Sep 1, 2021

• Normal Fed monetary policy is still a long way away as Jerome Powell presses the ongoing near-zero rates

• The bond market embraces the loose money and leaves longer-dated bond yields close to 1.30%

• High yield bonds continue to accrue return

• Equity markets enjoy loose monetary conditions but may fret about the impact of the delta variant

• Be aware of the risk of downgrades to corporate profits forecasts if the economists are right on a global slowdown

• Tactically Japan and European equities preferred over the US.

The financial markets are still struggling to return to anything that the mind can consider normal. Last week, Fed Chair Jerome Powell in his major Jackson Hole meeting was quite forthcoming to endorse that the start of the road to a normal level of interest rates was still many quarters away. Meanwhile, the delta version of COVID-19 continues to stall economic activities across the globe. Maybe we are in a new normal – we just don’t want to accept it?

The much-anticipated Jackson Hole speech from the Fed Chair, rather than answering the question about monetary policy over the next decade, instead focused on the next few months. The financial markets have generally concluded that the Fed may announce a plan to taper its bond purchases as early as during its September meeting. However, the Fed, on its part, is sending out clear signals to the market that tapering of bond purchases does not presage an early increase in interest rates.

With the US employment report due out this week, there will be an early test of the Fed’s resolve to keep the market from discounting a rate rise. The market expects another set of encouraging numbers on the employment front, with consensus forecasts of nonfarm payrolls of 750,000 and a two-tenths drop in the unemployment rate to 5.2%.

Interestingly, the last time the Fed raised interest rates from near zero was back in December 2015 when the unemployment rate was 5.1%. The Fed then stayed with just the one rate rise for nearly 12 months as the unemployment rate remained stubbornly perched at the 5.1% level. With a broader reopening of the US economy, particularly the services sector, still a good measure away, we should expect a further fall in the rate of unemployment in coming weeks even if it is not at quite the pace of improvement seen in recent months.

Powell’s speech last week caused little fuss in the bond market. After the volatility of yields in July, August has seen less drama. The US 10-year government bond yield pushed to 1.31% after the speech, compared to the low of 1.17% at the start of the month. However, breakeven yields have not reacted in the same manner as their nominal counterparts. The 10-year breakeven rate is still around 2.38%, the midpoint of its recent range.

Credit markets cheered the dovish tone reiterated by Powell. In July, high yield credit spreads had drifted marginally higher while being generally well-behaved in a supportive scenario – none of this will likely change given the latest stance taken by the Fed. The US high yield CDS market tightened quite strongly to 275 basis points on Friday, from a high of 300 points earlier in the month. The market now has a dovish Fed to go with a low default experience and healthy institutional demand as supportive factors for credit for the rest of the year.

Not all equity markets globally had the chance to react to Powell’s statement on Friday; however, the good performance of the US equity markets likely sets us for further gains this week. Mr Powell’s relatively dovish statement and hopes that the recent surge in US COVID cases might be in abeyance helped the share prices of companies seen as the reopening trades. Las Vegas stalwarts Caesars Entertainment and Las Vegas Sands were up 16% and 10%, respectively, reversing the previous week’s share price weakness. Las Vegas Sands is still down a third from the levels of March. At a broader level, the Nasdaq led Friday’s rally, rising 2.8%.

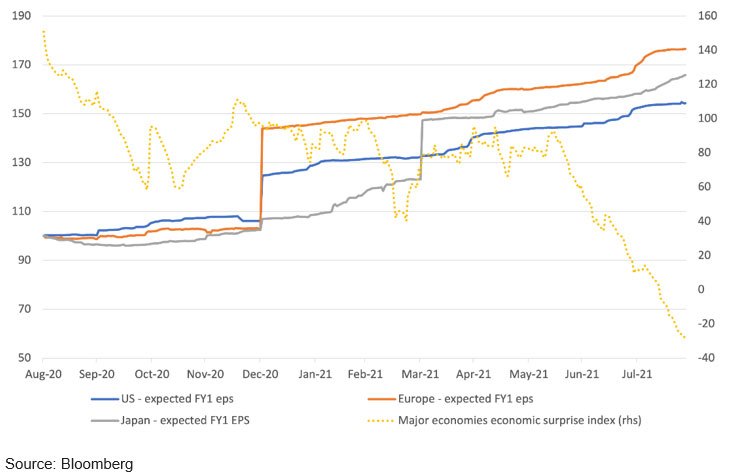

Chart 1: Europe and Japan lead the United States in recent upgrades to earnings forecasts against the backdrop of a drop in economic surprises

However, while monetary policy remains very accommodative, economists continue to trim their growth forecasts. A lack of growth momentum could provide something of a headwind to equities if it translates into material downgrades to corporate profits forecasts. At least for the moment, this seems to be affecting the US more than either Europe or Japan.

In the United States, analysts’ corporate profits forecasts have been static over the past six weeks (Chart 1). On the contrary, for both Japan and Europe, analysts continue to upgrade their corporate profit forecasts. The upgrades to Japanese analysts’ earnings forecasts have been quite marked and probably explain why Japanese equities have finally shown some outperformance against global benchmarks. We retain our constructive views on both the Japanese and European equity markets.

The spread of the delta variant continues to make policymakers hesitant about a broader reopening of their respective economies. The delta variant has proved stubbornly more infectious and has caused more hospitalisations. Research published this past weekend in the medical journal Lancet shows that those suffering from the delta variant were approximately twice as likely to need hospitalisation. That said, 75% of those that caught the virus were unvaccinated. The study analysed more than 40,000 positive cases in the UK between 29 March and 23 May. Nevertheless, around 64% of the UK population is fully vaccinated and rates of vaccinations have accelerated around the world. In the US, there is a contrast between younger people needing hospital treatment at the highest rate on record while hospitalisations among seniors have dropped.

The intriguing mix of advice from the medical profession continues to make politicians hesitant to fully reopen. Canada is facing its ‘fourth wave’ with some experts suggesting this could be the biggest yet. Clearly, we are still a long way from normal.