Oct 4, 2017

Thirty years ago, no one could have foreseen the huge expansion of the Vietnam war, wage and price controls, two oil shocks, the resignation of a President, the dissolution of the Soviet Union, a one day drop in the Dow of 508 points, or treasury yields at 2.8% and 17.4%. But surprise, not one of these blockbuster events made the slightest dent in Ben Graham’s investment principles. Nor did they render unsound the negotiated purchases of fine businesses, at sensible prices. Imagine the cost to us then, if we had let fear of the unknowns cause us to defer or alter the deployment of capital. Indeed, we usually made our best purchases when apprehensions about some macro event were high. – Warren Buffett

Performance Review Q3 CY 2017

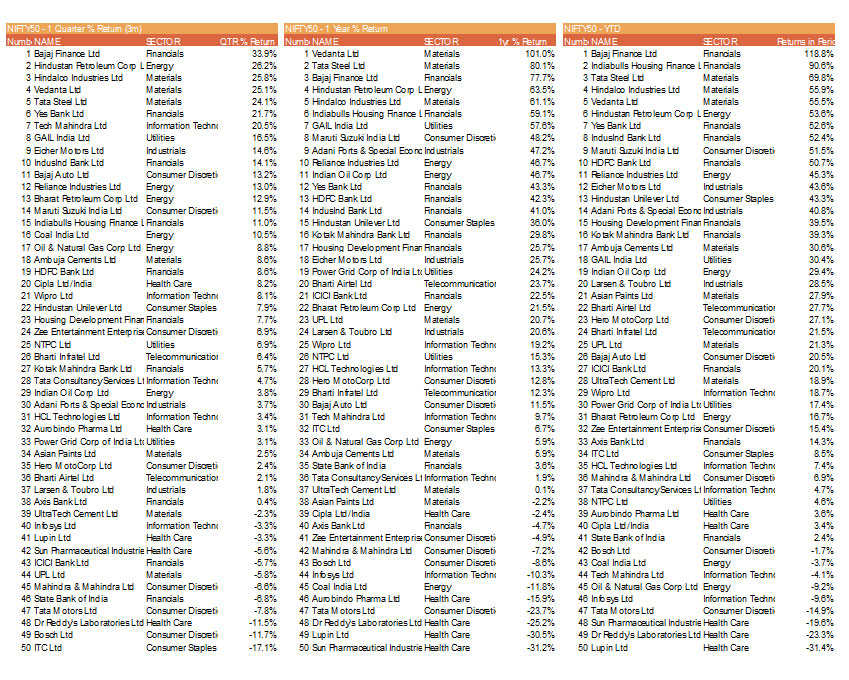

Nifty 50

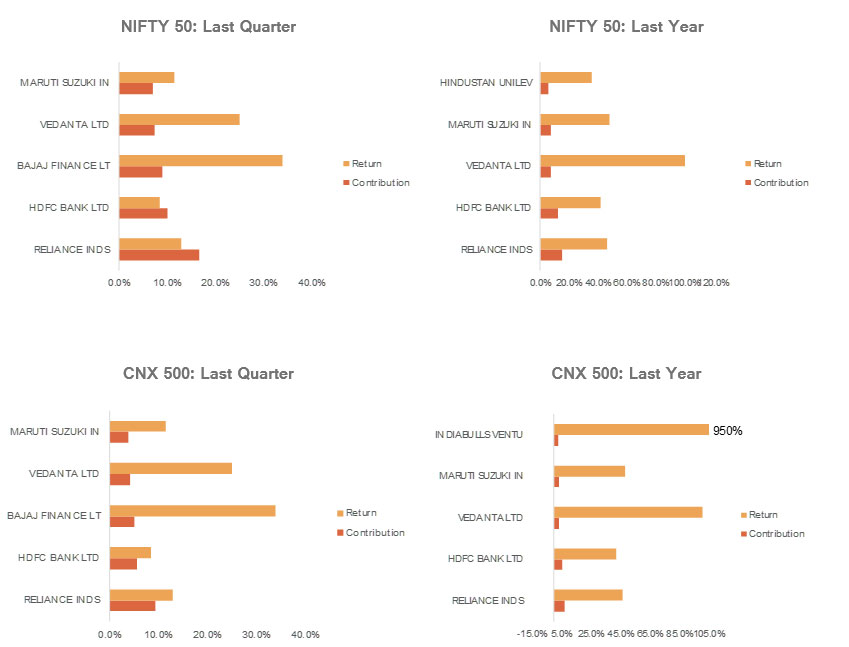

In the quarter gone by, Financials, Commodities and Energy claimed the top 10 spots. Financialisation domestically and the global uptrend in commodities provided useful tailwinds. Bajaj Finance, Hindustan Petroleum and Vedanta were the major winners. At the bottom of the pack were Health Care and Consumer names such as Lupin, Dr. Reddy’s, M&M and ITC.

