Sep 3, 2019

“If you really want something in life you have to work for it. Now quiet! They’re about to announce the lottery numbers.” – Homer Simpson

Everyone knows everything today. There is an avalanche of data, opinion, news, blogs available on the net, much of the easily sourced is negative. Global media creates a veritable state of fear, because fear generates eyeballs. If it bleeds, it leads. If it’s fear, it sells. Yet, as we look back at the last twenty years, India has created massive wealth in equities. In the midst of the cacophony of biased, fake news, we attempt to provide meaningful and thoughtful interpretation of the markets. We start this week with a longer-term domestic perspective.

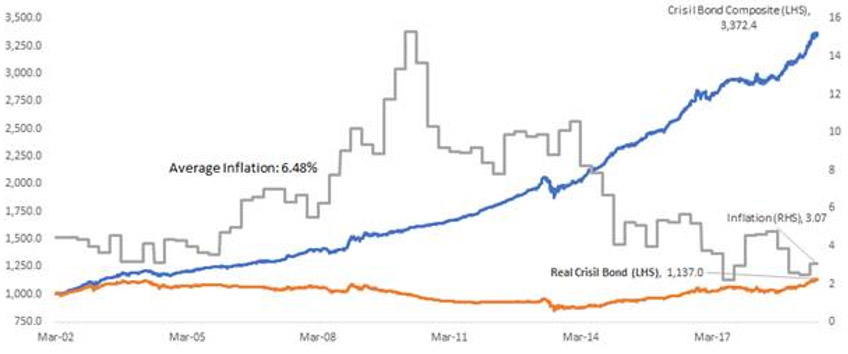

The Real Return of Bonds in India is 0.74% per year Since 2002

Bonds play a critical part in investor portfolios, usually from an income generation, diversification and volatility reduction perspective. Consider that INR 1000 invested in Mar 2002 in the Crisil Bond Composite Index has grown nominally to 3372 today, for a 7.2% CAGR. However, inflation adjusting the return – the real return – drops the growth to a palty INR 1137 or and the total real return to just 13.7% over 17.5 years. Clearly, investors pay a meaningful penalty for reliable income and reduced volatility.

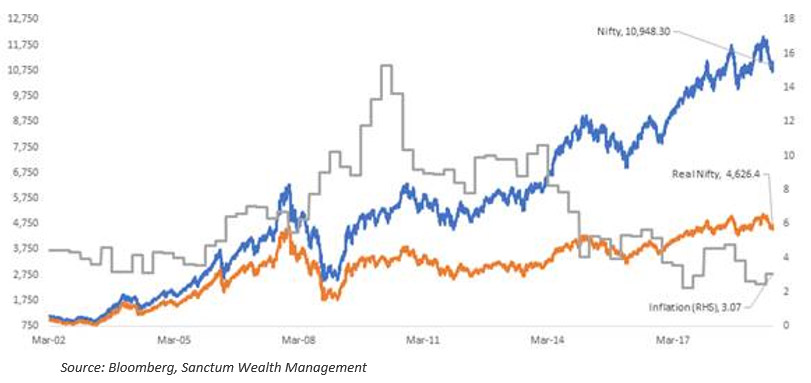

The Real Return of Equities in India is 9.18% per year Since 2002

Moving to equities, the Nifty 50 has delivered an impressive nominal return of 13.9% CAGR since 2002. However, the real return of 9.18% is even more impressive. (Note: Our choice of starting period is driven by data availability.) In other words, an investor would have doubled his purchasing power via equities every 8~ years.

Real Wealth – Equities Have Quadrupled Real Purchasing Power Over the Past 17 Years

That translates to a quadrupling of purchasing power – or wealth – over 17.5 years. Granted, it has not been easy being an equity investor, with painful corrections along the way. Volatility has only risen in the 2010s, but the falls have not been as severe. With equities, investors pay a penalty in accepting volatility for long-term wealth creation.

