Jun 27, 2017

“The idea that the future is unpredictable is undermined every day with the ease with which the past is explained” – Daniel Kahneman, Thinking Fast and Slow

While scepticism reigns on the prognosis of the equity bull market, there’s no doubt about the level of fear. Welcome to the bull market in fear. We’d postulate that this fear is driven by two key factors: one, the embedded painful experience of sell-offs we’ve experienced each of the past two years, and heightened valuations. We make the case this week – backed by data – that top line growth is coming through, the economy is showing signs of recovery, GST is a likely game changer, and we remain in the middle innings of the business cycle.

Equities

Sales & Earnings Have Come Through

First, we’ll clarify what data we look at. Our PAT number is prior to one-time adjustments and extraordinary items, to get closer to like to like comparisons on profits. We look at the CNX 500 to get a broader view of the market.

Sales Are Up 11.0%, Profits After Tax Are Up 20.8%…When Adjusted for Just 2 Companies

Consolidated Profits after Tax are up 20.8% in Q1 CY17 if we adjust for just two companies. We adjust for Vedanta because of a very large deferred tax credit last year and we adjust for Power Finance Corp for a significantly large loss.

Adjusting for 2 companies (Vedanta and Power Finance Corp)…

…Sales Growth Is Up 11.0% and Net Profits are Up an Impressive 20.8% YoY

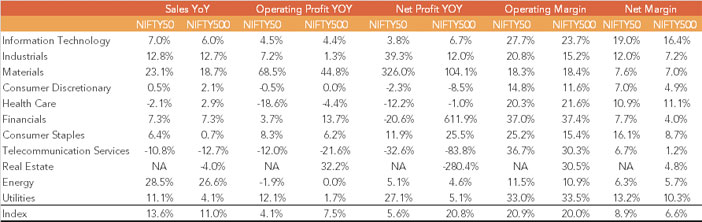

CNX 500 Performance Q1 CY17

A Respectable 43%~ of CNX 500 Companies Have Delivered Sales Above 10% YoY…

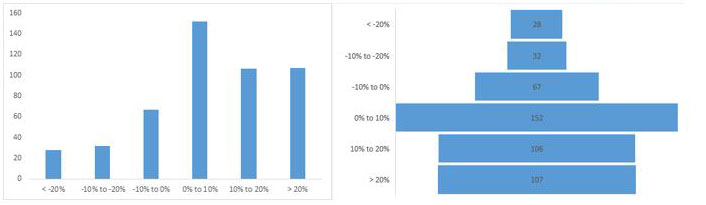

…While 47% Have Delivered Operating Earnings in Excess of 10% YoY

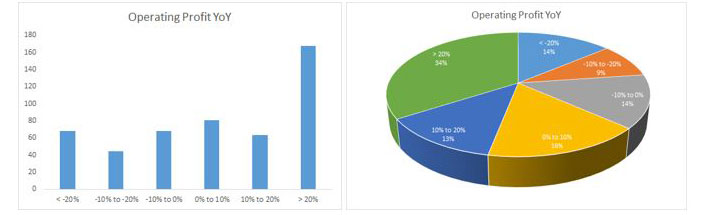

Finally, 31% of CNX 500 Companies Reported Healthy PAT In Excess of 20% YoY…

…While 47% Reported Negative Earnings Growth…

…Suggesting a Bifurcating Economy of Haves and Have Nots

Sales Numbers Have Impressed For the First Time In Several Quarters

On sales, as the charts show, the majority of companies are delivering positive top line growth. Around 43% are delivering at least 10% plus growth. In a 3%~ inflation world, that’s a meaningful top line number. Further, the distribution demonstrates that skew is weighted towards 10-20% growth.

Given Q1 CY17 was the first quarter out of demonetisation, there was certainly a fair bit of shock in the system and this is respectable performance under the circumstances.

One third – or 168 companies – have delivered at least 20% operating earnings growth, which is impressive. Almost half – 47% to be precise – have delivered operating earnings in excess of 10%, again impressive relative to GDP growth and inflation. We’d have looked for numbers to be a bit better spread; however, we take this in the context of demonetisation and a challenging operating environment.

Profit After Taxes – 31% of Companies Grew Above 20% YoY, While 47% Contracted

The PAT performance distribution gives a clear indication of the state of the market and a story of haves and have nots. One third of the market continues to thrive. 40% of companies are delivering acceptable growth above 10%. However, the other half is struggling. 47% of companies have reported negative earnings, or negative earnings growth. This demonstrates the narrow nature of the recovery and reinforces the view that our economy is essentially supported by one key leg – consumption.