Year to date, Financials and Commodities dominated yet again, with the former claiming 5 of the top 10 slots. Bajaj Finance, HDFC Bank and Yes Bank performed well. Tata Steel on the back of the Thyssenkrupp deal and Vedanta drove the commodities pack. Health Care has continued to perform woefully in the YTD period as the stress seen during the year so far from the U.S. FDA and the increasingly difficult U.S. health care market is yet to alleviate convincingly.

For the year over year period, 29 of the 50 stocks delivered hurdle returns of 12% or higher. Materials, Financials and Energy broadly claimed the top 10 positions. Similar underperformers as in the YTD period populated the bottom of the pack.

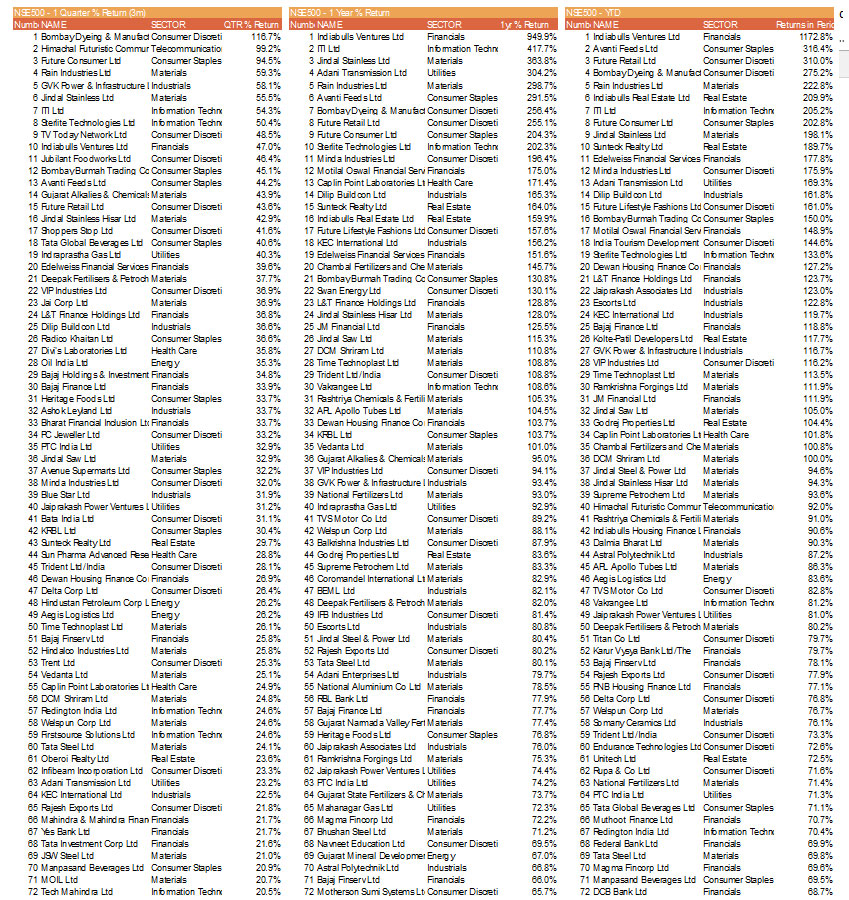

CNX 500

From a quarterly perspective, the CNX 500 top 10 demonstrated much more vigour vs. the NIFTY top 10. Much of the action seemed forward expectations driven in Future Consumer, Himachal Futuristic on a base-less partnership with R-Jio and Rain Industries on the back of sustained Aluminum demand for its Coal Tar Pitch, hence corroborating the commodities uptrend, and strong Carbon demand.

Year to date and year over year, the Consumption theme dominated in the top performers. Indiabulls (Ventures and Real Estate) was the lone house in to represent the Financials pack. 290 of the 500 stocks delivered 20% gains last year, with much of the rally fueled by mid-caps. Heath Care and select Consumer Discretionary names constituted the bottom of the pack for the YTD and 1 year periods.