The Real Return of Bonds – Adjusted for CPI – is 0.74% Per Year Since 2002

The Real Return of Equities – Adjusted for CPI – is 9.18% Per Year Since 2002

The Economy – Structural Worries, Global Worries, Growth Worries…etc etc

This leads investors to a bit of a quandary today. While a case for equities is well accepted, the list of worries today is long indeed. The domestic economy just reported a significant deceleration at 5% growth, valuations are high, credit market is stressed, sentiment is pervasively dismal, there is talk of a structural slowdown, FIs are selling, and the consumer could be tapped out. Global issues are even more worrisome, with a worsening trade war, a manufacturing recession, a treasury bubble, negative interest rates as key concerns. We address these along the course of this commentary.

Fiscal Course Correction Underway

In the past fortnight, the government has course corrected, and announced a flurry of reforms, with more on the way. Recall the investor fraternity was fairly ebullient post the Modi victory, and it was the budget that killed animal spirits. Fiscal reform and monetary stimulus are necessary pre-requisites for a bottoming and revival in the economy. While one can debate the efficacy of some measures announced, in toto, we expect fiscal policy to course correct, and contribute positively with additional measures coming.

Services Remain in Good Shape, and Credit to Industry is Growing

India’s services sector looks well positioned. July’s reading was a 12 month high at 53.7. India’s growth momentum was slowed by demonetisation and GSP in the past five years, but the services sector remains well positioned.

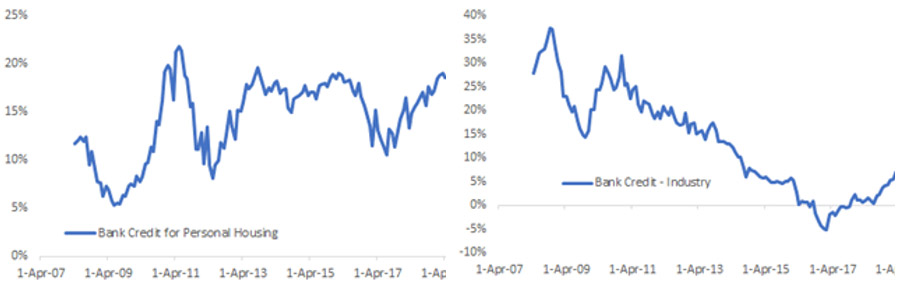

A Revival in Credit for Housing and Private Industry is Underway, Particularly MSMEs

We’ve Witnessed One of the Sharpest FI Sell-offs in Years…

…But Our Flow Indicator is Approaching Key Levels That Historically Correspond to Bottoms

Bank credit for personal housing has shown a strong pickup, as has bank credit to industry, and to medium sized enterprises in particular. We acknowledge, however, that this could be a pickup in slack from NBFCs no longer in the market.

FIs Have Sold Sharply and Look to be Closing In On a Bottom

FIs were strong buyers on the Modi victory and October credit crisis. They drove the Nifty 50 to 12,000 and have now taken back almost all of the buying. It appears that FI selling could be bottoming out soon.

The Domestic Consumer Balance Sheet is Healthy

While the domestic consumer has witnessed their debt rise from roughly 8% of GDP to 11.3% in recent quarters, and this could explain some of the pull back in spending we’re witnessing, India’s consumer debt to GDP remains puny at 11.3% versus 76.3% for the U.S. consumer.

Rate Cuts and Baby Steps to Transmission via RLLR Underway

We expect the RBI to cut rates by another 50 bps over coming meetings. SBI and Bank of Baroda launched repo linked lending rate (RLLR) based home loans last week. SBI will charge a spread of 2.25% above repo rate plus credit premium. Adjustable rates linked to a benchmark is the global standard. Should private sector banks not follow suit, they may find PSUs eating into their market share. Incidentally, a 2.25% spread above repo plus credit risk premium is a fat number, and the lending space is ripe for disruption. Transmission of lower rates remains the key to the strength of the recovery.

