Oct 15, 2018

The most important thing is to have a sense of where we are in the business cycle – Howard Marks GlobalAdverse Central Bank Policy, a Strong Dollar and Crude

Amidst clear signs that the Fed is planning to continue to hike interest rates this year and next, and withdraw liquidity, developed markets caught the EM flu and experienced a sharp bout of selling last week. Ironically, crude declined sharply to $80.5 levels and the INR strengthened to 73.5. The global policy environment remains bleak, with trade wars, rising interest rates in the U.S., shrinking central bank balance sheets and high crude oil prices. Add to that rising tensions between the Saudis and the U.S. over the disappearance of a Saudi journalist.

Recessions Risks Have Risen in the U.S. to 14.6% from 4.06% at the Start of 2018

The trade war has started affecting the U.S. and China. According to the New York Federal Reserve, the narrowing of the 10-year 3-month Treasury spread has increased the probability of a recession by the end of August 2019 to 14.6%. This is the highest level since late 2008. The estimate of a recession starting within one year was just 4.06% at the end of December 2017. Note that markets tend to top out 6-9 months ahead of recessions.

World Trade Showing a Slowdown as the Trade War Begins to Impact Global Growth

China’s car sales fell the most in nearly seven years in September, stoking concerns the world’s biggest auto market could contract for the first time in decades this year amidst rising worries about growth and a bitter trade war. Vehicle sales slumped by 11.6% to 2.39 million units last month, the third straight decline.

German industrial output dipped in August for the third time in as many months, suggesting Europe’s largest economy has also decelerated in the past quarter. Industrial output fell 0.3% in August, missing expectations of 0.4% growth. It followed a fall of 1.3% in July.

India’s passenger vehicle sales have slipped as well, at 292,658 units in September, down 5.6% from 310,041 units a year earlier. Rising crude oil prices, higher interest rates and a weak rupee lifted prices of imported vehicles. This is the first time that year-on-year passenger vehicle sales have fallen in three consecutive months since April 2014.

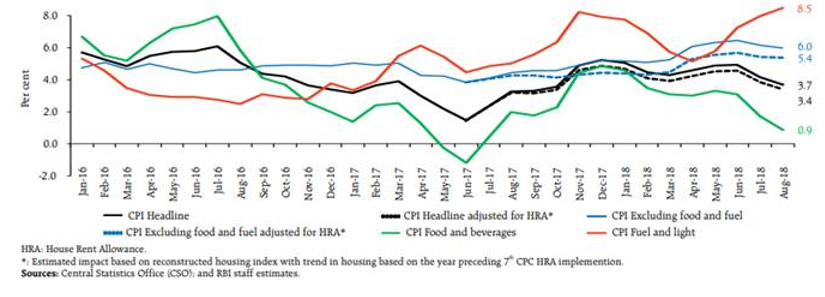

Domestic Inflation Has Yet to Feel the Impact of Rising Fuel

Domestic

Inflation Has Undershot Projections Domestically and Globally

Amidst the slowdown, however, expectations that inflation would rise to 5.1% have not come to fruition due to benign food inflation. There has been no visible impact on CPI of rising fuel prices due to favourable food supply and soft rural wage growth in spite of the quickening of agricultural activity.

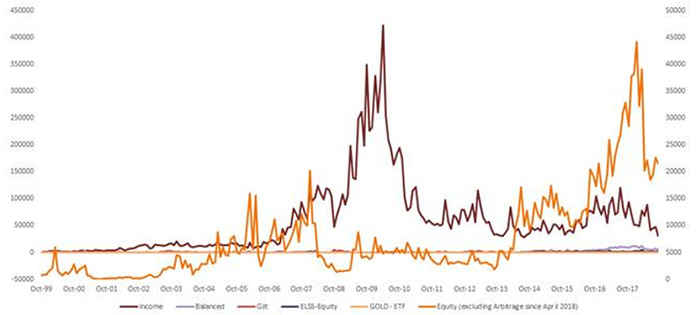

Meanwhile, Domestic MF Equity Flows Have Held Up Better Than Expected…

The domestic mutual fund investor was selling quite frantically in Jan 2018, but sales have slowed in September. Further, the domestic equity investor continues to reliably pump in around INR 10,000 Cr. a month on average into equity mutual funds. We can expect a slump in flows in October, but it appears that investors have not sworn off equities. SIPs have remained stable and rising at INR 7,700 crores a month.

