Jul 6, 2020

As the first half of 2020 came to a close, it felt like a cliff hanger of a television series season. Escalating covid cases, continuing equity market strength, tense geopolitical equations, no-deal Brexit, brr of the printing presses – the interplay of events and response have been dizzying. Even while we come to terms with a changed world, we await anxiously for the next half and as die-hard optimists, hope for a happy ending.

Quarterly Asset Allocation Pairs Update

Every quarter we use our asset pairs methodology as a key input in formulation of our investment strategy views across asset classes. We understand that the current economic data might not be a true reflection of what is to come given economic activity was disrupted as India and larger part of the world have been in some form of a lockdown for past few months. However, we did the exercise to get some sense of what the data is telling us.

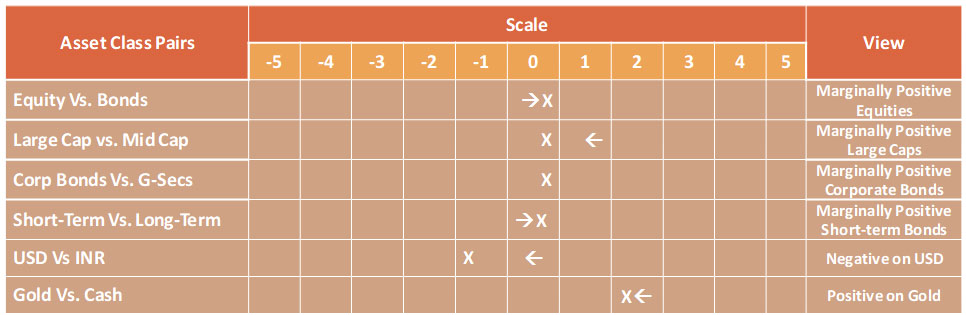

Equities Vs. Bonds

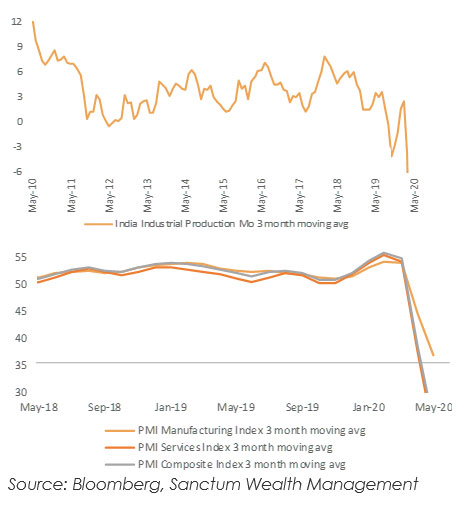

Economic disruption to impact equities

High frequency economic data for the period under lockdown has started coming in. As expected, numbers are grim. Industrial production, PMI, auto sales have all fallen off the cliff. Economic disruption is negative for equities as it impacts profitability while it can be positive for bonds as yields could remain lower.

Macroeconomic data has been grim as expected

Relative valuation in favour of equities, but earnings a question mark

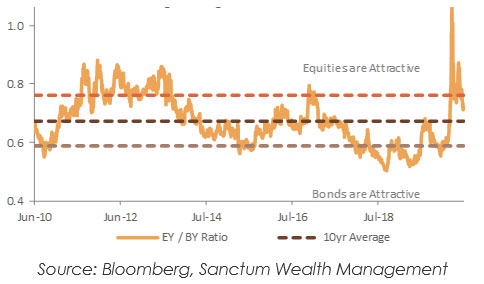

Over the past quarter bond yields have declined sharply, while price correction took place in Indian equities as well, relative to bond yields equity valuations (earnings yield) seems more attractive. However, it is important to note corporate profitability could take a hit as the results of quarter ending June 2020 will reflect the full impact of the lockdown. This could impact equity valuations adversely.

Equities looking relatively attractive Vs. bonds

Domestic flows have offset foreign outflows in equities

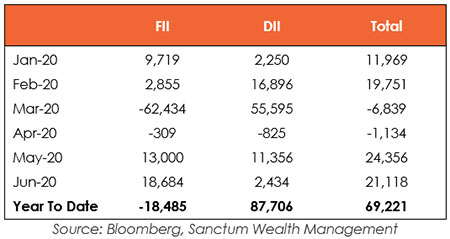

As cases started to pile up and markets began correcting, foreign institutional investors (FIIs) exited Indian equities in a big way in March 2020. Over the last two month they have turned buyers again, but year to date they remain net sellers. On the other hand, domestic institutional investors have remained net buyers through most part of the year. Given, limited avenues for returns locally, domestic flows could continue to remain robust, supporting equities.