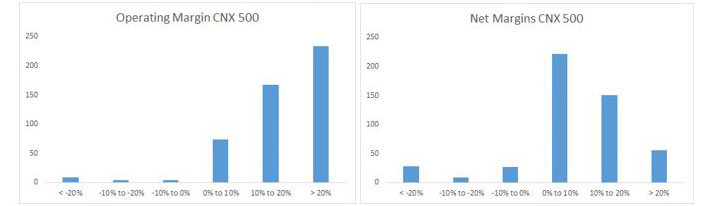

Operating & Net Profit Margins Are Healthy

The bulk of companies in the CNX 500 delivered healthy operating and net profit margins. Profitability is not an issue. Very few companies had negative margins. However, while a majority of companies had healthy operating margins, net margins demonstrated a relatively weaker trend, indicating that a cross section of the market is weighed down by high interest burdens.

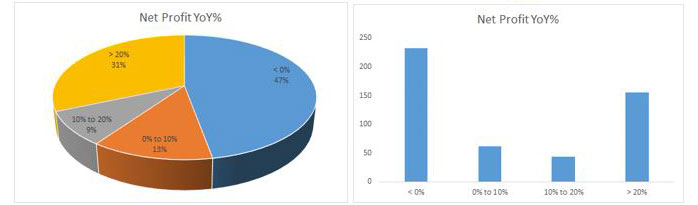

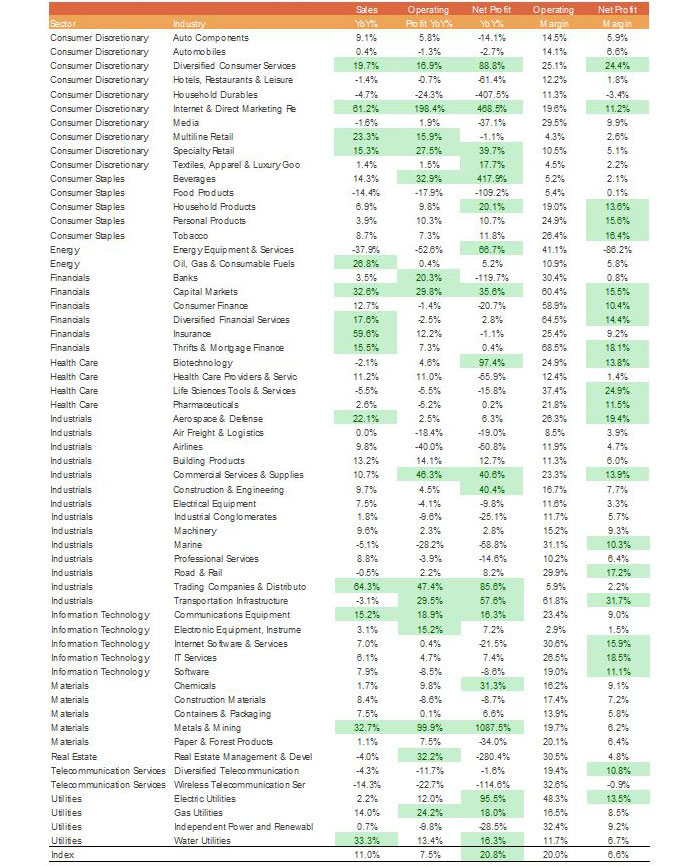

We refrain from drawing too many conclusions on sectoral data, preferring to drill down to Industry, except to note that Materials, Industrials, and Energy have delivered strong top line results.

Operating & Net Margins for the CNX 500 Are Healthy…

GST – Transformative and a Positive for Markets

There Will Be Mayhem In the Short Term

It’s clear the nation is not ready for GST and confusion is likely to reign. July is likely to be yet another painful month for small businesses. We also think GST is likely to lead a large number of business models folding.

A Dramatic Expansion of the Tax Base

GST is causing large businesses to stop working with vendors that don’t file taxes. Thousands of small businesses will be forced to come into the fold, wittingly or unwittingly. It’s safe to assume that government tax collections are likely to rise. This frees up money for reforms and investment, and a strengthening of the government’s finances.

A Dramatic Shrinkage of the Underground Economy

In an economy where more than 90% of workers are employed informally, GST will force companies to be enrolled in the tax system and prove they paid taxes to claim a credit against their costs. Companies will need to comply and the black economy will shrink. Many in the unorganized sector will need to transform their business models.

