May 23, 2016

Nifty 50 earnings and CNX 500 earnings have been affected by the woeful performance from PSU banks and Steel companies. Excluding these two industries, profits for the Nifty 50 and CNX 500 have been impressive in what was expected to be a dismal earnings season. We remain buyers of growth stocks selling at reasonable valuations.

We continue to like ultra-short and short term funds as short end rates can move lower over the next few months with the liquidity situation easing. For the medium term, we remain focused on moderate credit oriented accrual funds.

Earnings Update

Heading into Q4 FY16, consensus expectations were that investors were in for a dismal earnings season. While first look performance may look to be living up to dismal expectations, digging under the hood reveals a far more appealing performance.

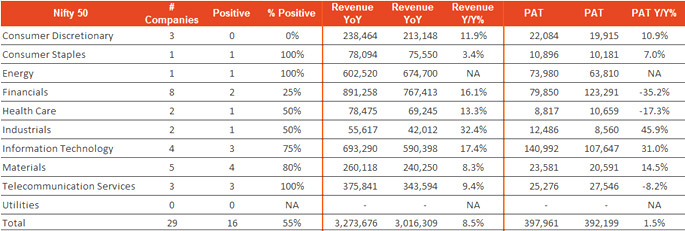

Of the 29 Nifty 50 companies that have reported to date, 55% have delivered positive earnings surprises for Q4 FY16. Further, sales growth is coming in at 8.5% while profits after taxes are up 1.5%. That looks woeful. However, adjusting for one company – Bank of Baroda – changes the picture completely. Bank of Baroda reported a 3,230 crore loss in the recent quarter. Incidentally, ICICI Bank also reported a 2,200 crore reduction in profits, but we’ve left that in the results.

Adjusting for Bank of Baroda, the numbers are transformed to a far better state – Nifty 50 sales are up 8.7% and PAT up 11.4%

With 29 Companies Reporting Earnings, Sales are Up 8.5% & Net Profits Up a Paltry 1.5%…

…But Adjusting for Bank of Baroda’s 3,200 Crore Write-off……Takes Revenues Up to 8.7% YoY and Net Profits Up a Respectable 11.4%

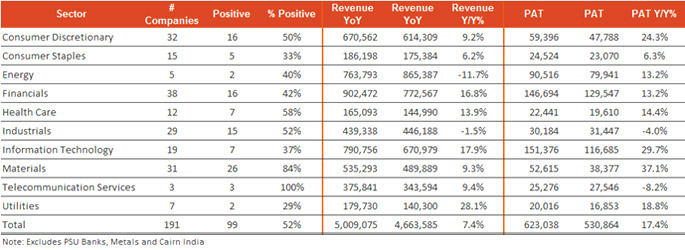

…Meanwhile CNX 500 Earnings Are Up a Healthy 17.4%… …But Only When Adjusted for PSU Banks & Steel Stocks …Suggesting the Wider Market Is Doing Just Fine

It’s evident from the earnings reports so far that the general market is doing well enough, and earnings are growing across Consumer Discretionary, Financials ex PSU, Health Care, IT, Materials and Utilities.

The government’s efforts in addressing PSU debt and ring fencing it will take time and efforts to firewall the sector will succeed. Moreover, the government remains committed and the full faith and credit of the Indian government stands behind the sector. Further, we’d point out that 89 per cent of 952 long term corporate debt securities worth over Rs 12.8 lakh crores were rated as safe for investment in 2015-16, a record high for such issues.

One of the undesirable effects of PSU bank woes is that bank credit has been slow on the uptake. It’s clear that capital is available for concerns that deserve it. Retail credit is buoyant and corporate credit is available to credit worthy institutions.

Valuations remain high for the market. Out performance will accrue to investors that buy right, allocate tactically and are able to manage volatility. We remain buyers of Equities at fair valuations. Recent quarterly performance reaffirms our view that a growth stock portfolio will deliver returns far in excess of other major asset classes.

Technical

The Nifty Index closed at 7750 level down by 0.83% for the week after another failed attempt at 7900. Immediate support is seen at 7700-7680 levels; breaking below this level, market can see decline towards 7545 levels which is the 38.2% retracement of the whole rise seen from low of 6825 in Feb’16 to high of 7992 in Apr’16.

On the upside 7900 levels will be the resistance for the market this week with significant amount of open interest addition in 7900 strike last week which will cap any gains. From a larger perspective, only if Nifty manages to sustain above 8000 levels on closing basis, it will provide positive trigger. Also, considering the rise that Nifty has shown in last couple of months, no major support levels have been broken on the downside and the Nifty continues to trade in a sideways range. Overall market is seen in a range of 7900-7600 levels.

Bonds

Bonds fell this week as a regular G-Sec auction weighed on secondary market demand, while fears of an interest rate hike in the U.S. continued to affect risk sentiment. The rupee fell for the seventh consecutive session, dropping to an over 11-week low against the dollar. The rupee ended at 67.44 to a dollar.

Underlying appetite for bonds has been hit by the recent higher than expected print of inflation, moderate supply and expectations of prolonged status quo on interest rates. In the coming week, the call money rate is likely to remain above the repo rate amid outflows on account of multiple debt auctions. The RBI is scheduled to auction bonds and T-bills worth Rs. 150 billion each and state development loans worth around Rs. 100 billion next week.

We continue to like ultra-short and short term funds as short end rates can move lower over the next few months with the liquidity situation easing.

For the medium term, we remain focused on moderate credit oriented accrual funds.Global

Key global events that will drive markets in coming days are the Fed’s adamant stance on raising rates in June, the Brexit vote in June and the continued increase in Crude Oil prices.

The market is loath to have liquidity withdrawn from the system and the best way to ensure that will be lower equity prices. So we wouldn’t be surprised to see volatility in coming weeks.

On Brexit, we think Britain would be worse off outside the EU and the markets are telling us a Remain vote is the likely vote, the odds on Leave are down to 25%. Of these, a sustained rise in the price of Crude is a key concern. Further out, a Trump victory could roil markets unless election rhetoric is toned down.

Crude Oil

Thanks to production disruptions in Nigeria, economic crisis in Venezuela, and an 8th straight weekly decline in the Baker Hughes rig count, it appears that supply and demand are starting to realign and balance is returning to global crude oil market dynamics. Sustained strong demand particularly from emerging markets has contributed from the demand side of the equation. Oil prices at or around $50 are probably a sweet spot for India but a continued rise, particularly post $60 would be a cause for concern.