Net Equity flows (INR Crores)

Asset pair methodology marginally in favour of equities

While valuations and flows seem to be in favour of equities, economic disruption and uncertainty of corporate earnings are against equities. Technical trends favour equity despite the rally being a bear market correction rather than a bull run. In balance, we have moved to neutral equities from the previously underweight position but continue to exercise abundant caution.

Large Cap Vs. Midcaps

Marginally in favour of large caps

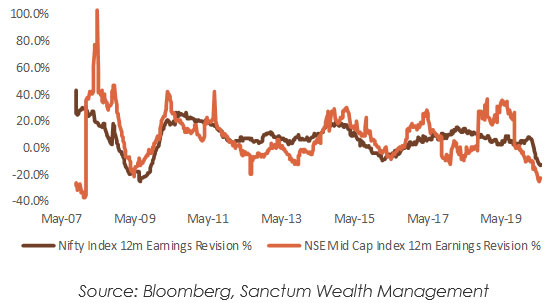

Recent market correction has led to contraction in valuations for both large caps and midcaps in equal proportions. However, midcaps have seen sharper earnings downgrades. Several midcaps companies might not have seen enough economic cycles. The segment also tends to have lesser ammunition – cash, capital in balance sheet, ability to raise money – to withstand current economic dislocation. Our asset pair score continues to remain in favour of the large caps although to a much lesser extent relative to the previous quarter on account of valuations.

Earnings Revision

Corporate Bond vs Government Bonds

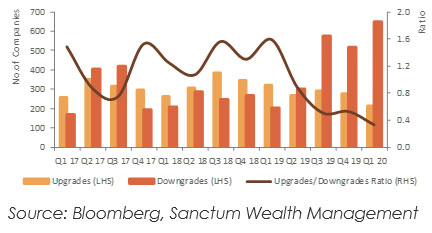

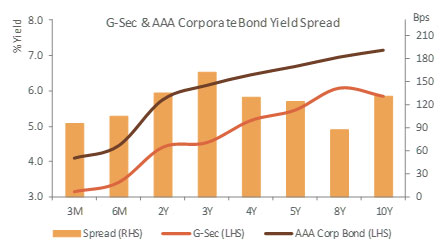

Marginally in favour of corporate bonds

Corporate bond spreads (difference between corporate bond and government bond yields) remains elevated when compared to history. This is positive to corporate bonds as there is scope for corporate yields to decline. However, as expected there has been higher number of ratings downgrades for corporates than upgrades in last few quarters. Hence, while corporates yields are attractive, we do not think it is time to search for yield beyond AAA – AA corporates. Our asset pair score is largely unchanged for this asset pair.

Credit Rating Upgrade/Downgrade Ratio attractive

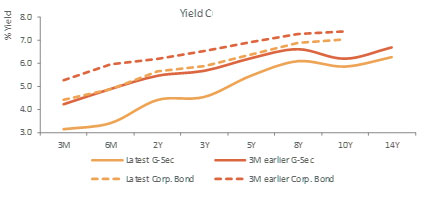

Corporate Bond yields

Short-term vs Long-term Bonds

Marginally in favour of Short-term bonds

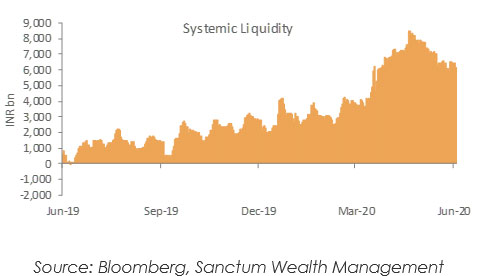

The RBI has provided ample liquidity over the past few months with rate cuts, increased open market operations, special liquidity windows etc. This has led to yields on short-term bonds decline sharply. The yield curve is pretty steep now, i.e. there is enough spread between short-term and long-term bonds. However, government borrowing is expected to increase as tax revenues fall amid lower corporate profitability. A large part of the borrowing might come from the long-term end of the yield curve causing long-term bond yields to rise. Hence despite the higher yield it would still be prudent to avoid taking too much duration in bond portfolios, in our view.

