Jul 5, 2023

• Fed pauses in June but signals further rate hikes.

• A diversified global equities portfolio should form the core of international allocations.

• Emerging markets’ valuations looking attractive relative to developed markets.

• India's inflation and growth outlook appears favourable in the current global economic context.

• Our asset allocation views- neutral equities, overweight gold- remain unchanged.

Back to Basics

We saw a stark contrast between the prevailing narrative that was generally pessimistic, and the surprising

optimism displayed by global equity markets in the first half of the year. Investors must now reconcile two

conflicting views about the US economy, with some predicting a soft landing and others a severe recession.

Given this uncertainty, it is best to stick to the basics by adopting a balanced portfolio strategy and seizing

tactical opportunities.

Source: Bloomberg, Sanctum Wealth

All data are in local currency and are price returns.

Global Macro Update

As anticipated, the US Federal Reserve halted its rate hike cycle during the June monetary policy meeting.

However, it did signal its intention to hike rates by another 50bps by the end of the year. The Fed also

revised its projection for GDP and inflation higher and unemployment projections lower, thereby

acknowledging the stronger-than-expected economic data. As reflected by Fed Funds futures, the market is

pricing in more than 85% probability of another rate hike in the July meeting followed by a long pause. and

now expects rate cuts only by the middle of next year.

Fed’s latest projections vs. March estimates

Source: Bloomberg, Sanctum Wealth

Old estimates as per March policy, new estimates as per June policy

The US economy has started exhibiting signs of a slowdown, although not as quickly as the Fed might have expected. In June 2023, the US manufacturing PMI dropped to 46.3, down from 48.4 in May 2023 and Investment Strategy 04 July 2023 below the projected 48.5. Similarly, the US services PMI declined to 54.1 in June from 54.9 in May but remained decisively in the expansion zone (as a reading above 50 signifies expansion). Other high- frequency indicators indicate that while the economy has weakened, it hasn’t collapsed.

Similarly, inflation shows signs of moderation, although core inflation remains stubborn. The base effect should help with further moderation in the upcoming months. However, non-farm payrolls are near the upper end of the pre-COVID range, indicating a strong labour market, which concerns the Fed.

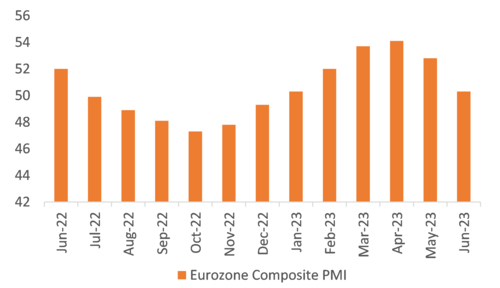

The Eurozone is displaying greater signs of a slowdown, as evidenced by the latest data. In June 2023, PMIs across the board missed expectations. Composite PMI declined to 50.3 from 52.8 in May, manufacturing PMI fell to 44.1 from 46.4, and services PMI also weakened to 52.4 from 55.1 but remained in the expansionary zone. Additionally, inflation in the Eurozone has finally started to moderate, but core inflation, excluding energy and food, remains persistently high. Furthermore, the labour market in Eurozone also remains tight. Unlike the Fed, the European Central Bank (ECB) raised rates by another 25bps in June policy and signaled further rate hikes.

Eurozone composite PMI pointing to signs of slowdown

Source: Bloomberg, Sanctum Wealth

Unlike the rest of Europe, Brexit-led structural inflation in the UK shows no signs of a slowdown, with headline inflation at 8.7% and core inflation at 7.1%. The Bank of England has responded by increasing rates by 50bps to 4%. The market expects rates to peak at around 6.25% by the end of 2023.

At the start of the year, we had highlighted that the new leadership at the Bank of Japan (BoJ) could look to change course from its current ultra-loose monetary policy. However, Governor Ueda has consistently emphasised that inflation will stabilise soon. Given elevated inflation and recent wage hikes, the pressure on BoJ to tweak or abandon its Yield Curve Control is mounting. Such a change in approach could potentially strengthen the Japanese Yen against the US Dollar in the coming months.

The Chinese economy is also showing signs of slower growth after a sharp rebound post the reopening. However, unlike other countries, China is not facing inflation issues. This allows the authorities to offer policy support to bolster the Chinese economy. The People's Bank of China (PBoC) lowered interest rates slightly but did not provide the anticipated boost the market hoped for. As a result, all eyes are now on the upcoming July Politburo meeting, where analysts anticipate a more substantial stimulus to support the economy.

Global Markets Outlook

A balanced portfolio should include a well-diversified global equities portfolio at the core of its international

allocation. Such a portfolio should diversify beyond US equities and include other developed and emerging

markets. This is because while US equities constitute close to two-thirds of the MSCI All Country World

Index (MSCI ACWI), historical patterns suggest that when a sector or country becomes disproportionately

weighted, there tends to be a normalisation over time. For instance, Japanese equities previously

accounted for 44% of the global index but now represent less than 8%.

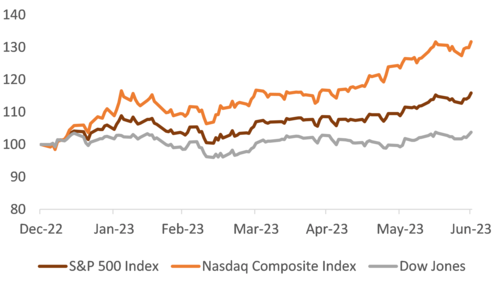

Although it is difficult to foretell whether US equities will follow the same trajectory, it may be prudent to diversify away from the US. Even from a tactical perspective, there are potential headwinds for US equities. The recent rally has been driven primarily by a few mega-cap stocks in the technology sector. Excluding these stocks, the overall performance of US equities year-to-date has been relatively subdued. The Dow Jones 30, which represents more traditional industries, has only returned 3.5% year-to-date, whereas the tech-heavy Nasdaq has seen a substantial return of 30.8%.