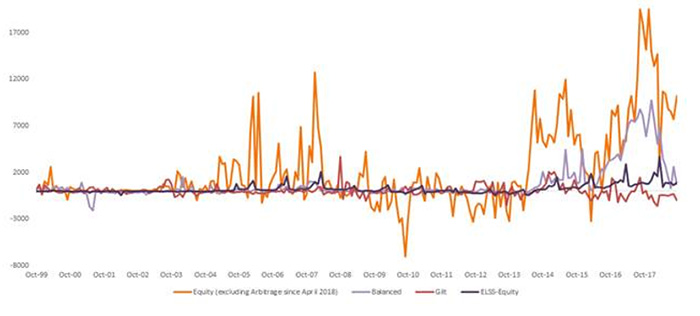

Sales in Equity MFs Peaked in January 2018 …

There’s Been No Recent Pickup in Selling in Sep 2018

Net Flows into Equity Funds Remain Solid But Have Come Off Highs Set Last Year…

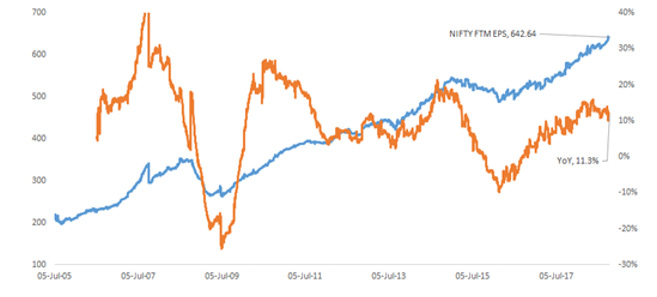

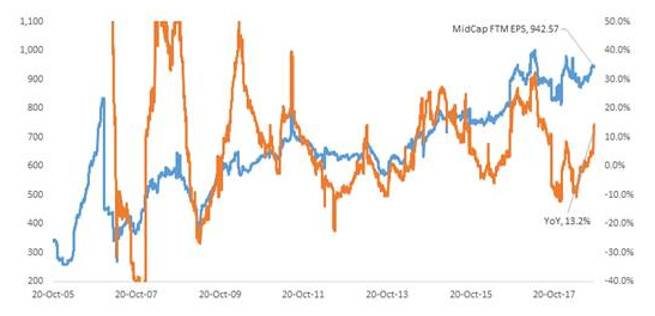

While Forward EPS Are Unreliable at Times, the Trend Does Provide a Look into Company Level Commentary…

…Nifty FTM EPS Estimates Continue to Rise on an Absolute Basis, but the Rate Has Slowed

While Nifty Midcap FTM EPS Estimates Remain Stuck in a Range…

And Nifty Smallcap FTM EPS Estimates Look to Have Peaked Earlier This Year

FTM EPS Revisions Are Rolling Over

While analyst forward estimates can be unreliable at times, the trend in analyst EPS revisions is usually driven by management commentary, and does provide color into aggregate views on earnings and the economy. Absolute Nifty forward EPS have been on a steady move higher, but the year over year growth has decelerated since May ’18 at 15.9% year over year to now being up 11.3% year over year.

Earnings revisions for midcaps remain stuck in a range, with some improvement of late. Small cap EPS estimates look to have peaked earlier this year. EPS growth estimates across cap structures have shown deceleration.

Outlook

Key Macro Risks Remain – Business Cycle Risk, Slowing Global Growth, a Hiking Fed, Trade Wars and FI Selling

There remains remarkable complacency in the U.S. markets. Equity ownership as a percentage of financial assets is at an all-time high. The U.S. equity investor is fully invested. The U.S. is in a late stage bull market cycle, and the momentum of yield curve spread inversion, if not absolute inversion, alongside rising interest rates will impede the economic recovery. Making matters worse, the Fed remains on a tightening path.

The macro will be driven by trade war discussions, sparring and negotiations, crude oil price action, and the Fed. The likely scenario has the Fed eventually pulling back on rate hikes, and a resolution to the trade war that has a win-win positioning. However, forecasting the timing is difficult. Notwithstanding sharp rallies, markets will struggle to maintain momentum as long as global growth is slowing and domestic headwinds remain. In addition, markets will have to work through election risk, domestically and in the U.S.

