Nov 30, 2023

India’s evolving housing landscape

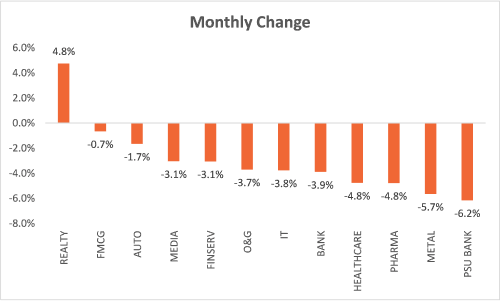

• From a sectoral perspective, Nifty Realty was the best-performing index and the only index to post gains, ending 5% up for the last month.

• In our view, this is not a short-term upswing but a structural play in the Indian housing market.

• Several factors have led to the upswing in the real estate cycle, which we believe is more structural and here to stay for coming years.

• We have been invested in real estate ancillary companies for the last two years in our Titans portfolio and continue to add other beneficiaries of theme depending on their fundamentals.

The headline indices witnessed a ~3% dip in October, while we saw a significant disparity in the behaviour of midcap and small-cap indices. The midcap index fell 4% in the month, whereas the small-cap index showed significant resilience, falling less than a percentage point. In the current month, the small-cap index has not only touched new highs but also has posted a smart 9% increase from its last month’s close, while the midcap and headline indices have only recovered their October month losses. This exuberance in small caps is not healthy, as such moves sometimes tend to mark short-term market tops.

From a sectoral perspective, Nifty Realty was the best-performing index and the only index to post gains, ending 5% up for the month. All other indices closed in red. The Realty index is also a star performer in the current month with gains of over 13%, surpassing its fifteen-year high in the current month.

Source: NSE, Sanctum Wealth Research

While the animal spirits in the Realty sector are visible now at the index level, we have been bullish on the sector for the past two years.

Our strategy in Titans portfolio is identifying a theme as the first step and going bottom up in the theme to identify winners. In 2020, we used the pick and shovel strategy to play the housing theme, focusing on companies benefiting from the housing boom. The thinking was simple – as more houses would be built, they would need more cement, paints, pipes, wires and finance. These were the spaces we identified for investing. The theme did well for us in the past two years, and we believe the sector may continue to do well in the coming years.

Here’s how some of the housing-related portfolio stocks in Sanctum Indian Titans have performed over the last three years.

Source: Sanctum Wealth Research

We have further doubled down on the sector recently by getting into direct beneficiaries of the realty play – the real estate developers. A closer look at the data indicates that the good days in the sector are far from over. The industry only reached its 2010 peak in terms of the number of units sold in 2022. In 2023, the top seven cities saw sales of over 1.2 lakh units in the second quarter alone, growing 30% YoY. Sales in the current festive season have also been robust, with the largest property market, MMR, seeing a 30% increase in property registrations compared to last year’s festive season.

Here is a chart showing housing supply and demand over the last decade.

Source: JLL India, Sanctum Wealth Research

Not only is the residential segment seeing robust growth but also the commercial segment, which is growing at 30% YoY in terms of area leased in Q2.

Several factors have led to such growth, and most don’t indicate exhaustion, which makes us believe that real estate growth can be a multi-year trend.

Major headwinds now over

Real Estate Regulatory Authority (RERA) has helped rebuild the homebuyer trust in the sector, which was a big stumbling block, given the nightmares honest homebuyers had to go through in the pre-RERA period.

The industry faced back-to-back jolts as RERA emerged, including GST implementation, demonetisation, a mini financial crisis of 2018, and COVID. During these jolts, the banks also went through the painful cleaning-up exercise emanating from the asset quality review, making lending difficult.

As all these issues are now behind us and the financial system is on a solid wicket, the path is set for the industry to grow.

Improved affordability

There has also been a massive improvement in real estate affordability compared to 2010. The annual nominal salary increases in India fell between nine to twelve percent, while the real estate pricing CAGR had been ~7%, making real estate affordable for salaried individuals.