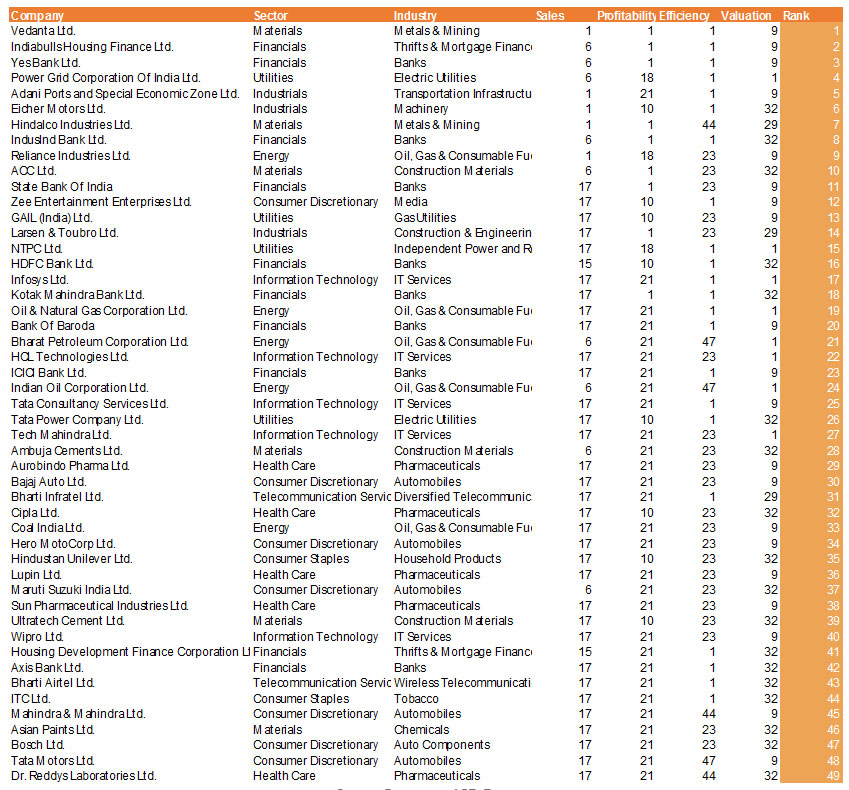

Fundamental Strength Ratings

Based on growth, profitability, margins and valuations we score each company. We have excluded Tata Steel from both index fundamental ratings because of a huge loss in last year’s corresponding quarter.

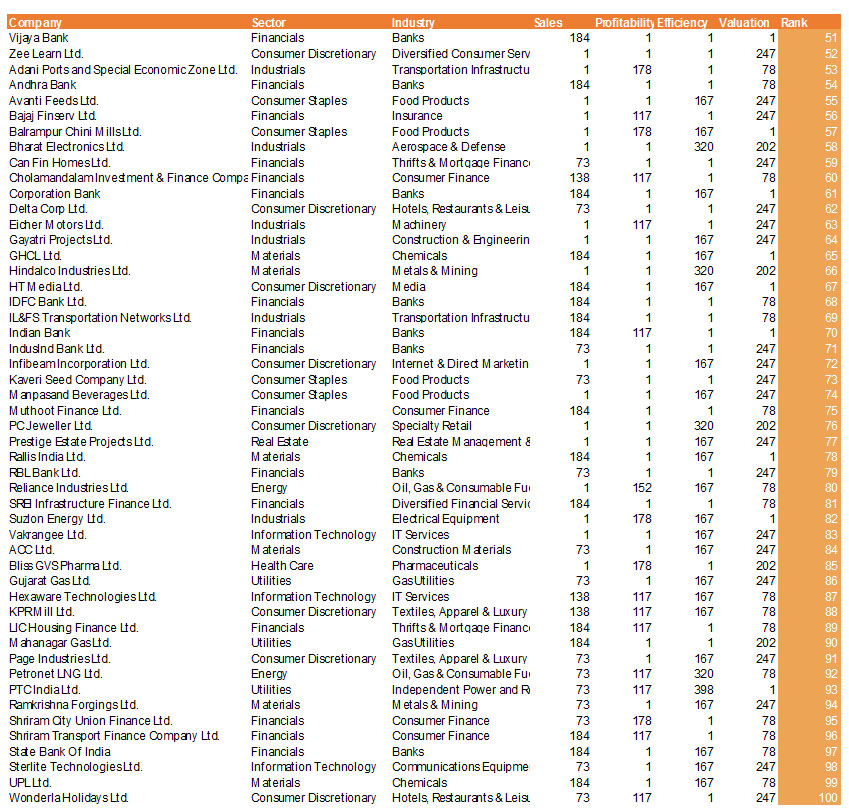

Nifty 50

Vedanta, Power Grid, Eicher and Yes Bank were some of the prime performers in the top 10 fundamentally sound Nifty 50 companies. Dr. Reddy’s, Tata Motors, Bosch and M&M scored lowest on our fundamental scoring mainly dragged by sagging bottom line (de-)growth and incompatibly high valuations.

