Nov 26, 2018

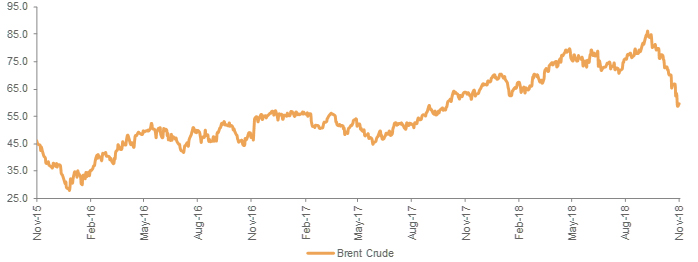

Crude oil prices have fallen dramatically, with Brent falling 31% from a high of $86.2 to $58.8 in the past few weeks. The dramatic drop in prices has been precipitated by rising inventories, expectations of dramatically rising U.S. production in 2019, coupled with cooling global demand, leading to a supply demand mismatch. The volatility in prices is being exacerbated by speculators and hedge funds.

Setting aside fears of slowing global growth for a moment, this is much needed relief for the Indian economy from a fiscal, consumption, interest rate, inflation and operating profitability viewpoint. Secondly, $80 can now be established as an upper bound on global oil prices, as demand destruction occurred quickly at levels above $80 in the recent past.

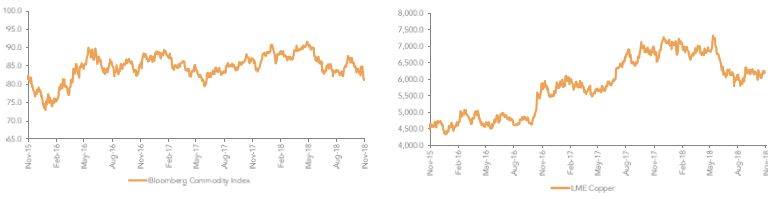

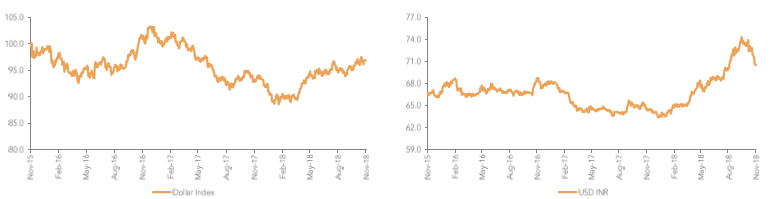

Inter-market linkages have reverberated through global asset classes. Commodity prices have rolled over, as has Copper, well known for it’s indication of global economic prospects. The deflationary impact of falling Brent has impacted Gold, which has fallen back to lower levels of the trading range. Finally, the Rupee appears to have put in a medium-term bottom, currently heading for $70 after hitting a high of 74.46 recently. We can also expect downward pressure on domestic interest rates and inflation, rising disposable incomes, and pressure shifting from commodity importing nations.

Brent Is At a 7 Month Low

The Bloomberg Commodity Price Index Is at a 1 Year Low & Copper Prices Have Peaked As Well…

The USD Has Been Stronger Since April on a Safe Haven Trade, While the Rupee Appears to Have Made a Bottom in Late September

Gold Remains Range Bound and Lower Since April

A Strong Show on Earnings

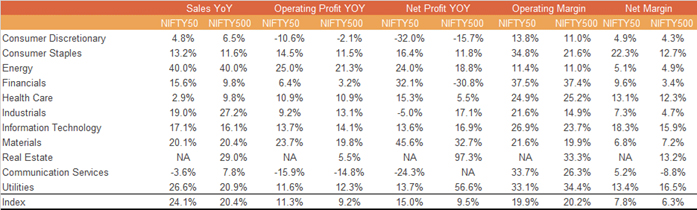

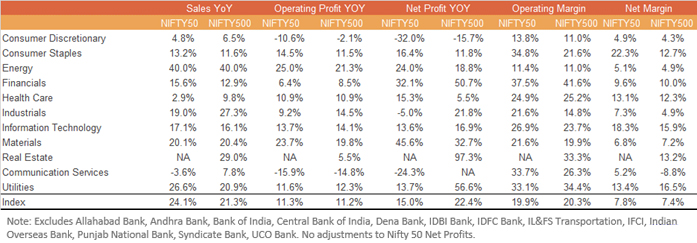

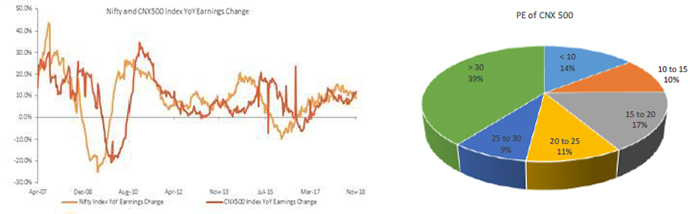

With earnings season mostly complete, the Nifty 50 and CNX 500 companies have posted impressive performances, with profits up 15.0% and 22.4% respectively, (no adjustments for the Nifty 50, excluding losses from PSU banks for the CNX 500). Sectorally, the performance has been led by Financials (ex PSU), Industrials, Energy, Materials and Utilities.