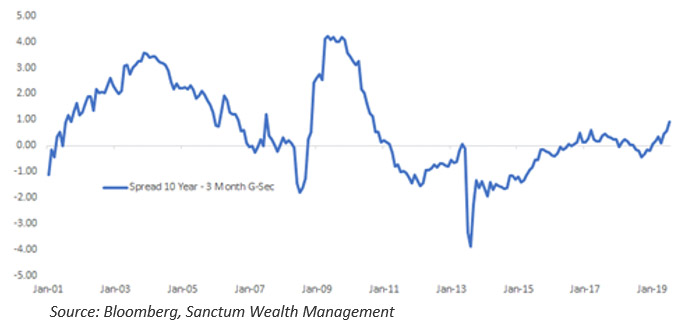

Yield Curve Steepening Has Traditionally Been a Precursor to Markets Performing Well

Yield Curve Steepening and Liquidity Surplus

The spread between the 10 year and 3 month g-sec finally moved decisively into positive territory, (see chart above) primarily as a result of the RBI’s rate cuts. The long end of the curve remains benign at 6.5%. There is also an abundance of liquidity in the system currently, with surplus liquidity parked in the reverse repo window of the Reserve Bank at ₹ 2.0 lakh crore.

Pathway to an Economic Recovery

The path to economic recovery will unfold as growth stabilizes. Increased liquidity, low inflation, lower rates, and lower commodity prices will have the usual positive effect on consumers, business and investors. Short term rates will continue to decline and the RBI will continue to ease. Transmission will happen slowly. Businesses will aggressively push for lower rates. Some businesses will recognize their profitability and top line improving, and will use cheap money to expand into new markets. Lower rates will lead to improving earnings, treasury profits, and rising disposable income.

As we write this, we are anecdotally witnessing some businesses doing precisely this. We would also point to a pickup in bank credit to industry, particularly medium enterprises, and a rising money supply. Domestic deposit and credit growth remain in double digits.

Global

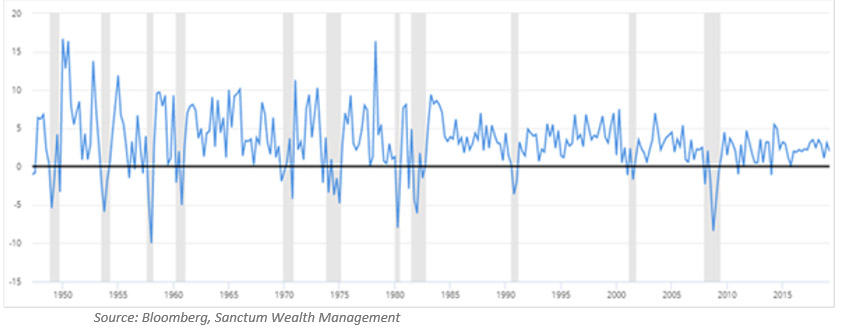

Implications of Lengthening U.S. Business Cycles

Fed Chairman Powell pointed out in Jackson Hole that the U.S. business cycles have gotten longer since 1982. This is true. However, this is also in large part due to the Fed’s “do whatever it takes to keep a recession away” philosophy since 1998. Since there’s been no high amplitude growth, and none of the markers of a typical business cycle top, it’s unlikely that the economic slowdown, if or when it occurs, is likely to be as severe either. There are however, unintended consequences, that will need to be monitored and impacts pondered, such as negative interest rates in 27% of the world’s bond market.