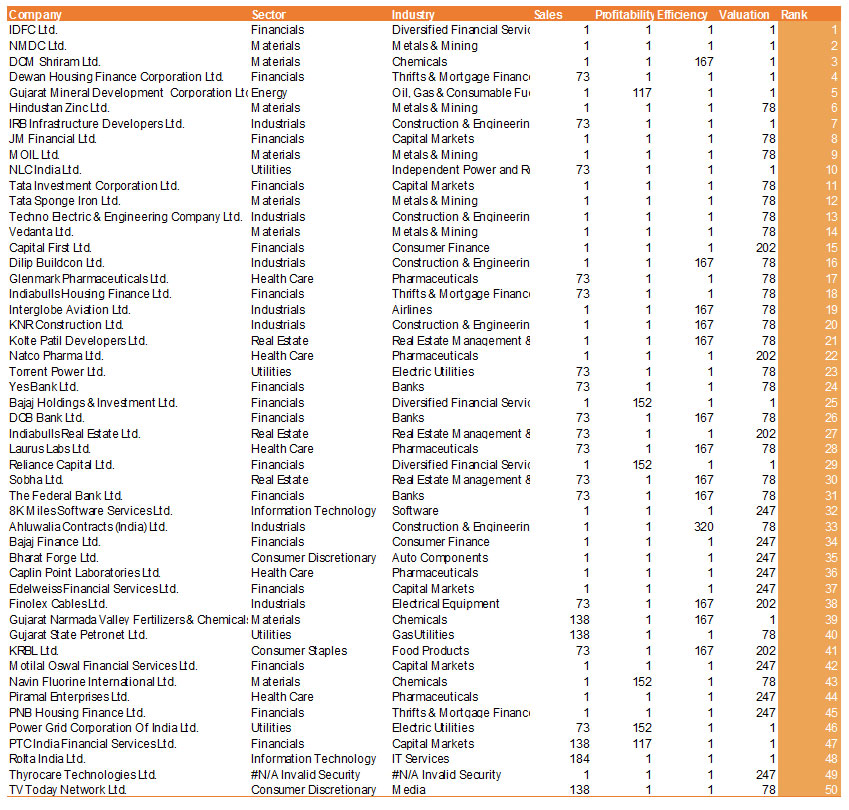

CNX 500

Financials and Commodities, in particular, Metals and Mining fared extremely well on sales and net income growth along with good profitability.