Short-term corporate spreads more attractive

Surplus liquidity in the system has increased

Gold vs Cash

Positive outlook for Gold

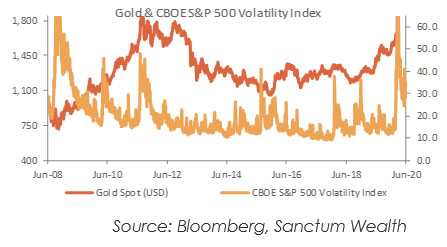

Gold has rallied sharply over the last one year as first US-China trade tensions and then the outbreak of Covid19 increased equity volatility. This led to rise in demand for safe haven assets likes gold. Given the sharp rally in gold, valuations relative to other commodities have turned unfavourable for gold. However, expanding US Fed balance sheet, still elevated economic volatility, rising gold ETF demand and technical trends are all in favour of gold. Hence, while the score on our asset pair methodology has decreased for gold, it still is significantly in favour of gold.

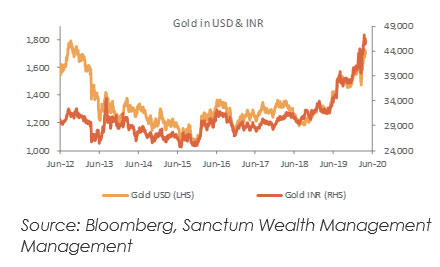

Gold in INR has seen a sharper rally

Elevated equity volatility positive for gold

USD vs INR

Positive outlook for INR

This is one asset pair that has seen significant change in score in our asset pair methodology. On the back of valuations, lower crude, forex reserves build-up as well as trend indicators, we now favour the rupee against USD

We have been advocates of international diversification for a few years now. To represent that view in our model asset allocation portfolios, we have now decided to include an allocation to international equities as well. To that effect we have added exposure ranging 3%-5% to our three risk profiles i.e. Sanctum Wealth Shield, Sanctum Wealth Enhancement and Sanctum Wealth Generation.

Summary of our asset model

Portfolio Update

Our flagship strategies – Sanctum Indian Olympians and Sanctum Indian Titans have distinct positioning but a common trait of buying into resilient businesses run by high quality management teams. Therefore, most of these businesses are expected to gain further market share gains in the longer term even if there are some setbacks in the current environment.

Traditionally both our strategies are buy and hold strategies with low churn. But in light of changing business environment, we chose to review our positions more actively. We hedged early on in Sanctum Indian Titans and increased cash in Olympians as risk escalation seemed imminent. We have since deployed most of the cash in businesses which are relatively resilient in these uncertain times while keeping the portfolio beta under check.

We anticipated that lending as a business would see headwinds as the economic disruption intensified and hence reduced exposure to the segment while increasing allocation to non-lending financials while maintaining the overall sector weight of financials in line with the benchmark. We also increased exposure to consumer staples and healthcare during the quarter. More recently we added Bharti Airtel as the telecom industry turned around the corner and is now expected to witness steep revenue growth over the next few years. We have been constructive on the rural theme and as a reflection of it, we added Hero Motocorp to Sanctum Indian Olympians considering its dominance in commuter segment of two wheelers especially in rural India.

| We have to practice defensive investing, since many of the outcomes are likely to go against us. It’s more important to ensure survival under negative outcomes than it is to guarantee maximum returns under favourable ones. |

| – Howard Marks |

Our thoughts echo the above quote. We exercised caution in our portfolios ever since the magnitude of the economic disruption became evident. The caution helped us significantly during the sharp sell of in March and cushioned us for future risk. The divergence between economic reality and equity markets continue to pose risks. We therefore put cash back to work only gradually, giving up some of the outperformance.