Increased Productivity, Decreased Logistics Costs, Faster Time to Transport, Improved Working Capital

Logistics companies spend over half their time stuck at tolls and check points. Many companies choose to have a multi nodal network concentrated within states, rather than a hub and spoke model which most international companies employ. With GST, logistics efficiency will increase as time spent at check points will halve. Companies will be able to move goods faster and more reliably.

Lower Inflation and Improved Corporate Performance

The move to replace more than a dozen levies with a new goods and services tax will reduce bureaucracy and bribes at state borders, free up inter-state trade and lead to lower cost of goods sold.

Tax Avoidance Business Models Will Fail Going Forward

Businesses based on tax avoidance models will be at significant risk of survival. Any business that is looking to stay outside the tax net will need to ensure every transaction it conducts is also with a business outside the tax net.

GST Likely to Benefit the Organized Sector, Government and Consumers

GST will effectively benefit the government and organized sector companies. Secondarily, we would hope – but not expect – some positive impact on prices but that remains to be seen. Savings should be passed on to consumers.

Industry Performance Led By Capital Markets, Metals & Mining, Specialty Retail

Macro Indicators Remain Mid Cycle

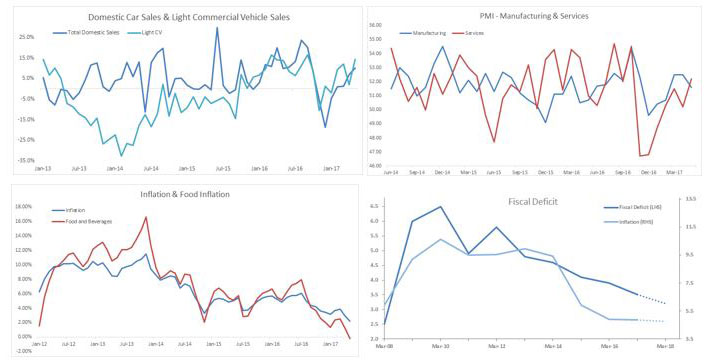

Consumer & Commercial Sectors Showing Some Buoyancy, Economy Remains in Mid Cycle Stage

Domestic automobile sales were accelerating last September, plummeted into demonetisation and are now showing signs of recovery. The same trend is visible in light commercial vehicle sales, which are a harbinger of a pickup in commercial activity. Inflation is at cycle lows, leaving a fair amount of headroom for the RBI to step in with a rate cut if growth falters. Manufacturing and Services PMIs are also showing similar signs of recovery from demonetisation blues.

Our assessment remains that we’re in the middle innings of the business cycle. Further, the RBI’s backed away from a hawkish view on inflation and we believe will step forward should the data worsen. However, that’s not our call. Post the short-term pain of GST, we continue to think disposable consumer incomes will rise and earnings leverage will kick in later this year.

Post Demonetisation, the Economy Is Recovering, But Nowhere Near Over Heating Or At a Cycle Top

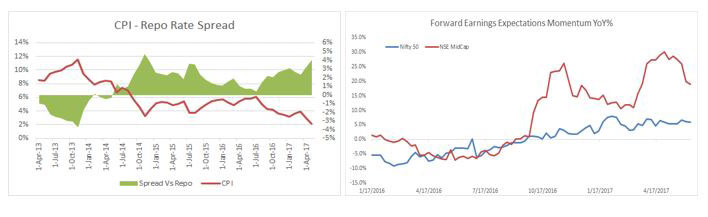

We Take Comfort Knowing The RBI Can Ease on Weakness…

…While Noting Strength in Earnings Revisions

Banking – Credit Growth Reverses & NPA Resolution Picks Up Pace

In other notable news, Banks’ credit growth grew at 6.02% in the fortnight ended 9-Jun-17, a welcome reversal from the 5.08% per cent in the earlier period. Bank deposit growth also picked up to 11.19% versus 10.9% in the prior period.

Global

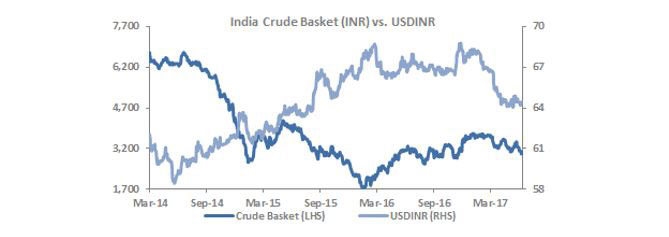

Disruption in the Crude Oil Industry a Boon for India

What’s happened in the energy space over the past two years is an example of the power of technological disruption. With solar now effectively competitive with coal in certain parts of the world, and shale competitive with crude, the dynamics of the energy industry are changing permanently. For an energy importer like India, this bodes well in terms of declining cost of raw materials and rising disposable incomes. The impact of disruption will be felt worst in the Middle East and the region will need to re-invent itself.

