Dec 9, 2021

Only since a few days was the world collectively heaving a sigh of relief and anticipating a return to normalcy after Delta cases receded and vaccinations/boosters shot count climbed. The newly identified Omicron variant has set anxiety levels soaring back again as initial reports suggest it is highly transmissible.

The high transmissibility was somewhat extrapolated to assume high severity as well and triggered a global reaction in various ways including travel bans, calls for reassessing vaccine efficacy, debates around further lockdowns, equity market sell-off, renewed supply chain disruption fears etc.

Further news and data that has trickled in, for now, suggest that the earlier reaction arguably may be exaggerated. The higher transmissibility is validated by scientists, but the magnitude of severity is being debated. With more evidence emerging the severity could be lesser than expected earlier. The see-sawing of emotions, reactions and measures will continue until there is more data that drives a definitive conclusion.

Overall, as per current data – assuming a base case of high transmissibility but low severity, our key concern area as echoed by several others is the supply chain disruption. China the world’s manufacturing hub with over a one-third share in global manufacturing output continues to follow a zero-tolerance policy in their handling of covid. Also, the labour force may resist a return to work, especially in the high contact services sectors. Therefore, while most of the world may resist lockdowns, some adverse impact on supply chains is expected. This could further exacerbate the issue of inflation. Over the next few months, favourable base effects will kick in and inflation may look softer, but Omicron related uncertainty will persist.

The U.S. Fed Chair Jerome Powell in a considerable shift of stance said that he believed high inflation would persist until the middle of the next year and so the Fed is “likely” to discuss speeding up the tapering of its asset-buying programme. In October, U.S. consumer price inflation rose at its fastest pace in 30 years.

US inflation at 30-year high

An otherwise reticent Europe also appears to be concerned about inflationary pressures. Germany, considered to be a highly inflation-sensitive country, last month recorded the highest inflation since 1992.

In sharp contrast to Powell’s hawkish stance, China cut banks’ reserve ratio by 50 bps effective Dec 15, 2021. China growth has been slowing down as the deleveraging continues.

India

India’s real gross domestic product (GDP) growth came in higher than consensus at 8.4% in Q2FY2 supported by a low base. Also, the reopening of the services sector aided overall growth. Exports crossed the USD 30 billion mark for the eighth consecutive month. As growth conditions normalized imports outpaced exports in the quarter. GST collections continue to be robust and clocked the second highest monthly collections ever in November 2021

GST Collection Trends (INR Crores)

Over the next few quarters, economic growth numbers could appear muted as base effects wear off. There are some Omicron related downside risks as well.

Most of the companies in their last earnings update have highlighted that the current commodity inflation across products is the sharpest they have witnessed in decades. Industry leaders with strong balance sheets have been able to weather the impact better than small/unorganized players. We observe that certain consumer category leaders have passed on the price hikes in a calibrated manner to limit adverse impact on demand. A combination of higher inventory and calibrated price hikes may help industry leaders protect margins better than the smaller players. Reflecting the volatility in the price of several commodities, shipping rates and the Omicron related potential supply-chain issues the gross margins for the next couple of quarters could be volatile.

The Omicron outbreak, strengthening dollar and US Fed Powell’s hawkish statement triggered an equity sell off in the month of November.

Correction from recent peak

FPIs turned net sellers for the second consecutive month. However, the net outflow of USD 2.71 billion in November 2021 needs to be balanced against the Primary investments of USD 3.64 billion. On a cumulative basis FII flow for this financial year (Secondary + Primary) stands at USD 2.34 bn.

Conclusion

In addition to describing our view, we also use this medium to share the things we are watching out for. These are data points, trends, issues that could create risks/opportunities in portfolios. Our objective is to catch these early and continuously weigh the probability of them playing out.

One such issue we currently see is the flattening of the US yield curve and the inversion in the long-term segment of the yield curve. Inversion of the yield curve is often an early indicator of an economic slowdown. Of course, the keyword here is ‘often’, which is not the same as always. US markets hugely influence the flow of money around the world, and hence the yield movement needs to be monitored, early as it may be.

At this point, we would like to take a slightly long-range view of Indian equities. We have gone through a decade of reforms that included a deleveraging cycle, cleaning and strengthening of the banking system (and by extension credit ecosystem), insolvency addressal, real estate regulations, tax reforms (GST and lowering of corporate taxes), social security, support for domestic manufacturing and many more. Covid also forced companies to get leaner and more efficient. The overall wealth effect and specifically job creation traction has put higher spending ability in the hands of the household. All this primes us up for virtuous growth upcycle.

We would want to maintain our focus on the long-term potential (higher trend growth) rather than getting distracted by the short-term noise/pain (inflation and the US interest rate cycle). We, therefore, reiterate that we prefer to stay put in equities through a correction if that were to happen and potentially add more. It is entirely likely that when we add to equities, negative news flow could be very high, and we may end up looking wrong in the short term. But we choose to live the clichés of the investing world – Stay invested, think long term. We sign off with an interesting quote we read: Market tops are made amidst volatility and market bottoms get created silently.

Technical Commentary

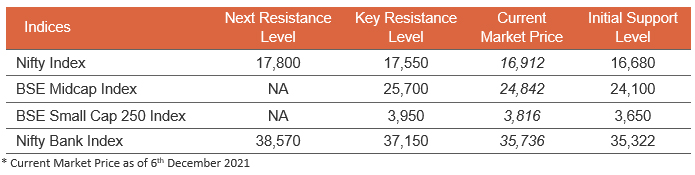

From the all-time high of 18,604, Nifty has corrected 10% in 6 weeks. The key level of 61.8% Fibonacci retracement of the rally from 15,515 to 18,604 is at around 16,695. Also, the target of bearish head and shoulders pattern over the Sep-Nov 2021 period is at 16,680 levels. Thus, 16,680 is a key support level for the Nifty. The Nifty index is likely to see sideways action between 16,700-17,550 levels before it sees a directional move. A break below the 16,680 level could suggest a move towards 16,175. While on the upside a break above 17,550 could indicate a move towards 17,800.

The Bank Nifty saw a steeper fall compared to Nifty. The Bank Nifty Index is now facing resistance at 37,150, a break above this could suggest a move towards 38,570 levels. On the downside recent low of 35,322 will act as a support, a break below could suggest a decline towards 34,000 levels. The BSE Midcap is expected to consolidate between 24,100 and 25,700 while the BSE Small cap 250 is likely to trade in a broad range of 3,650-3,950.