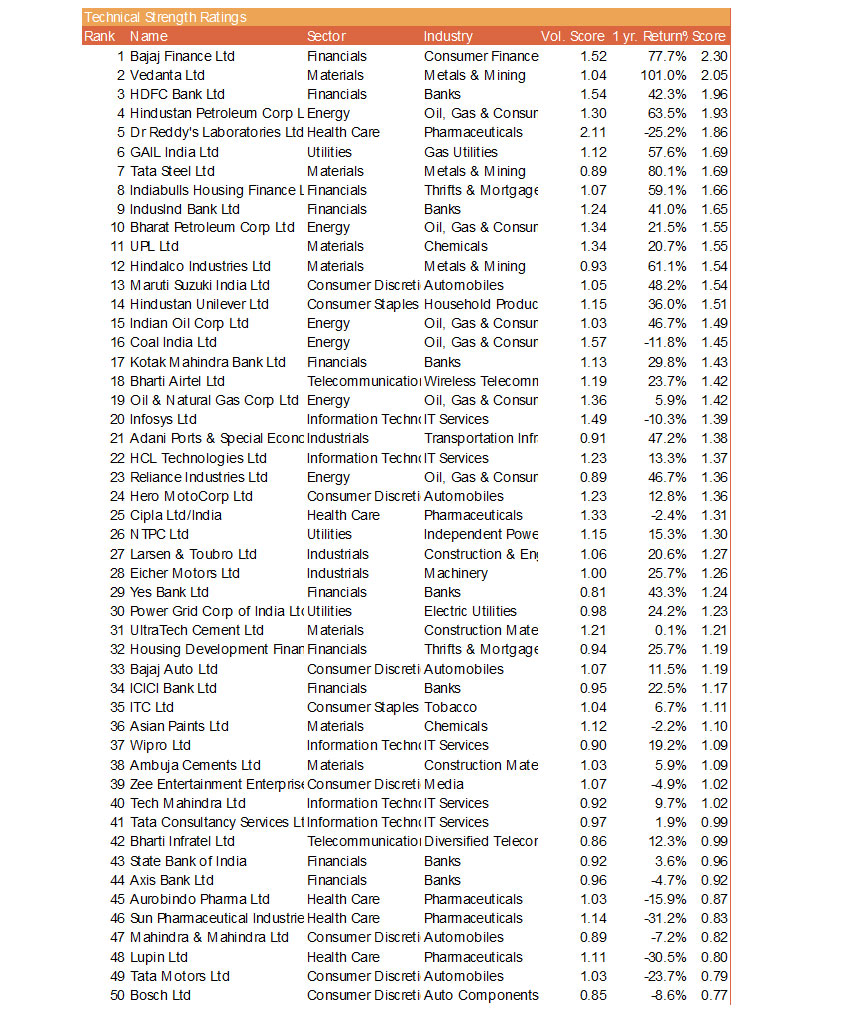

Technical Strength

Our technical ratings track technical factors such as volume and momentum as well as returns to come up with a technical score for each company.Nifty 50

Financials (Bajaj Finance, HDFC Bank) and Commodities (Vedanta, HPCL, GAIL, Tata Steel) exhibited strong technical momentum boosted by a good mix of positive short and medium term volume momentum. On the other hand, negative momentum plagued Consumer Discretionary (Auto makers Bosch, Tata Motors, M&M) and Health Care (Sun Pharma and Lupin).

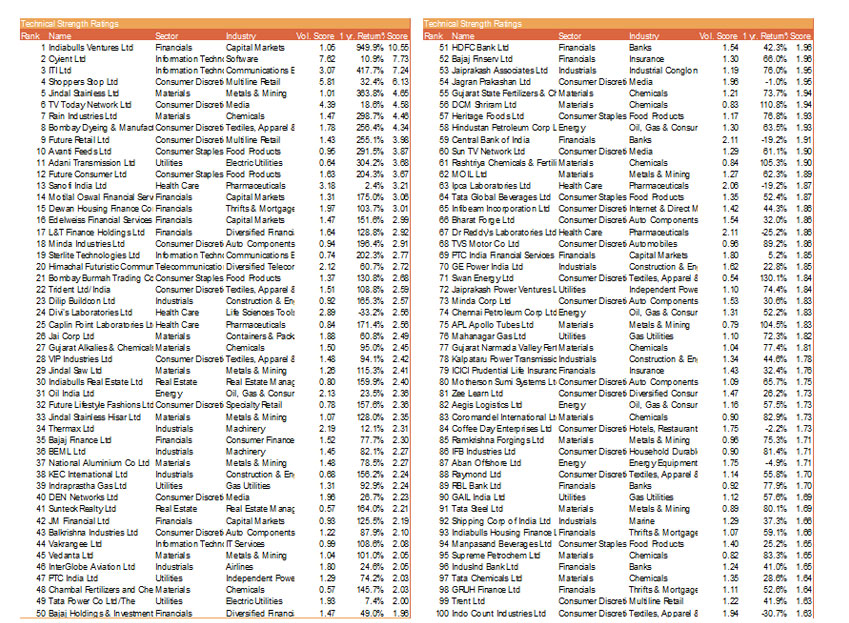

CNX 500

Investors chased Materials (Rain Industries), IT (Cyient and ITI) and Consumer (Shoppers Stop on the Amazon Deal, Future Retail among the 5 Consumer names in the top 10).

Much of the action in CNX 500 volumes was seen in the large cap space which witnessed ~110% of the usual weighted (short, medium and long term) volume momentum. Sector-wise, IT and Telecom saw the most volume activity.

