Mar 23, 2021

• The Fed sees growth but no lasting inflation

• The market is pricing a return to pre-GFC inflation of 2.25%

• Bond yields are set to rise and pose a quandary for investors facing low yields and high rate risk

• Old-fashioned dividend stocks offer a way out

• They offer higher income, growth upside and inflation protection

The Fed goes for the extreme dovish stance: To the concern of equity markets globally, Fed Chair Powell was clear in his message after this week’s Fed policy meeting that there was no prospect of rate hikes this year because it saw no clear inflation risk. For 2022 and 2023, the message was much the same. The Fed would want to see very clear signals of full economic recovery and persistent inflation pressure before policy will be tightened. There was no hint that tapering would be considered any time soon: expect to see purchases of fixed income securities to maintain a pace of $120 billion per month for the foreseeable future. Equity markets were mixed after a positive response initially, with the tech sector under pressure and the VIX index jumping back above 20 after a brief dip below.

The Fed’s inflation outlook is benign, but the economic outlook is bullish: While the stance is very dovish, the economic forecast that the Fed is using is no longer gloomy. It sees the unemployment rate dropping to 4.5% by the end of this year and 3.9% by December next year. Such an outcome would signal success in the intervention policy of the US government. The Fed still views inflation as under control. One measure of inflation, the PCE deflator, is forecast to only rise to 2.1% in 2022. For this reason, the coming jump in inflation to 3% or higher is viewed by the Fed as transitory.

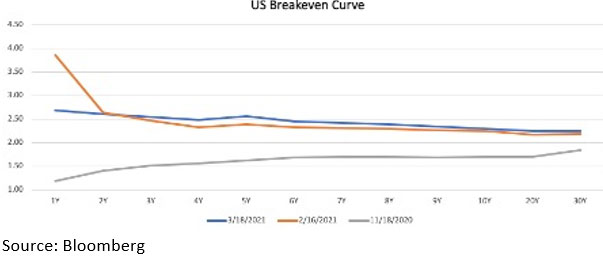

Chart 1

The market is pricing higher inflation: Chart 1 plots the recent development of the market’s view of inflation in the form of the US 10Y breakeven rate. After the sharp spike in February, it is still inverted showing a spike in the 1Y and 2Y, but a decline after that to about 2.25%.

Bond investors face a conundrum: As inflation returns and the economy gradually delivers the evidence of healing that the Fed is looking for before beginning to taper bond purchases and possibly tightening policy, bond yields look set to rise. There is currently a record surge in new issuance going on in the US HY bond market, as issuers rush to get new paper into the market before liquidity conditions tighten and outright yields rise – as they have, as expected, after the Fed statement. So far in 2021, $127 billion in new HY debt has been issued. Bloomberg reports that only a further $12 billion is needed before the end of the month to hit the all-time record.

The conditions for a drift upwards in the 10Y from 1.7% upwards beyond 2% looks unavoidable. While credit spreads have been better behaved than government bond yields, the risk of loss from higher base yields is now substantial. These warnings have been issued. Where does an investor turn for income without undue exposure to rising rates?

There are several reasons to consider high-dividend equities as a long-term replacement for low-yielding bonds: The first and most obvious reason is that there is a burgeoning universe of equities that pay higher dividends than is available in the corporate bond market for issuers of similar quality. Looking across a range of bond indices reveals the paucity of yields on offer. For global EM debt, the average yield on offer ranges from 3.5% in hard currency to 3.9% for local currency. US HY is a bit higher but barely above 5%. With yield curves steepening across the board, a low-duration exposure will offer lower yields still – closer to the 2% to 3% range. By contrast, it is not very challenging to put together a global portfolio of stocks with relatively predictable dividends of between 3.5% to 4%.

Patience will be rewarded: The second reason for considering this strategy is the effect of time on the portfolio. Many of the sectors that have been out of favour of late that pay good dividends have lower volatility characteristics (energy sector, some consumer plays) than growth stocks. If the investor has a longer time horizon and can ride out the potential variability of the equity market, the reward will be potentially better returns than a bond portfolio held for the same period (five years or more), as a generally positive environment for stocks plays to the investor’s advantage.

A better inflation play than bonds: The third appeal of the strategy is that it plays directly into the upside of the growth and inflation narrative. In the materials and mining sector, for example, a surging global economy will not only entrench the security of the dividend stream but also feed into the upside for the selected portfolio of equities. Other sectors, such as retail and consumer-spending orientated names, will have the opportunity to directly benefit from pricing pressure in the system by passing on price increases to end consumers. Again, that will fortify the dividend cover available and provide upside to the companies’ share prices.