US equities driven primarily by technology sector

Source: Bloomberg, Sanctum Wealth

New sector leadership would need to emerge for the rally in US equities to persist. Furthermore, US equities valuations are expensive compared to the rest of the world, and the lag effects of one of the steepest rate hikes in US history are yet to be fully felt on the economy.

While valuations in Europe are much better as they trade at a significant discount, hawkish ECB policies could hurt economic growth and affect corporate earnings. On the other hand, improved corporate governance and reasonable valuations support Japanese equities. Although a potential strengthening of the Japanese Yen (JPY) may negatively impact corporate earnings due to Japan's reliance on exports, this is like to be offset by the investment gains from JPY appreciation against the US Dollar.

Emerging markets, particularly Asia-ex-Japan, also offer attractive valuations relative to developed markets. EM equities have underperformed developed market equities over the last decade primarily due to the outperformance of US equities. However, such periods of underperformance followed by a reversal are not unprecedented. Factors such as lower debt servicing costs, ample liquidity, and dollar strength against emerging market currencies have supported developed markets over the last decade but are expected to reverse.

Source: Bloomberg, Sanctum Wealth

China is a key component of EM. Chinese equities have corrected in the first half of 2023, resulting in more appealing valuations. The decline can be attributed to slowdown following the pandemic recovery and geopolitical tensions between the US and China. Market participants may require stimulative policy measures for Chinese equities to bounce back.

Indian Macro Update

Amidst the global slowdown, both India's high and low-frequency indicators show resilience. Industrial

activity, particularly in construction, remains strong, as reflected in robust manufacturing PMI number.

Consumer sentiment is reaching new highs, and auto sales remain solid, except for a slight moderation in

passenger vehicle sales due to a high base. The service sector also demonstrates strength, as seen in

services PMI, credit to services, air passenger traffic, and e-toll collections. GST collections continue to

clock more than INR 1.4 lakh crores a month.

While there are concerns about excessive monetary tightening globally, India has been performing well in this aspect. There has been a notable slowdown in inflation, driven by easing food and core inflation. Accordingly, the RBI kept rates unchanged in its recent policies, and may remain on hold for some time.

India's major concern, crude oil prices have remained favourable despite production cuts by OPEC+. Expectations of muted global demand amid slowing economic growth has offset supply cuts. Additionally, the recent moderation in the current account deficit suggests external headwinds have eased. The RBI has also used recent dollar weakness to rebuild FX reserves.

Overall, India's inflation and growth outlook appears favourable in the current global economic context.

India Market Update

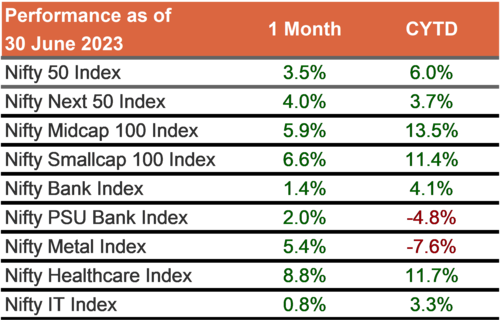

Indian equities rallied last month with the broader market outperforming the Nifty 50. After underperforming

in the first quarter of 2023, the broader market has rebounded sharply and now outperforms the Nifty 50

even on a year-to-date basis. The healthcare sector has emerged as the biggest outperformer, while

financial services have taken a back seat. The IT sector remains a laggard.

Source: Bloomberg, Sanctum Wealth

The above returns are total returns

Equity Outlook

Indian corporate earnings growth has surpassed most global peers. While most markets have witnessed

EPS contraction, India has delivered strong double-digit earnings growth over the last year. The outlook for

earnings also remains strong. Revenue growth is likely to be robust supported by still-strong urban

consumption demand and signs of recovery in rural demand. Further easing input prices should lead to

margin expansion.

FII flows have turned positive year-to-date but remain below historical levels. With India’s relative macro strength, better earnings prospects, and a weakening dollar, India could get higher inflows from foreign investors going forward.

While valuations at an aggregate level are not cheap, certain sectors are trading at or below pre-COVID levels, presenting opportunities for active managers to generate alpha.

Given the uncertain global environment and limited margin of safety that valuations provide, we maintain a neutral stance on equities, advising investors to buy on dips and gradually allocate fresh equity as part of a balanced portfolio approach.

Debt Outlook

In its June monetary policy decision, the Monetary Policy Committee (MPC) kept rates unchanged, as

widely anticipated by the market. However, some perceived the decision to keep the stance unchanged at

"withdrawal of accommodation" as somewhat hawkish. Consequently, bond yields have increased by over

14 bps, reaching 7.11% currently. It is important to note that bond yields had declined from 7.46% in March

2023 to recent lows of 6.97%, as the market celebrated the end of the rate hike cycle.

10 Year government bond yields have declined as RBI ends its rate hike cycle

Source: Bloomberg, Sanctum Wealth

However, at 7.11% it would seem that the market has already started factoring in rate cuts. Despite the moderation in inflation, an actual rate cut might still be a few policy meetings away, as economic growth remains resilient. The RBI may seek signs of a slowdown before providing support through rate cuts. Hence, a further decline in bond yields may take some time.

Those looking to add further duration may use any spike in yields as entry points. As we had highlighted earlier, investors holding duration may experience some volatility in the interim but stand to benefit when rate cuts become more imminent. For investors who cannot tolerate the associated volatility, opting for shorter-duration papers could be more prudent. These shorter-term bonds offer attractive yields, particularly given the current flat yield curve.