Global risks remain in place, with slowing down global economic data starting to impact confidence and spending. While earnings are likely to be robust domestically, that’s in the rear view mirror and what matters is how much the environment has changed in terms of liquidity, consumer confidence, rates, and funding.

Crude Oil Risks – Retail petrol prices are +17.7% in Delhi and diesel prices +24.9%

Crude has not helped, remaining above $80 and uncomfortably high. Crude costs will be seen in margins and declining sales, particularly on autos. Signs that credit growth is moderating have also emerged, alongside auto sales weakness. With rising EMIs, the urban consumer is likely to pull back their purse strings at the margin.

Sentiment Is Consensus Bearish

FI selling has been relentless this year and there’s been carnage in mid and small caps. There is consensus bearishness, and it is rare to find a bullish voice on the street. Clearly, sentiment can be classified as extreme bearishness.

Valuations on Growth Portfolios Have Gotten Cheaper

Much of this is embedded in the price. Our multi cap PMS portfolio sports a P/E multiple of 17.5 times FY 20, and will get cheaper with earnings announcements. Our large cap portfolio is at a reasonable 22.0 times FY 20. At some point, markets will get to attractively cheap, whether via earnings growth or price erosion.

Asset allocation

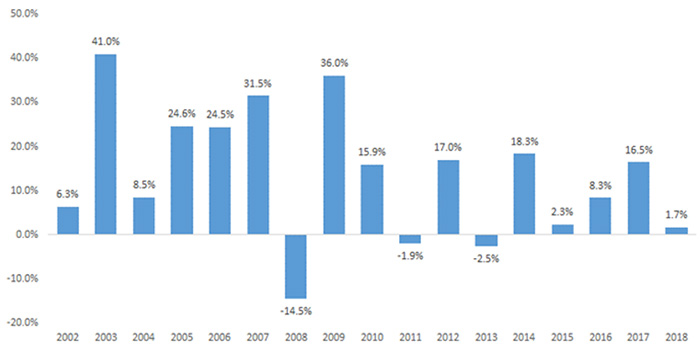

In the meantime, diversified portfolios have weathered the volatility better than aggressive equity only portfolios. Asset allocation is the time tested means of reducing volatility and an effective asset allocation portfolio generates higher optimized portfolio returns than any single underlying asset class. With regular rebalancing, returns can be further enhanced. We share the return profile of one such portfolio below, which has handily beaten a fixed income only portfolio with a long term CAGR of 13.4% with very low volatility.

Valuations for Our Large and Multi Cap PMS …

…Have Declined to 22.0 Times FY 20 for the Large Cap …and 17.5 Times for the Multi Cap

Asset Allocation Beats Fixed Income Returns Handily with Minimal Volatility…

…Delivering a Long Term CAGR of 13.4%

Technical Strategy

Equity markets closed in the positive giving some respite to bulls after five consecutive weeks of fall. But it was tumultuous in terms of volatility which hit 8-month high. Sell off in US markets added to weak rupee and crude oil price concerns. Still Nifty managed to recover on Friday and close at 10473 levels up by 1.5% for the week. Last week market tested the rising support trend line connecting lows of 6825 and 7893 after piercing it during the week. Nifty managed to bounce back after hitting 10138 a new low for the decline. For the week index has formed bullish candle with lower shadow at support trend line. Relative strength index has given positive crossover with its average on daily chart and moved above oversold zone. Thus, suggesting bounce back in market can continue. Now crossing above 10500 levels on sustainable basis, index can rally towards 10750-10850 which is the falling gap area resistance zone. On the downside if market trades below 10200 levels then index can see decline towards March’18 low of 9952 and 9870 levels which is 38.2% Fibonacci retracement of the major rise from 6825 to 11760 levels. In Nifty options, maximum open interest for Puts is seen at strike price 10000 followed by 10200; while in Calls it is seen at strike price 11000 followed by 10700 and 10800. Good amount of Put writing was seen 10000 to 10400 and Call unwinding in 10200 to 10600 was witnessed. India VIX closed lower by 9.3% at 18.63 levels on Friday. Further cooling off will help in forming short term bottom in the market and sustainable bounce. But since it remains at elevated levels, volatility is likely to continue in the market.

Nifty Daily chart