yet to be fully reflected in macroeconomic indicators. In contrast, global equity markets have displayed robust momentum, even as global bond yields have moved up sharply. However, both equity and bond markets corrected in August, primarily driven by rising oil prices and strong service sector data in the US, which increased concerns about a more hawkish Fed. The outlook remains very fuzzy amid disparity in incoming data.

Global Macro Update

Strong economic data in the US prompted the Atlanta Fed’s Nowcast to project US GDP growth for Q3 2023 at 5.9%. While this is an initial forecast subject to multiple revisions, it underscores the resilience of US economy. Nevertheless, conflicting data continues to emerge from the US. The US ISM Services PMI, which favours larger companies, including those in the public sector, exceeded expectations at 54.5. In contrast, the S&P Services PMI, which exclusively focuses on the private services sector, was revised downwards to 50.5. Both the ISM and S&P Manufacturing PMI exhibited improvements compared to the previous month.

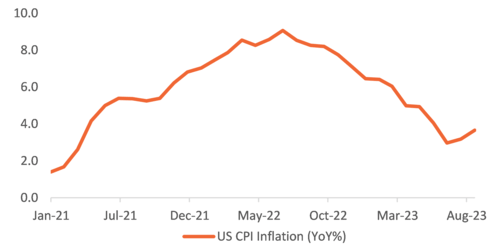

Similarly, the US labour market report indicated an increase in new job additions, but a significant rise in the available workforce pushed the unemployment rate to 3.8% from 3.5% in the last month This uptick in unemployment can be an early indicator of an economic slowdown, but we need to monitor its trend. On the inflation front, US CPI inflation rose to 3.7% in August due to sharp increase in energy prices, while core inflation decreased to 4.3% in August from 4.7%. US inflation appears to be moderating but remains above the Fed’s target range.

US inflation starting to moderating

Source: Bloomberg

A spike in oil prices, following Saudi Arabia and Russia’s extended output cuts, further complicates the inflation outlook. This marks the third cut in the ongoing OPEC+ output reduction cycle. Historically, OPEC+ Investment Strategy 15 September 2023 has limited these cuts to 2-3 at a time. Without further supply cuts, given global economic slowdown, oil may not pose a significant issue. However, if additional cuts are implemented, there is a possibility of global inflation rising once again.

Despite the higher inflation reading and increased manufacturing activity, most analysts expect the Fed to remain on hold later this month, with fewer than 40% expecting a rate hike in the November policy meeting. We believe, the Fed may stay on hold for the foreseeable future.

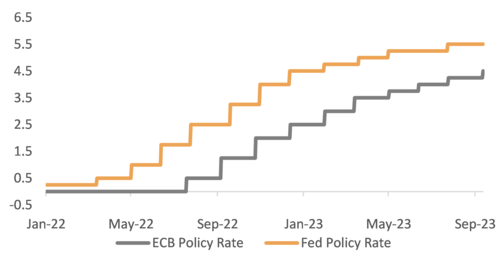

In contrast, European macroeconomic data has been disappointing. The Euro area is grappling with stagflation, high inflation, and low growth. Both manufacturing and services PMIs, along with decline in German factory orders, signal slowing economic growth. Furthermore, core inflation in the Euro area is significantly higher than in the US. The ECB has also maintained a hawkish stance amid elevated inflation pressures and a tight labour market. ECB rate actions have lagged Fed’s as a result, the ECB may need to take further measures to control inflation in Europe. Consequently, the risk of recession in Europe appears much higher than in the US.

ECB has lagged Fed in raising rates

Source: Bloomberg, Sanctum Wealth

Upper end of Fed’s target rate band and ECB main refinancing operations rates depicted

Recent Chinese economic data shows some signs of marginal improvement, but the data is still overwhelming negative. At present, we observe targeted supportive measures aimed at specific sectors of the economy, but achieving transformative change will necessitate substantial government intervention. Although the recent measure to stabilize property sector have helped calm the market and may contribute to a near-term rebound, a long-term rally in Chinese equities will require more decisive measures from the government.