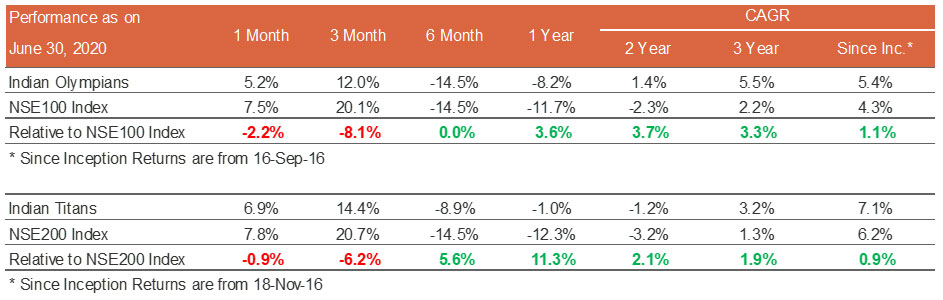

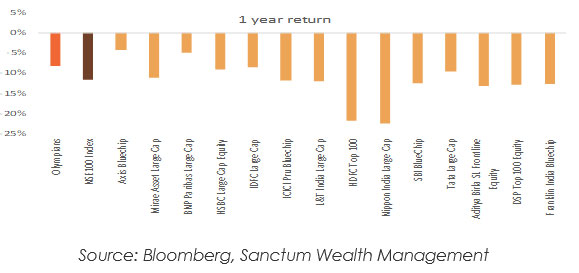

Reflecting on the past performance of our strategies, we have delivered outperformance not only relative to index but also to mutual fund peer set. Sanctum Indian Olympians continues to be a top quartile performer in the near term

Indian Olympians has been an outperformer in last 1 year

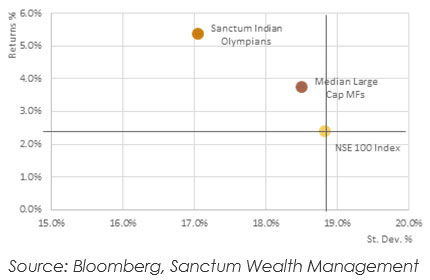

It has also delivered superior risk adjusted return

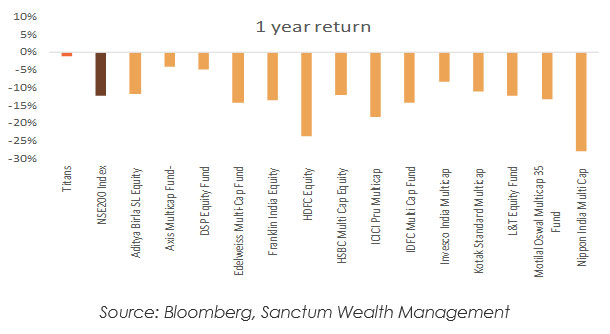

Sanctum Indian Titans was successful in protecting most of the downside resulting in being the top performer in its category for the past year.

Indian Titans is top performer in its category in last 1 year

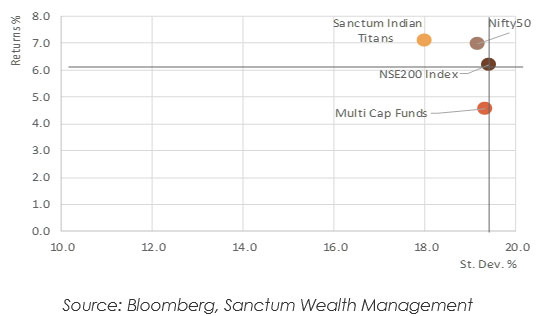

Titans delivered superior risk adjusted return too

Our third strategy, Sanctum Indian Smart Solutions after a rejig last year has joined the ranks of Sanctum Indian Titans and Sanctum Indian Olympians in delivering strong performance. We are not covering it this month for the sake of brevity, but intend to do so in our next note, watch this space.

Equity

Even though equity markets looked uncertain at several points in time in June, broader markets ended the month with large gains – Nifty with an impressive 8% gain; small caps, a segment almost written off in the minds of most investors, chalked up a 15% gain. But behind the giddy gains is a story to be heeded. A lot of the gains were on counters most quality conscious investors wouldn’t touch.

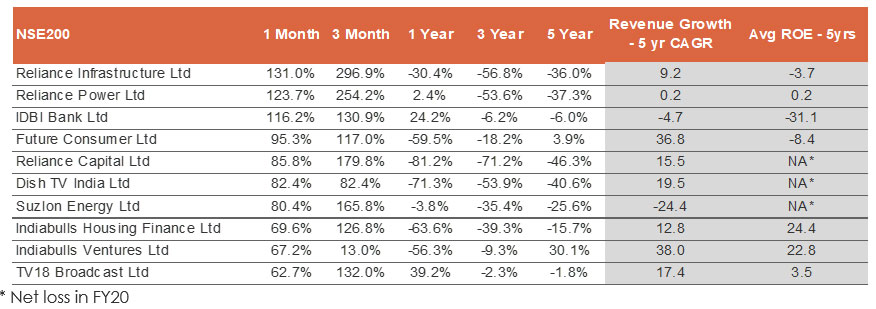

Best performing NSE200 stocks over last one month have weak fundamentals and have been wealth destroyers over long run

