Nov 9, 2021

• Central banks turning upbeat on economy on belief inflation to prove less transitory than thought.

• Equities appear set to extend gains as central banks step away from tightening.

• Third-quarter results so far have been robust, although economic data remains mixed, and markets look for greater clarity from the Fed.

• Like some others, we believe inflation is stickier than the central banks would have us believe

• Those investors looking to buy better value in the equity market need to look towards Asia, REITs, infrastructure, and healthcare among global sectors.

We are back in a bull market. With central bankers backing off from materially tightening monetary policy even in the face of higher-than-expected inflation, the green light is back on for further gains in risk asset prices. Both equities and bonds rallied last week as major central banks stopped well short of signaling interest rate increases. The Global Aggregate bond Index rose 0.7% on the week; major equity markets gained at least 2%.

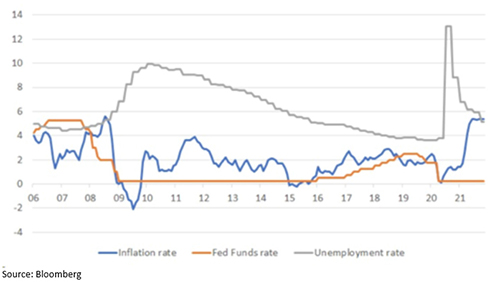

Last week, the Reserve Bank of Australia and the Bank of England stepped back from announcing interest rate increases, and the FOMC’s post-meeting commentary indicated any monetary tightening was still some distance away. Quite frankly, the outcomes of the meetings represented a collective bottling by central bankers who had previously indicated that the way to normalisation of monetary policy should start to accelerate. If we were to decode the central banks’ views from their meetings, it would appear they suspect inflation is proving to be less transitory than they previously thought, but they want to wait just a little longer for greater clarity.

In the case of the Federal Reserve, one would wonder what they want to see before they are comfortable endorsing any increase in interest rates in 2022. This week, the market projects the US consumer price inflation to have hit 5.9% in October, the highest since 1990; core inflation ex food and energy to be at 4.3% as against 4.0% in September. Last week’s employment data was much stronger than expected and incorporated revisions to earlier months’ data, which took away the softness that the Fed had previously alluded to as a reason to hold fire on tightening.

Chart 1: Unemployment and inflation yet to impress the Federal Reserve

Both equity and bond markets understandably took the cue from central bankers as a positive. The equity market rally probably has more legs to it. In most parts of the world, the corporate results season is delivering profits well ahead of expectations, and retail investors look fully committed to pushing the markets higher. Stretched valuations remain a minor constraint on how markets move. With interest rates remaining low, liquidity remains relatively plentiful, and the marginal investor is a buyer.

The equity markets are all about the here and now. Third-quarter corporate results so far have been robust in most parts of the world. About 76% of the companies in the US, 60% in Europe and 55% in Japan have beaten analysts’ 3Q earnings estimates. Oddly, the earnings beats have come despite the backdrop of ongoing downgrades to economists’ GDP forecasts and disappointments with economic data in most parts of the world.

The bond market reacted to the Fed’s statement as if it had melted away any residual inflation risk. The US 10Y Treasury ended the week at 1.45%, a 20bps drop in yield. The bond market’s pricing of inflation market also reacted, but not to the same extent. The 10-year breakeven rates dropped around 10bps in the week to imply an inflation rate of 2.55% after touching all-time highs the week before.

For now, the bond market is satisfied with the Fed’s explanation. It yielded just enough to imply it recognised the inflation situation as it seems to us to be developing, but without risking a full-blown bond tantrum by calling it a significant risk. However, the labour market did not support the view: For the previous two months, the labour market had been hamstrung by COVID. October was better and showed signs of the expected tightening that had been anticipated in the previous months. For a start, the overall pace of payroll growth for August and September was upgraded by 235,000, and October by another 531,000 compared with market estimates of 450,000.

We, like some others, believe that inflation poses more of a problem than the central banks want to discount. We worry that they are being overly cautious about tightening, leaving the risk that when they eventually must tighten, the tightening will come in a lumpy fashion that undermines the positive market sentiment.

Inflation has hit me where it hurts. My Starbucks here in Singapore, Grande Americano, went up 5.4%! Starbucks, like many in the food sector, has got its cost pressure problems. The coffee giant faces inflation in costs on many fronts; by summer 2022, it will have increased its average hourly wages by 21% to $17 from $14 an hour. Arabica coffee prices are at a five-year high and were recently up 60% year-to-date. Last week’s quarterly results disappointed the market and the stock initially plunged 7%. However the full week’s price movement in Starbucks summarises the current market mood. Despite the bad news, by Friday, the share price was higher on the week. Maybe ESG investors saw merit in the wage increase!

How do you safely move into markets when they have had such a strong run? While investors will understandably want to hold onto their core positions, any marginal investment should be directed to those parts of the market left well behind. Sectors to consider include value stocks, REITs and healthcare, with Asia and Brazil being the preferred regions. Asia is the trickiest, in our view. Few commentators have any conviction about China at present. To go back to my Starbucks story, Starbucks comparable store sales in China fell 7% in the third quarter. The China macro picture still looks very difficult. The market keeps expecting and hoping that the authorities will relent and implement a reflation programme.

We finish with one reflection: Barron’s, the US financial broadsheet, ends its article on How to play a market bubble (Ben Levison, November 3rd, 2021) with the words, “remember, it’s all a lot of fun until the music stops playing.”