U.S. Business Expansions Have Gotten Longer Since Prior to 1982…

…This Expansion Remains a Late Stage Expansion

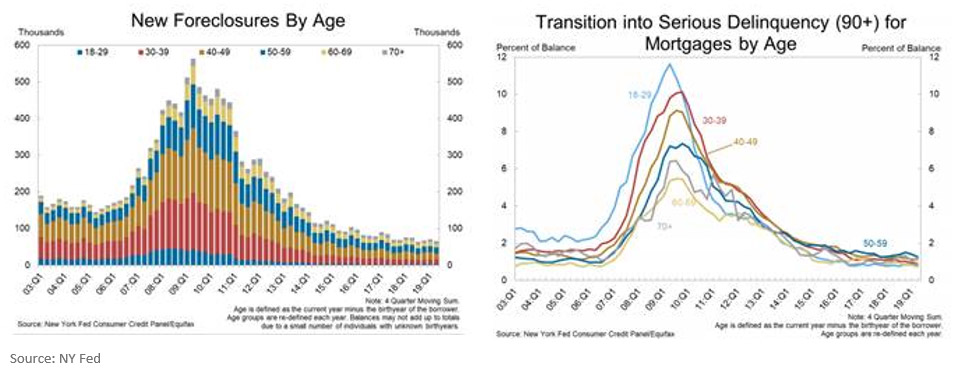

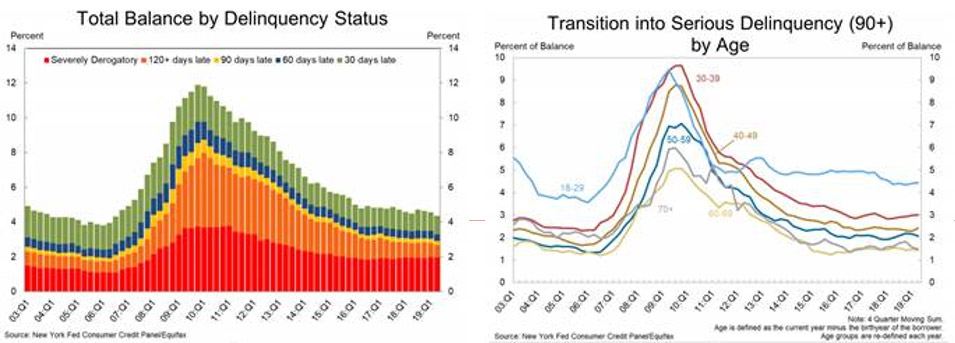

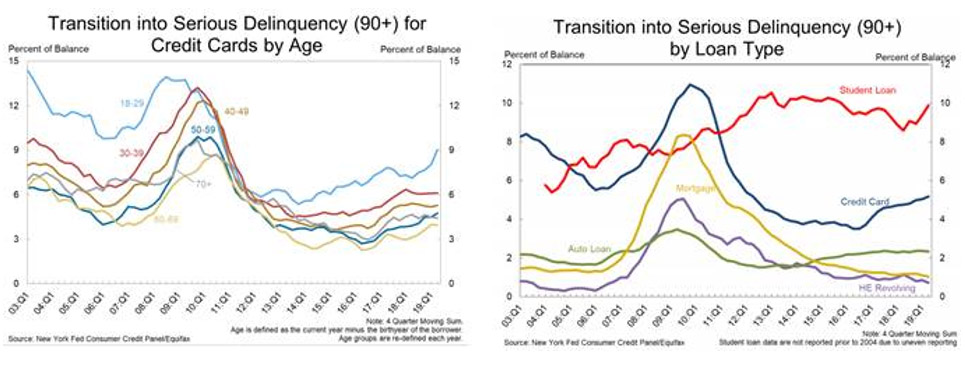

The U.S. Consumer in 2019 Is In Far Better Shape than 2007

…2007 Was a Consumer and Real Estate Crisis…

The U.S. Consumer Has Deleveraged Meaningfully Since 2009 and Is Much Healthier Today

We further make the case with charts below that the U.S. consumer has successfully deleveraged and is in reasonably healthy condition. Across metrics, we are unable to find significant signals of deterioration.