Global Market Update

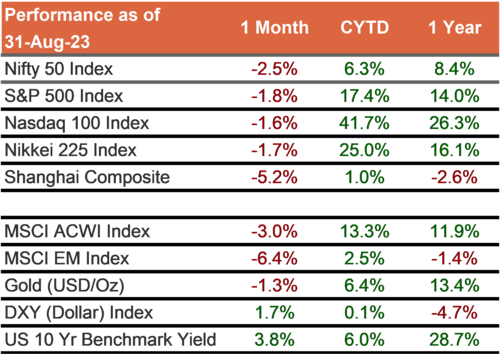

Amid stronger-than-expected growth in the US and concerns about higher interest rates, global equity markets corrected last month. Emerging market equities fell more than their developed market counterparts, partly due to a stronger USD. China, in particular, was a major drag, with issues in the Chinese property market leading to correction in Chinese equities.

Source: Bloomberg, Sanctum Wealth

All data is in local currency and represents price returns.

In August, bonds, much like equities, experienced corrections. The rise in bond yields was driven by heightened concerns about inflation and hawkish central banks. Additionally, the US Treasury significantly increased debt issuance following the recent debt ceiling standoff, and this trend is expected to continue for the next few quarters. Two additional factors weighed against US bonds: a less attractive carry trade for Japanese investors due to adjustments in Japanese yield curve control and concerns about the rising US fiscal deficit. Despite these challenges, US yields at their current levels remain attractive.

India Market Update

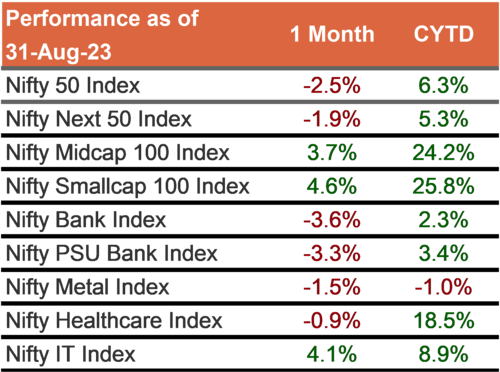

In line with global equity markets, Indian equities also took a pause last month. FIIs turned net sellers after significant purchases in the previous four months. While large-cap stocks delivered negative returns, more domestically focused mid and small-cap stocks continued to outperform and posted positive returns last month as well. Sectors like IT, consumer durables, and capital goods led the gains.

Source: Bloomberg, Sanctum Wealth

The above returns are price returns

Tactical Asset Allocation | Quarterly Asset Pairs Review

Following the release of corporate earnings results, the Sanctum Investment Committee convened to deliberate on our proprietary asset pair model, which plays a pivotal role in shaping our tactical asset allocation decisions and model portfolios. For this quarter, the model indicates a modest overweight for equities, particularly favouring large-cap stocks. Scores for other asset pairs are neutral.

Equities vs Bonds

Flows, earnings supportive, but global headwinds a concern

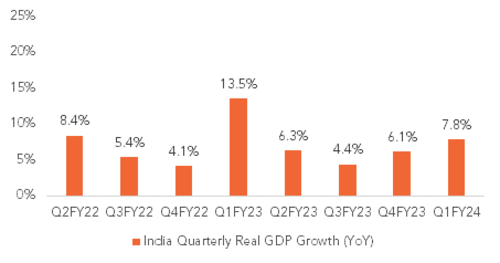

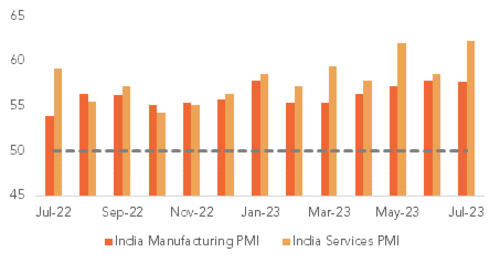

India’s Q1 FY24 GDP grew by 7.8% in line with consensus estimates but slightly below the RBI’s projection of 8%. This growth was driven by a resurgence in contact-intensive service sectors such as hotels, transportation, and communication, along with increased investment activity, notably due to front-loaded government capital expenditure. This economic momentum is reflected in high-frequency indicators like PMI, GST collections, e-way toll collection, and core industry growth as well. However, potential headwinds include a below-normal monsoon attributed to El Niño and the lagged impact of rate hikes, both globally and locally, which could affect economic activity in the coming quarters.

