Feb 19, 2018

“Failure comes from ego, greed, envy, fear, imitation. I have success not because I am smart, but because I am rational” – Warren Buffett

XIV, VIX, PNB, PSU. It’s been an eventful fortnight, one that necessitates a review of the shifting investment landscape.

Global

The VIX Event Highlighted the Embedded Leverage in Developed Markets…

Why did the VIX skyrocket from historic lows in early February? One anecdotal account claims large players manipulated the bids on VIX without actually entering a trade, leading to a spike in the index, and a massive sell-off. Regardless of the mechanics, the event highlights significant derivative leverage currently hiding underneath so called vanilla products in developed markets. The recent episode highlights that India is inter-connected with the global world. Should this risk come forth – and let’s be clear we are not suggesting it is – India will suffer collateral damage.

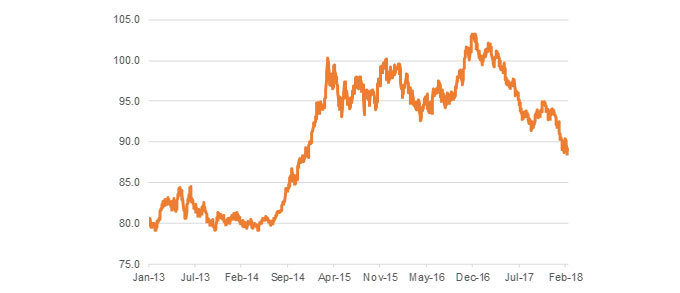

The Weakness in the U.S. Dollar Suggests a Reverse Flight to Quality…

The U.S. Dollar has been in a year long sell-off. One interpretation is that improving prospects in Europe, Japan and emerging markets are leading to asset diversification and capital outflows. Clearly, relationships between rates and currency appear to have broken down. Alternatively, a ballooning U.S. deficit, the specter of inflation and rising rates could be causing capital outflows. Japan has been an aggressive seller of U.S. treasuries.

The U.S. Dollar Has Been in a Year Long Sell Off

The U.S. 10 Year Has Risen 50 bps on Tax Reform, and U.S. Debt Continues to Rise Uncontrollably…

The tax reform bill was signed on December 22nd; since then, the U.S. 10 year yield has risen to 2.8% from 2.4%, and the federal government’s borrowing costs have increased by over 16%. In 2000, the U.S. federal debt was $5.6 trillion and real GDP $12.5 trillion. Today, federal debt has quadrupled to $20.6 trillion, while real GDP is only $17 trillion. The federal debt has increased 3 times, while GDP is up 36%.

The Powell Fed Is an Unknown Factor…

Separately, the Powell Fed is a relative unknown. We can surmise a continuation of the Fed policies of Yellen, but that’s conjecture. That the VIX event happened on the first week of the Powell tenure is an interesting side note.

Finally… Protectionist Trade Rhetoric is Brewing…

Over the past year, the U.S. has squeezed margins on Indian Pharma, squeezed jobs out of the IT sector in India and is mulling a massive hike in import duties on steel and aluminum imports against China and India. The US also imposed tariffs of up to 50% on imports of washing machines and solar panels from China and South Korea. Meanwhile, India recently announced import duties on electronic goods and components. China talks free trade, but is massively protectionist. Should a trade war break out, it’s first order impacts will be inflation, falling profits and slower global growth.

Domestic

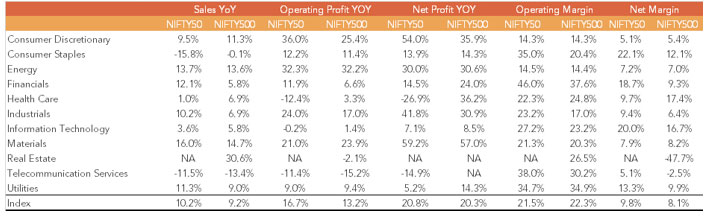

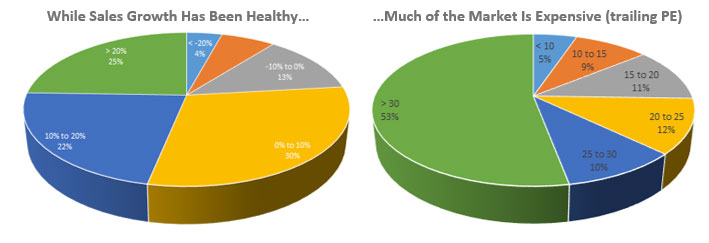

Earnings Growth for the CNX 500 (Ex PSUs) Is Up +20.3%

The PSU space has reported losses due to RBI mandated provisioning to the tune of INR 17,000~ Cr. Excluding PSUs, sales growth for the CNX 500 is up 9.2% and earnings growth is up 20.3%. A surprisingly high 52% of companies have beaten expectations. Inflation has moderated, and we have had the strongest two months of industrial production data in five years. A host of economic data, ranging from passenger and commercial vehicle sales, two and three wheelers, to capital goods manufacturing and bank credit continue to look healthy.