Here is an indexed comparison of housing prices and salaries over the last decade.

Source: RBI, Sanctum Wealth Research

Furthermore, India’s mortgage penetration at 13% of GDP is lower than some comparable Asian economies and less than half of China’s and a fourth of the US, which not only shows the low housing leverage but also a tremendous scope of demand fulfilment through mortgage.

Improved quality of supply

RERA has also helped organise and consolidate the real estate industry as the cost of non-compliance has increased significantly for erring builders. Therefore, the supply quality has also improved significantly, leading to swift decision-making by buyers, improved turnover and lower after-sales issues.

Urbanization

At 36% urbanisation, India is 6% more urbanised than in 2010 on an increased population base, which bodes well for the sector as cities are the prime growth centres for real estate development. The development of new urban centres also bodes well for the sector as the emerging geographies have comparable earnings prospects but much more affordable housing prices.

The country has also seen significant improvement in infrastructure, including roads, railways and metros, which has opened new clusters for real estate development.

Currently, India is as urbanised as China was in the early 2000s when it started investing in infrastructure development in a big way (8% of GDP in 2002 to 24% in 2016). The country also reformed its housing sector, which acted as an inflection point for growth acceleration. Since then, China’s urbanisation rate has doubled, and resultingly, the real estate sector’s contribution to China’s growth has been consistently close to 35%.

From an economic output perspective, China’s GDP was close to $1.2 trillion in 2000, and it will grow to approximately $18 trillion in 2022, which is close to $16.8 trillion addition in 22 years. Cumulatively, Housing contributed close to a third of additional GDP output, which is $5.5 trillion addition from the sector alone in the last 22 years.

Source: World Bank Data, Sanctum Wealth Research

India has also accelerated its infrastructure spending recently. The budget allocation to infrastructure in FY24 (Rs. 10 lakh crore) is 3.3% of GDP, three times that in 2019. If these investments continue and economic growth remains robust, it would be natural for the real estate sector to outpace the GDP growth by a significant margin.

Though the debt-fuelled growth in China came with plenty of challenges, India’s real estate sector is still far from being overleveraged to be a major concern (average debt/equity of 0.6x). Instead, RERA’s implementation has made it difficult for developers in India to go the Evergrande way.

Rate action has not affected demand

Though rates have increased in recently, they have come up from a very low base not seen in several years. The current rates are more in the normal range, so the real estate demand hasn’t seen a dent despite the hike. Higher rates aren’t a concern for the sector unless significant macro changes warrant much higher rates.

Conclusion

We believe that the housing market has gone through a lengthy consolidation, and the industry has emerged stronger from the tumultuous decade. As most of the concerns marring the industry have been allayed, there is a significant scope for growth. We also believe that it’s not a short-term trend and is here to stay for years to come.

We continue to be bullish on the real estate ancillary businesses; however, there is a lack of valuation comfort in names that have run up significantly recently. This is why we have trimmed some of our investments in these names and are moving to other beneficiaries of the sector upswing that are valued reasonably.

Here is a glimpse of one-year forward valuations for these sectors.

Source: Sanctum Wealth Research

We believe that the valuation will catch up in reasonably valued sectors and, therefore, continue to evaluate new opportunities to benefit from the themes.

In Titans, the theme and the companies in the theme have been a major focus area for us. This is why we sometimes end up missing on some themes that won’t fit in our criterion. The same has been the case in the past few months, when the focus on quality has led to a short-term lag in the portfolio. However, we believe that our approach help attain less volatile portfolio returns in the long run.

On that note, here is the performance of our flagship strategies over different periods.

Portfolio Performance

The detailed performance can be viewed and compared with other PMS performances on this webpage.

Performance is calculated using Time Weighted Returns, net of fees and expenses. Returns over one year are compounded annually; returns for less than one year are absolute. Please note that SEBI does not verify the performance information provided above. Please note that past performance is not a guarantee of future performance.