GDP growth in line with expectations

PMI data also remains strong

Source: Bloomberg, Sanctum Wealth

The latest quarter’s results displayed robust earnings momentum, with the Nifty reporting 32% earnings growth in Q1 FY24, exceeding analyst expectations. This growth was driven by the BFSI and Auto sectors, while the healthcare sector also showed signs of recovery. However, sales growth remained in single digits. A similar pattern was observed in the broader BSE 500 index, with top-line growth at 5.3%, while EBITDA and PAT grew by 17.9% and 26.2%, respectively. Margin expansion due to moderation in input prices supported earnings growth, despite modest sales growth in the last quarter. However, going forward, sales growth is likely to be a key driver of earnings as input costs have stabilized, and further margin expansion is unlikely.

Q1 FY24 earnings growth was strong

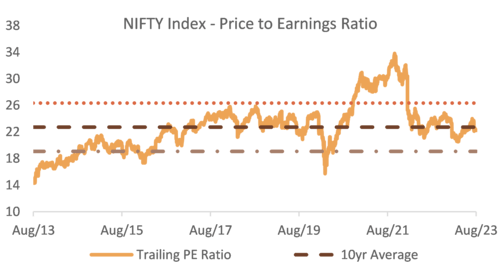

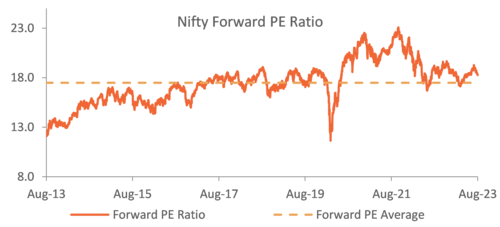

Large valuations close to average

Source: Bloomberg, Sanctum Wealth

While economic activity and earnings growth have remained favourable, the swing factor was the pickup in net equity inflows. Between April and July 2023, foreign investors purchased about USD 18bn worth of equities, marking it the highest four-month inflow ever recorded. Strong foreign flows supported equity markets, leading to a nearly 13% rally in the Nifty during that period. However, as foreign investors turned net sellers in August, the momentum in equity prices also moderated. So far in this financial year, Indian equities, represented by the Nifty 50, have gained over 13%. However, this increase in stock prices has been somewhat offset by a corresponding increase in earnings, leaving valuations close to historic levels.

Overall, while India remains relatively better placed compared to the rest of the world in terms of economic activity and earnings growth, equity flows are a key consideration. Flows can dry up quickly, primarily due to global factors, as India’s fundamentals remain robust. As a result, we recommend investors buy on dips and gradually build their fresh equity allocations.

Large-caps vs Mid-caps

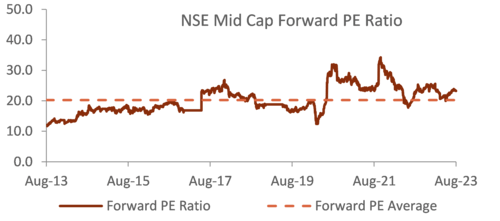

No valuations gap between large and mid-caps

In the current financial year, mid and small-cap stocks have significantly outperformed large-cap stocks, leading to higher valuations for mid-caps. When compared to historical valuation levels, mid-caps are currently trading at a higher premium than large-cap stocks, relative to their own historic averages. Additionally, mid-cap companies have reported lower earnings growth rates than large-cap companies. Consensus estimates also indicate expectations of higher earnings growth for the Nifty in the next 12 months. While technical momentum for mid-caps remains strong, some indicators, like the RSI, suggest that mid-caps may be overbought. Hence, we have turned overweight on large-cap equities.