CNX 500 Earnings Excluding PSUs are Up 20.3%……Sales Are Up 9.2%

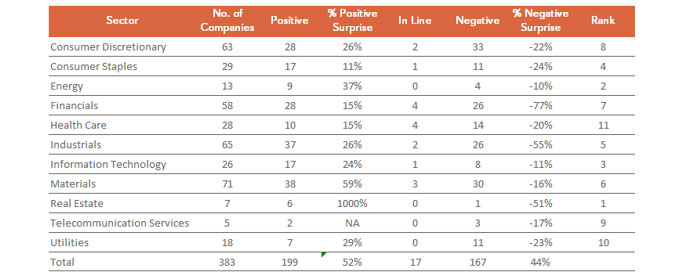

A Healthy 52% of Companies Have Beaten Estimates…

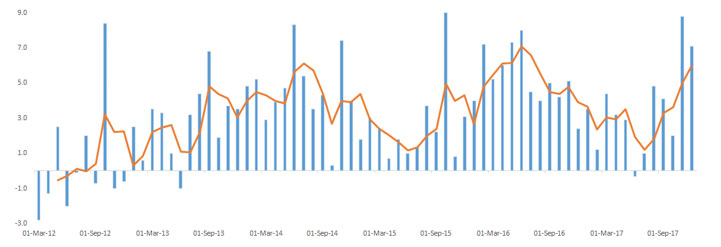

A Raft of Positive Economic Data Has Been Coming Forth… …Including Strong Industrial & Capital Goods Production…

RBI’s Change in NPA Resolution Procedure Accelerates the Debt Resolution Mechanism…

The RBI recently mandated that all existing categorization of standard stressed assets – SDR, S4A, CDR restructuring, and flexible restructuring under 5:25 scheme – be abolished, leaving IBC (insolvency bankruptcy court) as the only resolution mechanism. This is a welcome move in our view, as it creates a clearing mechanism that is straightforward. While in the short-term, this will increase the pain for the lenders, early identification and clear resolution will move us closer to a healthier banking system in the long term.

Outlook

Fixed Income

Interest Rates – PSU Clean-Up Is Pain in the Short Term, Positive Long Term

A lot of negatives are priced into current yields. Yields trade substantially above the repo rate and are factoring in two to three rate hikes. A major contributor to the increase in inflation has been rising crude prices. With crude selling off in 2018, some of that increase is likely to be offset. The government also has the choice of raising FI investment limits, and that remains a quiver in its bow it can use anytime it chooses.

With rising risks around PSU non performing loans and scams, we continue to recommend higher rated corporate credit with shorter maturities. We prefer short term funds for conservative investors. For investors interested in locking in current yields, and unwilling to consider notional NAV impacts, FMPs are another option that can be considered.

Equities

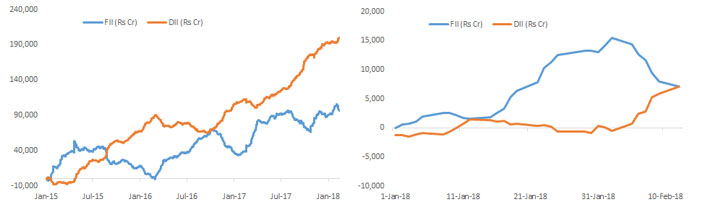

Domestic Investors Continue to Support the Equity Market

During the sell-off earlier this month, foreign investors pulled out INR 5,800 Cr. from equities, while domestic investors pumped in INR 6,700 Cr. Domestic investors were net buyers every day the week of Feb 5th.