Earnings Revisions

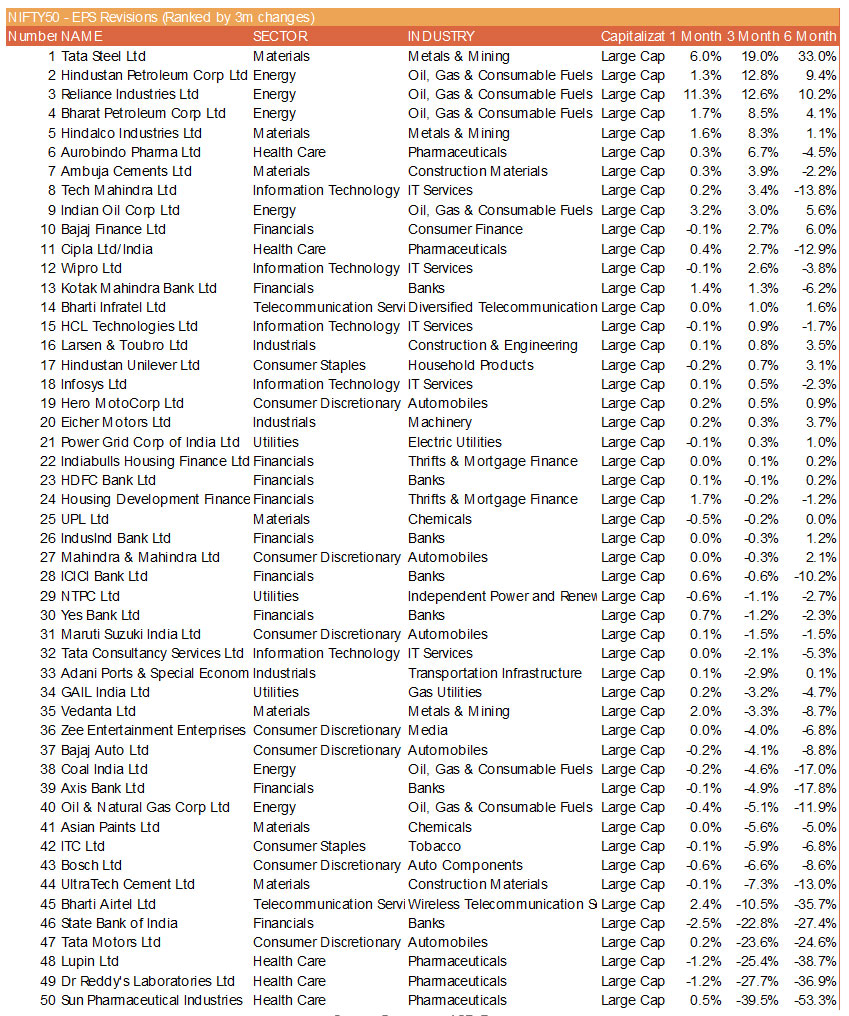

Nifty 50

Earnings revisions have been positive for Nifty 50 on average in the last month seemingly signaling out a bottoming of earnings projections as the last 3 and 6 month revisions are both negative.

Tata Steel continues to maintain the strongest upward revisions across all periods (as seen in Q2CY17/June ending as well). The OMCs (HPCL and BPCL majorly) and Reliance Industries were other noteworthy companies with upward revisions. The 3 heavy weight pharma names: Sun Pharma, Lupin and Dr. Reddy’s continue to suffer deep earnings downward revisions. Within Industries, Oil and Gas and Metals and Mining witnessed positive earnings revisions.