Midcap valuations now relatively expensive

Source: Bloomberg, Sanctum Wealth

Fixed Income | Corporate vs Government | Short-term vs Long-term

Yields have peaked, credit environment favourable

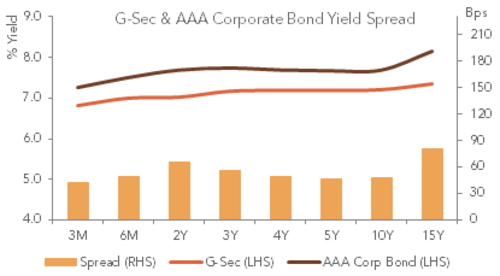

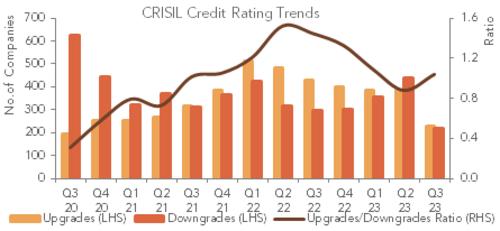

The credit spread between AAA-rated bonds and government bonds remains narrow across the yield curve. As one moves further down the credit curve, there is an opportunity to obtain a decent yield pick-up. The overall credit environment remains favourable, characterized by low corporate leverage and robust earnings growth. However, investors should be mindful of two key factors: the upgrade-to-downgrade ratio has started to moderate, and a significant amount of capital is currently being raised by “performing credit”funds. Consequently, investors need to be selective when investing in these funds.

Corporate spreads remain low

Upgrade to downgrade ratio has moderated

Source: Bloomberg, Sanctum Wealth

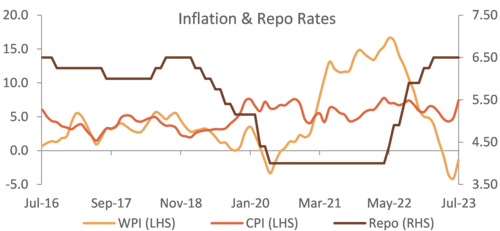

In July, India’s CPI inflation accelerated to 7.44%, driven by an uptick in food prices. Despite this surge in food inflation, the RBI chose to keep interest rates unchanged. However, the rise in inflation pushed the yield on 10-year government bonds to 7.2%. The outlook for food inflation has become uncertain due to the uneven monsoon influenced by El Niño.

Recent inflation spike largely due to food inflation

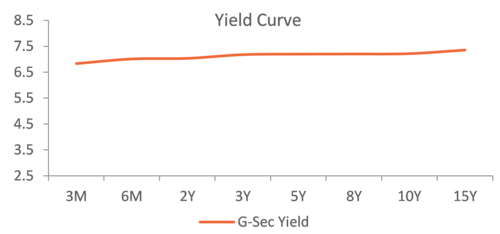

Yield Curve is still flat

Source: Bloomberg, Sanctum Wealth

While the RBI may continue to focus on core inflation (excluding fuel and food), which is currently below 5%, it may need to react to Fed actions. A hawkish shift by the Fed could result in INR weakness, and the RBI may choose to prevent this. Additionally, it is unlikely that the RBI will turn dovish before the Fed does. Currently, our base case is that the Fed may be nearing the conclusion of its rate hike cycle, and the RBI may also maintain a hold. Hence, gains from adding duration are unlikely for at least the next few months. Further a flat yield curve does not compensate investors for the additional risk. We suggest investors match their investment horizon with investment duration.

