Feb 1, 2021

• Commentary on bubble-like equity market conditions has reached a frenzy.

• Equity market valuations are stretched, but that is not a useful signal for predicting a sell off.

• The long term factors that have supported exaggerated valuations are still very much in play.

• Would investors really substantially sell equities ahead of President Biden’s fiscal boost?

• Inflation is the greatest risk to the equity rally and consequential rise in long term rates.

• We see room for profit taking, but there is too much money on the side-lines waiting to go back in.

• If it’s a bubble – it can probably get still larger.

The current commentary on bubble-like equity market conditions has reached a frenzy. The Robinhood investors assault on hedge funds, and the sharp appreciation of equity markets almost perversely in line with the rise in global COVID cases has commentators reaching for their pens to call time on the ‘bubble’ in equity markets. Try as you may, there is no easy way to unwind bubble-like conditions in financial markets. To paraphrase Alan Greenspan, we don’t get drawn into whether there is a bubble, we should stand prepared to pick up the pieces afterwards!

In our view, there is a difference between long term factors that have created a potential bubble in equity markets and short-term factors that can exaggerate them to breaking point. Let us start with a longer-term perspective. For this, we need to cast our minds back to the financial crisis of 2007-09. The developed world has never righted itself from the legacy of that crisis. Emergency programs to support global growth have become institutionalised. The world remains awash with quantitative easing that has inflated asset prices. Also, governments have been able to ‘artificially’ inflate growth and even today can still spend money like it is going out of fashion. The global financial crisis, in essence, has never ended and many of the asset markets have had continued exaggerated returns from exaggerated levels of support from policymakers. In essence the bubble in the asset markets of the developed world has existed for some years but we don’t see any appetite amongst policy makers to deflate/prick this bubble anytime soon.

Some of the concern about market bubbles has focused on the actions of retail investors. We find some of the commentaries around the Reddit readers’ assault’ on the equity market as disingenuous. Just because someone does not have substantial wealth does not make them any less intelligent about investing markets. The Reddit readers’ strategy of investing in companies where there has been an outsize short position put on by hedge funds is the kind of trade that a hedge fund would have employed. The issue of outsize rallies in the market is an issue for the regulators. The suggestion that there is something untoward about investors buying stocks as opposed to selling stocks they don’t own beggars belief.

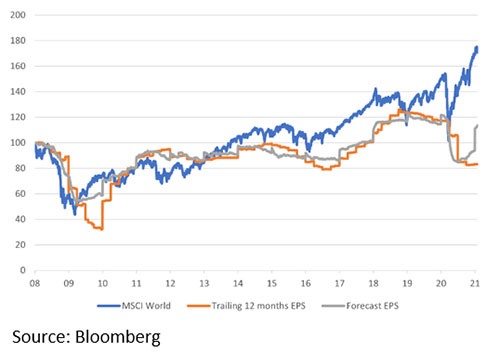

Chart 1 shows a very telling story of the discrepancy since 2008 between the substantial rise in global equity markets and the shocking lack of corporate profits growth. While corporate profits for the MSCI World index have fallen 20% since 2008, the global stock market has risen nearly 80%. Of course, 2020 was extraordinarily bad for corporate profits. Hence, we instead looked at analysts’ forecasts for the current year. Even using analysts forecast for corporate profits in 2021, the level of analysts’ estimates is just 10% above the 2008 base. The numbers imply a 70% re-rating of equities, much of it concentrated in the last 12 months.

Chart 1: Global Equity Index outpaces corporate profits by a good margin

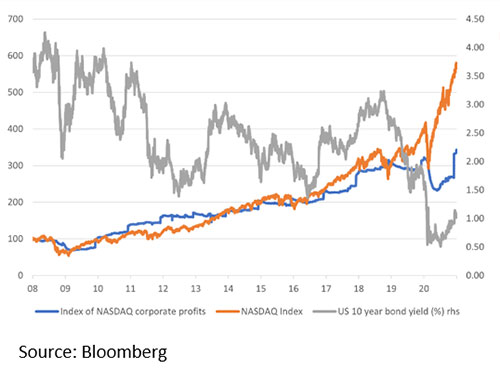

The rise in the NASDAQ Index, like the broad market, has far outpaced corporate profits over the past year (Chart 2). Before the COVID crisis hit, the index and corporate profits had moved mostly in line with each other. The rise in the NASDAQ index has received significant support from the marked fall in long term interest rates. With inherent strong long-term revenue and profits growth, the technology sector is less affected by the decline in nominal global GDP growth. Hence it benefits most from a valuation perspective from the very substantial fall in long-term interest rates. The US 10-year bond yield has fallen from 3% to just 1% over the course of two years. However, even adjusting for very low long term interest rates, the very sizable gap between the level of the index and the level of corporate profits is extreme.

Chart 2: Nasdaq index far outpaces corporate profits but helped by lower long-term interest rates

These two charts suggest there is room for profit-taking or a significant unwind of a seemingly large over-valuation of markets. However, valuations have proven to be a poor data point for making a profitable judgment about whether the global equity markets will correct.

Short term factors in our view remain supportive of markets irrespective of the high valuations. We would still contend that policymakers’ actions will keep equity markets in the ascendancy at least through much of this year. Would an investor seriously want to sell equities ahead of the likely significant fiscal boost in the United States? President Biden is committed to a fiscal package of $1.9 trillion equivalent to 8% of GDP. Most major central banks remain committed to maintaining interest rates at historically very low levels.

We continue to believe that the greatest risk to today’s equity bull market is from a significant rise in long-term interest rates. The risk in the first half of the year is that the equity market worries about the pause in the economic recovery US and Europe simultaneously as inflation starts to climb and spooks the bond markets. In the past week, while economic data for January has been weak, inflation data has come in ahead of expectations. Inflation data in the US, Germany and the United States were ahead of economists’ estimates. The consumer spending crunch in the second quarter of 2020 sent US inflation close to 0%. It has since rebounded to 1.4% and by most economists’ estimates should go to 2.5% of higher by the middle of the year.

However, if US bond yields were to rise markedly and precipitate significant equity market disruption, we would expect the Fed to intervene to drive down bond yields through quantitative easing. Fed Chair Powell was at pains last week to emphasise that the Fed is in no mood to back off its quantitative easing.

Technical factors have been screaming bubble/’exaggerated enthusiasm’ for some weeks. And to be fair short-term signals do indicate room for a meaningful setback but not a crash. Indicators of investor exuberance are evident in call buying volumes (20 year high), levels of leverage among US professional investors (second-highest reading of all time), greed-fear index (all time high).

Bottom line we see room for profit taking, but there is too much money on the side-lines waiting to go back in. If it’s a bubble – it can probably get still larger.