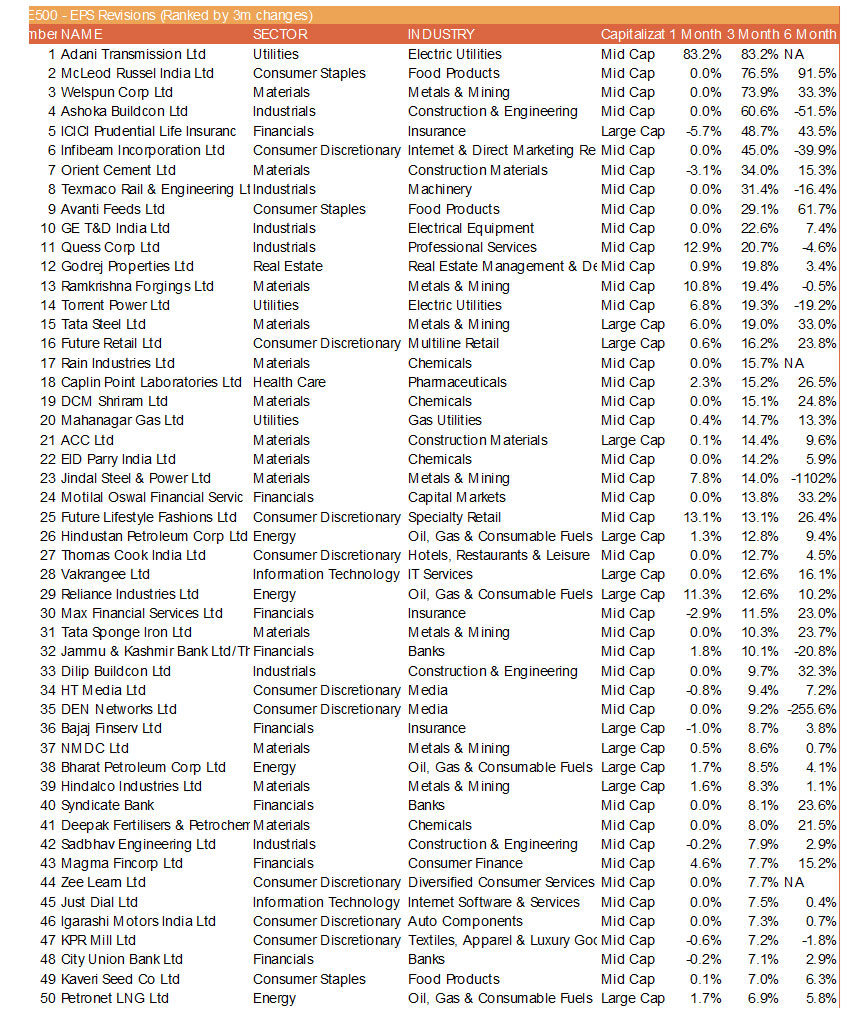

CNX 500

Similar to the Nifty 50, the CNX 500 on average also reported slightly improving earnings projections over the last month, while last 3 and 6 months still saw earnings cuts. Much of the optimism in the last month was driven by mid cap earnings re-rating. On the other hand, small caps witnessed severe cuts over the longer 3 and 6 month periods.

Utilities (mainly, Electric Utilities segment) again demonstrated earnings expectations progression. Energy as well exhibited improving earnings expectations. Telecom, Health Care (primarily Pharma industry) and Industrials (Construction & Engineering and Transportation Infrastructure) had much of their earnings estimates slashed.

Outlook

A shot in the foot. Not to be confused with a shot in the arm. Looking at the past year’s economic indicators, twice the economy has been on an upswing, and both times the momentum has drained on reform related shocks.

Angst Rising

The story this fortnightly is the rising angst that we are seeing in conversations with small business entrepreneurs, large businesses and consumers. The rapid deterioration in the discourse is symptomatic of the months of discomfort that have been suffered by many factions of the economy. A scant two months ago, the market appeared unstoppable and prices were rising on strong flows. We have been concerned about the situation since early August, and the rhetoric has only worsened since that time.

But…We are Not Ready to write off the Structural Bull Yet

Rates are low, inflation is low when viewed from a larger prism. Earnings revisions appear to be bottoming. Automobile sales in particular look healthy, and the robust numbers for commercial vehicles suggests that the government may be stepping up their investment plans. Auto sales are a strong indicator that the consumer remains willing to spend. Other economic indicators would appear to be muddling along. Animal spirits raged in the IPO market, but now to a lesser extent, and it would appear that smart money is cashing out while new money is pouring in.

While Valuations Are High, They have Been High for Three Years Now

One of the most common refrain from investors is valuations are high. That has been the case since 2014. Despite this, actively managed portfolios have delivered strong returns, despite two sharp sell-offs, and we remain of the opinion active managers will continue to outperform the index.

All Eyes on the Stimulus and Earnings

For years now, consumers have watched their burden rise while prospects for jobs and job security grow dimmer. A stimulus that frees consumer disposable income, creates jobs and energises the consumer is the need of the hour. A pickup in demand will attract investment capital, not the other way around. There is plenty of capital available today; it is the lack of attractive investment opportunities that is an issue. Addressing infrastructure is another worthy endeavour, but we’d look for a focus towards urban infrastructure renewal, as the cities of the nation are suffering from painful daily traffic jams.

A PSU bank recapitalisation will be met with a tepid response by the markets. Any stimulus intended to spur corporate investment will also likely not deliver the boost that is needed.

Separately, the government is working on resolving concerns related to GST and will, we believe, make necessary changes.

There is a time for offense and a time for defence. Heading into what appears to be a vulnerable earnings season, our strategy is titled towards including a bit of defence. Sectors exposed to financialisation look likely to do well. Visibility on the automobile sector, energy and materials is also quite strong.