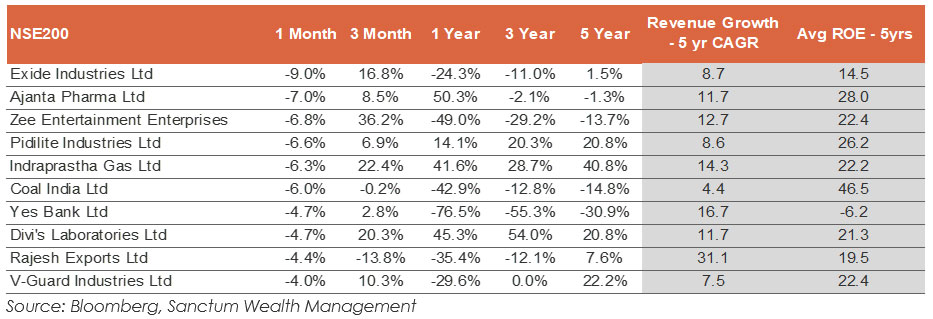

Many worst performing stocks over last 1 month are fundamentally strong businesses

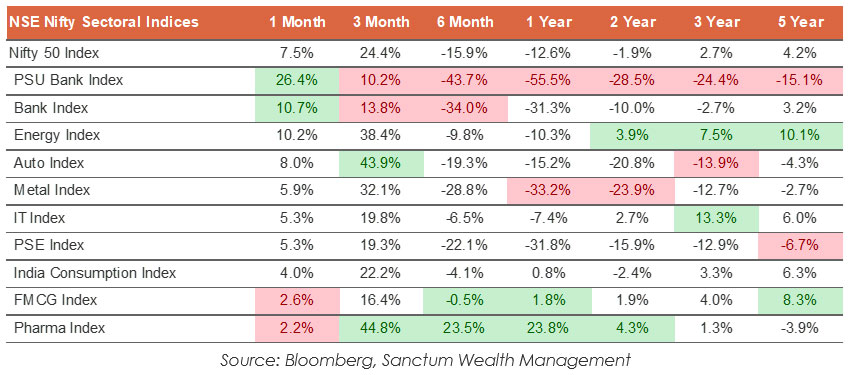

Nifty PSU Bank Index, the worst performing index across all other time periods, was the best performing Index over last one month. While, FMCG is the worst performing index over last one month which is one of the best performing index over last 5 years

Historically, we have seen that sub-par quality companies (with poor corporate governance, flaws in business models, inconsistent growth etc.) tend to fare well in spurts but when the tide turns, the damage is tremendous and many a times, irreversible. We will resolutely stay away from the space, even if costs us performance.

Technical trends:

In a though market, we saw profit booking when Nifty was at 10,550 levels on 24th June, it was immediately bought into and eventually market has hit new high for the rally. Nifty is forming high top and high bottom structure on daily charts since April low. Based on the key 61.8% Fibonacci level of the entire fall at 10,550 levels and rising resistance trend line at 10,660 odd levels, the 10,550-10,660 levels become an important resistance zone. If Nifty crosses above 10,660, we expect a rally towards 10900 where 200 day moving average is seen and then towards 11,100 levels. India VIX, a measure of volatility, was holding 28-29 levels in the month of June. But now it has broken below and is currently at 26.7 levels. This is positive for the market. VIX sustaining below 28 level could suggest that the market rally could continue.

On the downside, rising support trend line connecting low of 7,511-8,806 comes around 10,150 which will act as a support. Moving below 10,150 will also break the recent low of 10,194. Thus, a move below 10,150 could lead to a decline towards 9,800 initially and then 9,550.

Fixed Income

In our previous commentaries, we stated our preference for Corporate bond funds. We saw an opportunity for yield compression as a consequence of abundant liquidity and normalizing risk environment from extreme risk aversion in March 2020. The call has started playing out with the segment delivering upsized returns in the past month. We think there is more scope there. But it accompanies a word of caution. Whenever markets are flooded with excessive liquidity, moves tend to be front loaded – effectively windows of opportunity close quickly. Therefore, decision making has to be swift. By the time the opportunity is validated by some returns, the low hanging fruit is likely to have already been taken. Making large returns, therefore, need a leap of faith.