Gold vs Cash

Fundamentals less supportive of Gold

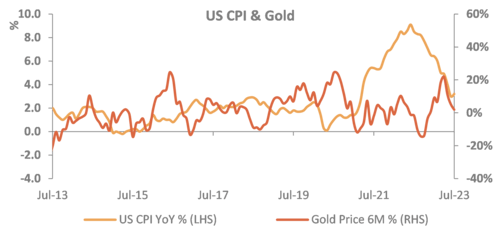

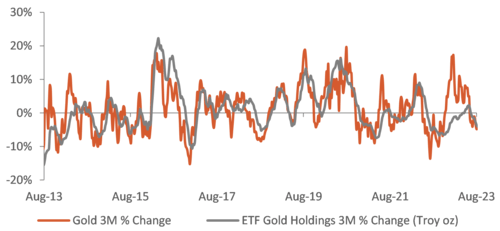

Gold prices have remained range-bound this financial year. The argument for gold as an inflation hedge has weakened due to the deceleration in US inflation. Additionally, gold ETFs have witnessed outflows, partially offset by an increase in net contracts. Consequently, the asset pair model scores have shifted close to neutral for gold. We will gradually reduce our gold overweight when the market provides an opportunity.

Deceleration in US inflation negative for Gold

Gold ETFs have seen outflows

Source: Bloomberg, Sanctum Wealth

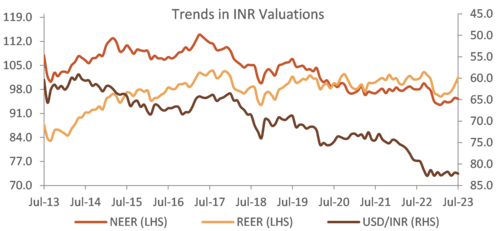

INR vs USD

INR fundamentals strong, but Fed action key risk

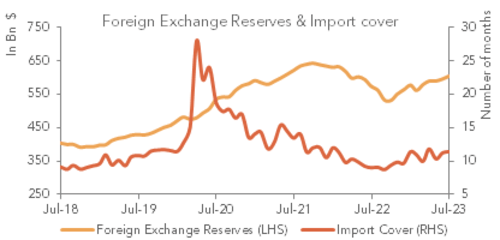

With the INR showing relative strength, it has now become fairly valued. However, fundamental factors support the INR. The RBI has used this INR strength to rebuild its FX reserves. Coupled with favourable commodity prices, the current account deficit and balance of payments have also turned favourable. This is further supported by strong FDI and foreign portfolio inflows. However, the key risk is the potential for a hawkish shift by the Fed, which could result in dollar strength.

RBI has been able to rebuild FX reserves

INR has now become fairly valued

Source: Bloomberg, Sanctum Wealth

Sanctum Multi-Asset Portfolios

Sanctum Multi-Asset Portfolios (SMAPs) serves as a conduit for implementing our tactical asset allocation decisions. We manage investments across three distinct risk profiles: Shield (conservative), Enhancement (balanced), and Generation (aggressive).

Given the rally in Indian equities, their relative weights in our existing SMAPs portfolio have increased, particularly for midcap funds. We intend to rebalance this exposure away from midcaps into large caps, which currently exhibit more favourable scores.

Our selection of equity active funds has started to outperform their respective benchmarks, contributing to the portfolios’ outperformance. In the last month, we made one major change by switching from Powergrid to Indigrid INVIT due to the latter’s stronger acquisition track record. Additionally, as we anticipate rate cuts in the next few quarters, our exposure to INVITs and REITs should help generate some capital gains.

The portfolios have performed broadly in line with expectations. Here is a performance update of our three multi-asset portfolio strategies:

Performance is calculated using Time Weighted Returns, net of fees and expenses. Returns over one year are compounded annually; returns for less than one year are absolute. Please note that SEBI does not verify the performance information provided above. Please note that past performance is not a guarantee of future performance.

NSE Multi Asset Index 2 composition is 50% Nifty 500, 20% Nifty 50 Arbitrage, 20% Nifty Medium Duration Debt Index, 10% Nifty REITs and InVITs