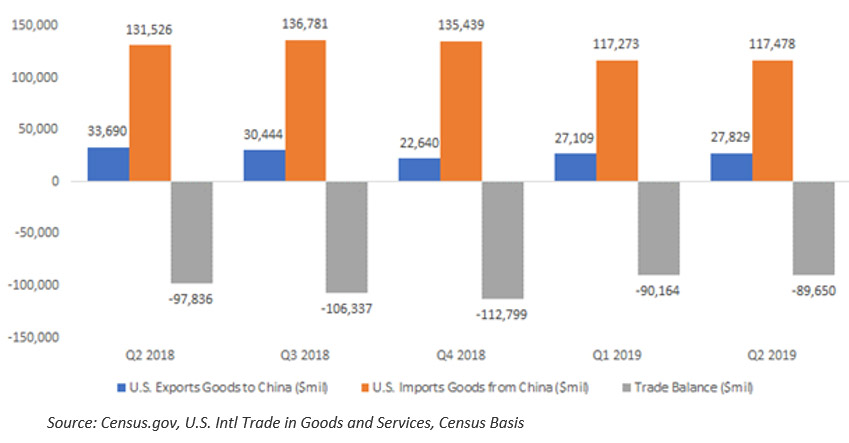

However, the U.S. Is Not Winning the Trade War with China…

While U.S. exports to China have declined 17.3% YoY, imports from China to the U.S. are down only 10.6%. On a dollar basis, however, Trump has fared better. Imports from China to the U.S. have declined by $14 billion, while exports from U.S. to China are down a smaller $5.8 billion. The trade balance has improved approximately 8 billion.

There are No Winners in a Trade War …

…While U.S. Goods Exports to China are Down $5.8 billion, or 17.3% YoY, …

… U.S. Goods Imports from China are Down $14 billion, or 10.6% YoY

Valuation in a Time of Low Rates

Let’s slay another holy cow. We ran a scatter plot on domestic valuations and inflation and found that a domestic inflation level of 2-3% equates to a trailing P/E roughly around 25. We’ve come across similar data in the U.S. which equates to an average CAPE (cyclically adjusted PE) of 20.9 for inflation levels around 2%, and a CAPE of 21.0 – 23.4 for interest rates less than 4%. High valuations are reasonably justified for a structurally low inflation and low interest rate environment. Still, investors would be wise to moderately temper their long term return expectations.

Outlook

Equities

The U.S. Remains in a Late Stage Expansion While India is Exiting a Slowdown

The preponderance of indicators today suggest that the U.S. is in a late cycle business expansion. The U.S. consumer is not stretched as he/she was in 2007 and has noticeably improved their balance sheet. The U.S. economy appears to be slowing but there isn’t enough to suggest a recession is imminent. Moreover, global fiscal stimulus is on the way.

Fiscal Policy Commitment is a Pre-Requisite for Recovery and Bold Measures Needed

India’s monetary policy has been at work since the beginning of the year, while the U.S. Fed has not even fully acknowledged a slowdown, and rightly so, based on the data. Fiscal policy commitment, working in tandem with monetary policy, with bold measures, and stimulus, is the balm that is necessary to ensure the economy, and sentiment, recovers in H2 FY20. .

Treasury Bubbles and Negative Interest Rates

There are unhealthy signs in global treasury and debt markets with negative yields and unnaturally low interest rates. Nearly 27% of the world’s bonds – $16 trillion – offer negative yield. The notion of earning a negative return is contrary to all prudent notions of finance. The yield curve remains an indicator in the background to keep a watch on.

A Losers Game

We’re not sure how this treasury bond and global negative yield scenario plays out. However, the history of this decade, and going back to 1998, is that fighting the central bankers is a loser’s game and a low probability of success strategy. That’s what we have witnessed time and again since 2009. Rather, Japan is one possible model. The Japanese have muddled along since 1990, for thirty years now, and they aren’t half as creative as the Fed and ECB.

JP Morgan Points to a Shift to Asia Longer Term

The longer term outcome remains fairly clear. Growth, as JP Morgan, pointed out this week, will shift to Asia and the U.S. dollar is seeing its global dominance come to an end. “In the coming decades we think the world economy will transition from the US and US dollar dominance toward a system where Asia wields greater power,” JP Morgan stated. Emerging markets such as India, Vietnam, Indonesia, Malaysia and Thailand are the place to be.