An analysis of the cumulative net inflow into India by Foreign Institutional Investors shows an inflow of roughly INR 840,000 crores, or $130 billion, since 1999. This passes the stress test versus data provided by the IBEF. The vast chunk of this came through during the post 2009 to pre Modi years, as shown below. Since 2015, FIs have added a cumulative net $14 billion into equities, compared with $31 billion by DIs. Domestic investors have poured INR 6,600 Cr. into Equities in February (till Feb 14th), which makes for an average month. Our point: domestic flows have not slowed.

Domestic Investors Have Poured $31 Billion into Equities Since 2014……Compared with $14 Billion by Foreign Investors

The Maturing Domestic Investor

In the face of panic selling in early Feb, the domestic mutual fund manager, and domestic investor has remained remarkably calm to date. Domestic investors also exercised restraint in chasing the market in January 2018 and for now, appear unperturbed.

Valuations Remain a Headwind

In the current environment, with strong economic and earnings data, we prefer predictable growth at reasonable valuations. A move to large caps would make sense, but the relative lower growth and high valuations of large caps give us pause. A move to large caps would also need supportive data around rising inflation, rising headwinds etc. Those aren’t evident at this time, and margins remain healthy. The other alternative is value. That’s driven interest in IT stocks recently, which present supposed protection to the downside. But value is no panacea, and can also be a falling knife, as the PSU sector is amply demonstrating.

Global Growth Continues to Be Strong…

The global Manufacturing PMI is close to an 82-month high in January. However, with risk premiums rising, and investor complacency taking a backseat, upside will be driven by earnings growth in excess of fair value.

Recent Market Action Has Shifted to Ignoring Good News and Selling Into Rallies

Somewhat worrisome in the short term has been recent action that has seen the market transforming into a “sell the rallies” market. Good economic data and earnings data have been sold into. However, we derive some comfort in the technicals of the market having improved moderately since the early Feb sell-off.

Early and Late Stage Business Cycle Indications

A case can be made that several aspects that often coincide with the later stages of the business cycle such as rising interest rates, rising inflation, rising trade imbalances, investor euphoria and high valuations are evident today. However, the earnings recovery is just getting started, as is the economic recovery, held back by GST roll out, while inflation remains in the acceptable band.

Sectorally, Private Banks Poised to Gain Share

With the worsening woes of PSU sector, and focus inward, private banks will be able to gain ever larger market share. With rates likely to stabilize at current levels, private banks are well positioned to gain. Most PSU banks are vacating their market to competitors, with financial woes likely to linger on for a while.

Equities

This month has witnessed two warning shots across the bow – embedded leverage in the U.S., and potential risk embedded in the PSU banking system. The PNB episode is of concern domestically, as an unknown, and markets hate unknowns.

Cautious optimism remains our most prudent course of action. Regardless of whether the current sell-off materializes into something more, these risks do need to be acknowledged. In this scenario, capital protected strategies, long short strategies, and hedged portfolios would be prudent additions to portfolios. For investors unwilling to pay high premiums for protection, cheaper out of the money options, and futures hedging remain alternatives that can be easily structured.

For investors with a reasonable appetite for risk, bottom up equities remain the best place to be to deliver solid returns over a three year holding period.

While embedded risks have risen on the margin, we note that the fundamentals in the economy remain healthy. India has structural tailwinds that will continue to deliver growth. Until visible signs of a slowdown emerge, our preferred course of action remains staying the course and implementing tactical strategies structured around hedging, long short strategies, and capital protection strategies.

Technical Outlook

On Friday markets opened in green following positive overnight cues from U.S., but couldn’t hold onto the gains and sustained selling pressure through the day saw index closing near lows of the day forming a bearish candle. For the day Nifty closed lower by 0.9% at 10452 levels and on weekly basis closed flat. Index is seeing supply pressure above 10600 levels and unable to sustain above it. Index needs to sustain above 10640 levels for the index to rally towards 10740 which will fill falling gap area. In Nifty options, significant amount of call writing was seen in strike price 10500 and 10600 which is likely to cap any upside in near term.

The gap down opening of 6-Feb-18 had taken support at rising trend line originating from September 2017 low of 9769 and has seen bounce back. Also, the 100-day moving average that arrested the declines in month of September and December has again provided support to recent fall and index has been trading above it for last eight sessions. This support comes around 10400 levels suggesting this as an important level for the market. Breaking below 10400 levels, index is likely to retest recent low of 10276 level. Below that next support level for index is seen around 10100-10070 where 200 day moving average and previous swing lows are seen. For now, index is trading in range of 10400-10650 odd levels and break from the same will give direction to the market.

Nifty Daily chart