With solar continuing to follow Moore’s law, and shale likely to experience similar improvements, we can’t help but re-orient our view on Energy prices. We began the year thinking that prices had a cap around $55 and any forays beyond that level would revert lower. Today, we have to re-orient our view to one where it would be reasonable to expect energy prices to experience structural, gradual declines over coming years.

Rupee Strengthening Alongside Declining Crude Oil Prices Bode Well for India’s Domestic Economy

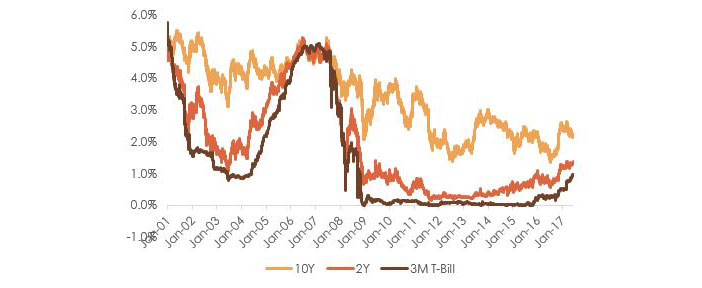

Is the Fed Caught In a Self-Fulfilling Loop?

Count us into the group that is perplexed by the Fed’s doggedness in raising rates. U.S. economic data has been rolling over the past month. Whether it be building permits, housing stats, construction spending, mortgage applications, a flattening out on disposable incomes, decelerating retail sales, slowing automobile sales, dismal factory orders, declining durable goods orders, we’re hard-pressed to find much economic activity that requires a rate hike.

The Fed seems to be worried about the next downturn and is actively moving towards a positioning that will enable them to cut rates by 200-300 bps if and when the next recession occurs. But the bond market is responding in its own ominous way. The net effect of a rise in short term rates with no attendant economic pickup is a flattening and possible eventual inversion of the yield curve.

In it’s good intentions, we think the Fed may be involved in a self-fulfilling prophecy, by contributing to a slowing down of the U.S. economy through their actions and sucking liquidity out of the system. It’s a situation that bears watching.

With Rising TBill & 2 Year Yields, the Gap Vs the 10 Year Has Narrowed Substantially…

Outlook

In a world where information is easily accessible, there’s always something to keep investors’ fear levels elevated. Unfortunately investing isn’t deterministic; rather, we operate in a world mired with probabilities and unique new inputs.

As we’ve stated often, dispersion in outcomes will be wider than ever. Despite elevated fear and calls for a correction and much worse, we think it’s prudent to be buyers on sell-offs rather than be sellers on rallies. It never ceases to amaze that two investors can consider the same data and come to diametrically opposed views.

We remain data driven for the most part. For now, top line growth in a challenging quarter gives us comfort and we’ll ride out the volatility or add to positions. We see positive triggers ahead in the form of 7th pay commission payouts, farm loan waivers, what looks to be a decent monsoon and a stabilizing rural situation, declining inflation, decent room for rate cuts, improving government finances, a widening tax base, shift to organised, improving productivity in the longer term, and an environment that benefits organized players as just a few factors that promote a continued positive outlook on the markets.

On the issue of valuation, we remain agnostic to index valuation, preferring to focus instead on the valuation paid in client portfolios relative to the stream of future earnings and growth opportunity.

Technical Strategy

The Nifty has been largely sideways to negative for last couple of weeks and closed at 9575 levels. Index has broken short term rising support trendline on daily chart and closed below it. Still it has support zone of 9560-9530 and sustaining below it on tradable basis may see pressure in the market. Also, in Nifty put options, 9500 strike price has highest open interest suggesting an important support for the market. Momentum indicators have given negative crossover with their respective averages on weekly chart now, suggesting market may see decline towards 9340 levels if it fails to hold 9560-9500 support zone. On the upside 9700 strike price call option has the highest open interest in Nifty options which is acting as technical resistance for the market. Thus, if sustained above 9700, next level for the market is seen at 9880 and then at 10,040 levels. Nifty options Put/Call ratio is closer to neutral level of one and currently at 1.10. INDIA VIX has stabilized around 11 levels for the last couple of months and is now at 11.56 levels. If there is any major spike in volatility, this will be cause of concern for the market.