Despite Pessimism and FI Selling, the Market Has Demonstrated Resilience

Over the past 18 months, despite a plethora of worries, the stock market has demonstrated resilience. The market has doggedly defended 10,800 and SIP data is showing moderately rising flows again. We expect GDP growth to stabilize and then pickup, valuations are likely to remain elevated while inflation to remain low and rates headed lower. The consumer, business and investor will recover in coming months. Domestic capital is continuing to provide liquidity to markets. In time, sentiment will turn.

Winner Take All Phenomenon and Value Investing

In a study performed by Arizona State University, researchers looked at 62,000 global common stocks from 1990 to 2018, and ranked them on a compounded, total-return basis. That period includes bear and bull cycles. Just 1% of the world’s public companies accounted for all the market gains during the past three decades. Five companies — Apple Inc., Microsoft Corp., Amazon.Com Inc., Alphabet Inc. (Google) and Exxon Mobil Corp. — accounted for 8.3% of global net wealth creation.

Equally importantly, less than half of the stocks in the study had cumulative positive returns. A majority of stocks — 60.9% — were net wealth destroyers. This study clearly argues to the challenges value investors face in winner take all markets. Two, Amazon, Microsoft, Google have been expensive stocks their entire life cycles. How does one ensure these companies make it into your portfolio? Broad indexing is one strategy. A better strategy is a portfolio focused on premium quality growth in winner take all markets, if feasible, or alternatively, dominance.

Strategy

Our best case scenario then is an extension of the U.S. expansion alongside a recovery in Indian markets. The alternative playbook remains a market correction followed by the launch of QE.

Domestic markets are better positioned. With fiscal policy support arriving, investors should stay the course on equities. Portfolios constructed to deal with multiple outcomes rather than a specific view are preferable. Adding strategies such as capital protected strategies, long short, an appropriate allocation to Gold and Silver, selective global allocation, opportunistic hedging, and appropriate fixed income and duration exposure will all work to enhance portfolio risk return profiles.

As always, equity investments should be viewed as long term. Over a three year horizon, a well constructed portfolio will deliver attractive returns. For instance, investors in Olympians that entered in the fall of 2016 have earned 14-16% average CAGR returns, net of fees. The alternatives – bond, gold, cash, real estate – don’t come close.

Fixed Income

In the past 75 years, the S&P 500 has suffered 16 down years. In 15 of those 16 years, moderate duration treasuries delivered positive returns. Moderate duration via corporate and PSU bond funds makes sense. A small portion allocated to moderate duration via g-secs can also be considered as a portfolio hedge. Alternatively, an allocation to Gold will provide similar protection. The benefit with duration is the regular income component.

A diversified portfolio of AAA rated, highest quality, corporate bonds, banking and PSU bond funds, short, medium term bonds, moderate duration remains our preferred positioning.

Technical Outlook

The Nifty witnessed gains at the start of the week and saw some profit booking in later part of the week. The Nifty finally settled at 11,023 with a gain of 1.8% for the week. Broader market indices BSE Midcap and Smallcap were up 2% and 2.9% respectively for the week. The bounce back from low of 10,637 touched high of 11,142. The Nifty has resistance zone around 11,150-11,200 where recent highs, 200 day moving average and 38.2% Fibonacci retracement of the fall 12,103-10,637 are seen. But, on daily chart index is forming possible bullish inverted head and shoulders pattern and the neckline for same is seen at 11150 odd levels. Thus, 11,200 is the breakout levels which needs to be taken out for uptrend to continue initially towards 11,370 and then 11,450 levels. On downside support is 10,850-10,800 zone which needs to hold for market to breakout on upside. Below 10,800, index is likely to test 10,637-10,580 zone. In Nifty September monthly expiry options, maximum open interest for Put is at strike price 10,800 followed 11,000; while for Call it is at 11,700 followed by 11,200. Thus, Put-Call option distribution data is suggesting a range of 10,800 and 11,200 for now. India VIX closed at 16.28 down by 6.15% for the week. VIX is hovering in the region of 18-16 which is capping the market upside; it needs to move below 16 for sustainable up move in Nifty above 11,200. However, VIX moving above 18 will lead to fresh selling pressure in the market.