Nifty 50 Sales Were Up 24.1% While Profits are Up 15%….

Adjusting for PSU Losses, Nifty 50 Profits are Up 15.0%…

While CNX 500 Profits are Up 22.4%

Nifty 50 Sales Were Up 24.1% While Profits are Up 15%….

Some Progress on Valuations

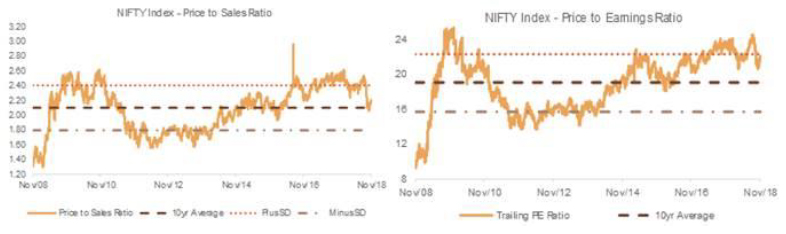

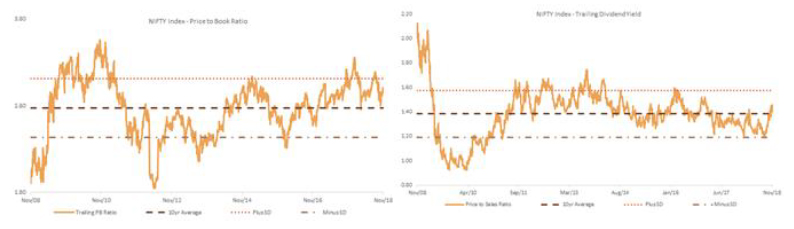

The Price to Sales ratio on the Nifty 50 is back its 10-year average, suggesting top line valuations are at reasonable levels. Price to Book and Price to Dividend Yield are also approaching valuations near the middle of their historical averages. However, the Nifty P/E ratio remains elevated and the relative value also suggests that equities remain expensive relative to fixed income. However, it should be noted PE valuations at the index level have been impacted by large losses amongst select constituents.

The Price to Sales Ratio is Back to Average Levels…

Price to Book and Price to Dividend Yield are Approaching Average Levels of Valuation…

But the Market at the Index Level Remains Expensive on a P/E Basis…

…. And Equities Remain Expensive Relative to Bonds

Equities

Taking an objective view of the macro situation, inflation is low, interest rates are likely headed lower, the RBI is likely on hold in terms of a rate hike, earnings are coming through, crude oil prices are ~30% lower, credit growth is healthy, the economy is the fastest growing large economy in the world and our demographics are strong. Globally, the U.S. and China appear to be interested in reaching a trade accord and the Fed, arguably is close to blinking, and pulling back on its rate hike timeline. So, many key factors are aligned positively for India.

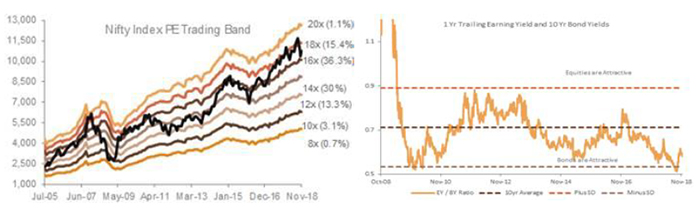

As we look ahead to 2019, elections loom as a key uncertainty. An adverse result poses shorter term risks, but longer term, fundamentals will assert themselves. While earnings growth is coming through, valuations remain a headwind that needs to be worked through. Much of the market has corrected to reasonable valuations, but parts of the market remain expensive.

Separately, FI inflows are starting to slowly make their way into the market. The domestic equity investor continues steadfast, providing strong support. Risks remain on NBFCs funding rollovers and cost of capital, but the RBI and government are keenly aware of the situation. The government will continue to need to manage PSU bad loans.

Looking ahead, we believe demographics, consumption, connectivity to rural and third tier, structural reforms, strong domestic inflows, good earnings momentum and lower crude prices provide support for the market. Meetings of the G-20, OPEC and Russia, and China U.S. trade talks are likely to be key triggers for markets globally, while elections will be the focus domestically alongside NBFC credit rollovers.