We remain cognizant of the possibility that a stimulus package is in the works, which could be well received by the markets. This is which is why we cannot be bearish in what still appears to be a bull market.

For diversified portfolios, we are actively engaged with clients on conversations around short term protection and positioning, while actively preserving exposure to upside.

For our PMS and actively managed portfolios, we have paid a small premium to protect portfolios. We are focused on protecting what has turned out to be a healthy year in terms of returns. We are also actively looking to rotate to emerging growth stories that are reasonably valued with expected strong growth in future earnings.

Performance Attribution Q3 CY 2017

A deeper analysis of the two flagship indices, the Nifty 50 and CNX 500 across stocks, sectors, industries and market caps reveal insights and implications in terms of portfolio performance.

Nifty 50 Performance – Quarter, YOY and YTD

Source: Bloomberg, ACE Equity

CNX 500 Performance – Quarter, YOY and YTD

Source: Bloomberg, ACE Equity

Fundamental Strength Ratings Nifty 50

We rank the Nifty 50 by growth, profitability, margins and valuation below to come up with a fundamental strength ranking.

Fundamental Strength Rating – Nifty 50

Source: Bloomberg, ACE Equity

Fundamental Strength Ratings CNX 500

We rank the CNX 500 by the same methodology.

Source: Bloomberg, ACE Equity

Fundamental Strength Ratings CNX 500 (continued)…

Source: Bloomberg, ACE Equity

Technical Strength Ratings Nifty 50

Source: Bloomberg, ACE Equity

Technical Strength Ratings CNX 500 (continued)..

Source: Bloomberg, ACE Equity

Contribution Analysis – Returns & Contributions

Source: Bloomberg, ACE Equity

Earnings Revisions Nifty 50

Source: Bloomberg, ACE Equity

Earnings Revisions CNX 500

Source: Bloomberg, ACE Equity

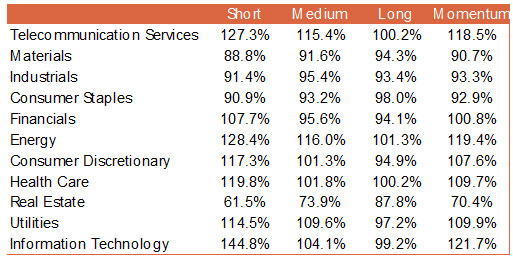

Performance by Capitalization & Sector – CNX 500

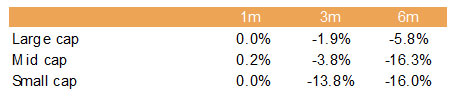

EPS Revisions

EPS Revisions Neutral for Large Caps in short term, but still negative overall for longer periods

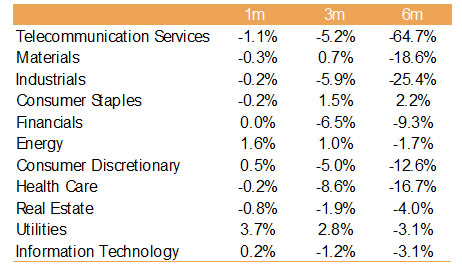

EPS Revisions Positive for Utilities and Negative for Telecom and Industrials

Source: Bloomberg, ACE Equity

Volume

Volume Momentum Is Strongest in Large Caps

Volume Momentum Is Strongest In IT and Telecom

Source: Bloomberg, ACE Equity

Technical Outlook

The Nifty managed to recover some of the losses at the end of the week’s close at 9789 levels down by 1.75%. Last week’s index made low of 9687 and has seen some bounce back. However, looking at the price action of Nifty over the last couple of months, index has formed bearish double top formation. But the confirmation of the pattern will come, once Nifty breaks below 9685 levels and starts to trade below it on a sustainable basis. In case index breaks below this level then the market may see decline towards 9450 initially and then 9230 possibly which is the pattern target. Thepositive for the market has been that, Nifty tested August low of 9686 and has seen buying coming in to the market. Thus, holding above 9685 market is likely to see bounce back towards 10000 levels. In Nifty options 10000 strike price call option has open interest which is likely to act as cap for the market in the near term. Nifty put/call ratio is at 1.20 and off its extreme levels, suggesting market has room on upside. INDIA VIX has also seen cooling off to 12.48 after touching high of 14.16 last week. However, rise above 14.20 levels on sustainable basis will be negative for the market as it can further rise towards 16 levels.

Nifty weekly chart

Source:Falcon7