With expected lower inflation, lower rates, higher margins, the market will continue to work through concerns. The macro environment is looking more favourable as we head into 2019 than it has in a while.

Earnings Growth is on a Steady Upward Trend…

…And More Than 50% of the CNX 500 Has a P/E Under 25

Fixed Income

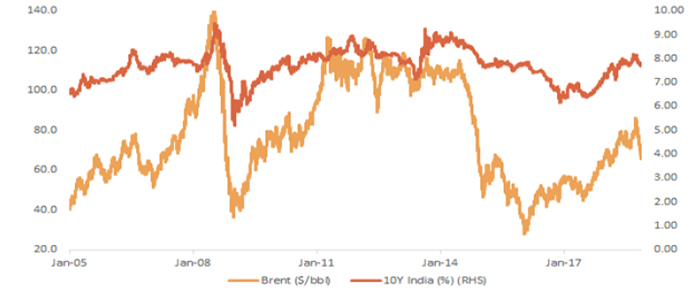

Brent has a clear leading relationship with crude, understandably so, leading the 10-year g-sec lower in 2008, 2012 and 2014, and leading g-secs higher in 2007, 2009 and 2017. The precipitous drop in crude, should it stabilize at these levels, suggests the direction of g-secs in coming months will be lower.

Brent Has a Clear Leading Correlation with 10 Year G-Secs

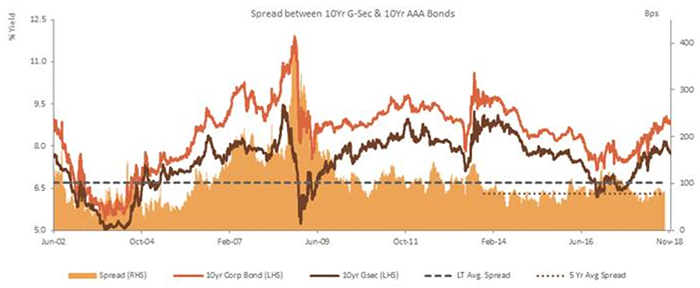

The fall in crude prices is also likely to exert a positive impact on inflation. While the G-Sec 10-year yield has declined, AAA bond yields have stayed elevated possibly reflecting heightened concerns about credit markets. However, AAA corporates generally follow g-secs with a lag, and we expect the same to play out over coming weeks.

AAA Corporate Yields Have Not Followed G-Secs Lower Lately, But Should Do So with a Lag

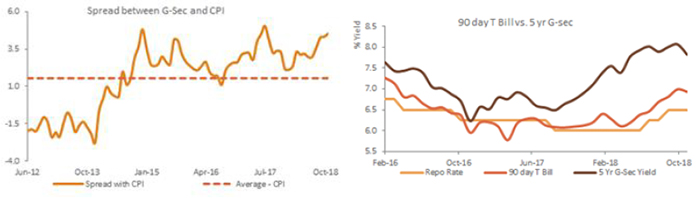

The Spread Between G-Secs and CPI Is At 5 Year Highs…

While Short Term T-Bill Rates Remain Stable

The market has a unique way of getting to where it needs to go, while confounding the consensus along the way. At the beginning of the year, the consensus expected crude at $55-60, and that’s where we’re at today. Whether production rises dramatically next year or not is anybody’s guess. Should oil prices sustain at current levels, and the NBFC crisis abate, there’s a case to be made for lower interest rates, particularly considering the spread between g-secs and CPI is close to 5 year highs and a decline in corporate bond yields could be expected. With a big week for rollovers, smooth credit functioning would be a positive for credit risk funds. Fresh money allocations to corporate bond funds, and credit risk funds with high quality paper and moderate duration, would be our primary preferences, alongside structured products with Nifty upside.

Technical Strategy

After three week of consecutive gains, closed in negative for the truncated gone by. The Nifty closed at 10527 down by 1.46% for the week. During the week index touched high of 10775 and come of the highs. Here 200 day moving average which comes around 10750 levels and the 24th October falling gap area of 10755-10845 are acting as resistance for the market. Now immediate support level for index is seen at 10450 levels, breaking below which further decline towards 10200 levels can be seen in the market. On the upside Nifty needs to clear 10755-10845 resistance zone for sustainable uptrend in the market. In Nifty options, maximum open interest for Puts is seen at 10000 followed by 9800, while for Calls it is at 11000 followed by 10700. Good amount of Put unwinding was seen in 10600 and Call writing in 10600 and 10700 suggesting upside to be capped and pressure on downside. India VIX measure at 19.16 continues to remain at elevated levels which is likely to cap upside in the market. It needs to decline below 17 levels to support up move.