Feb 15, 2021

• Equity markets rise as global corporate earnings reports handsomely beat expectations.

• US budget progress and an infrastructure and green budget to follow to keep markets vibrant.

• COVID news from Israel promotes hope for earlier normalisation.

• Better than expected US inflation data suppresses rise in US 10 year government bond yield

• High yield bond yields drop below 4%.

• Italy’s political challenges resolved – a catalyst for better eurozone equity performance?

Equities continue to grind higher with seeming few significant near-term challenges. The global equity index rose a further 1% last week and stands +5% for the year-to-date. We believe that the only thing that may upset the current party mood in equity markets is if US long-term interest rates move up markedly from current levels, which would indicate a tightening of monetary conditions. Valuations of equity markets are unnaturally high and can only be supported by plentiful liquidity and ongoing policy support for global growth.

Corporate earnings reports continued to surprise to the upside. With 74% of the S&P 500 reports said 80% of companies had beaten estimates. The size of the surprises at 15.1% is the third-highest level in more than a decade. The positive surprises are also evident in other markets. In Europe, 69% of companies have beaten expectations, and in Japan, 66% of companies have exceeded expectations. The earnings beat has been across most sectors, excluding airlines and hospitality.

Although equity market valuations look stretched, the likely ongoing announcement of US spending plans will keep investors engaged and equities moving higher.

Although the US Senate has been side-lined in the past week with the Trump impeachment, we expect to see more news in the coming days of the pace for approval for Biden’s budget. Current thinking is that the Senate will approve the stimulus plan by March, allowing for the household cheques to clear before the end of the quarter.

Remember we are also awaiting details of President Biden’s infrastructure and green bill. Some commentators have suggested that the bill could be voted into law by the end of July. At the moment the Democrats are pushing a campaign ‘Build by the Fourth of July (BBJ4)’. Topline spending could be of the order of $2 trillion at the federal level although President Biden expects there to be a good measure of private sector investment along-side the state.

Israeli COVID vaccination data gives grounds for hope.

The rollout of vaccinations and efficacy of the vaccinations remains an essential input into an investment strategy. A wholehearted shift into value stocks, commodity plays, and consumer discretionary stocks require a good measure of investor confidence that the COVID situation is under better control. In that vein, Israeli COVID vaccination data shows there is some room for optimism that things could better a little quicker than previously better. According to a study by Maccabi Healthcare Services of 523,000 people who received both doses of the Pfizer coronavirus vaccine, there have been zero subsequent deaths and only four severe cases. Israel has administered 69.46 doses per 100 people.

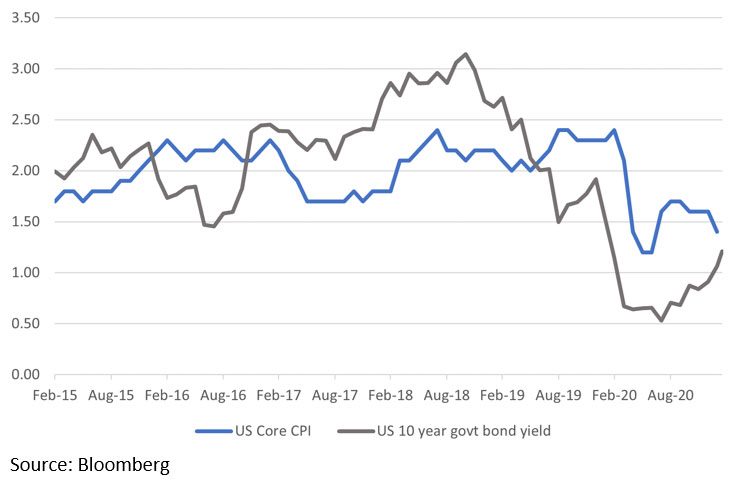

A drifting higher of US 10-year yield as inflation remained well behaved

The drift in treasury yields continues. Last week, the 10-year yield rose a further five basis points to reach 1.20%. This is despite the Fed buying $120 billion of Treasuries and MBS securities every month. Duration exposure looks to be a hazardous one to be taking right now, despite its evident qualities as a risk hedge and safe haven in crisis times.

Analysts didn’t find any more emphatic support for a more emphatic push higher in yields, at least in the near term. January’s US consumer price inflation number showed distinct softness at the core, which remained flat month-on-month at 1.4% year-on-year. Headline payrolls were also weak. The previous number of a 95,000 drop was revised to an even worse 204,000 decline.

Chart 1: Subdued US inflation to cap the near term rise in US 10-year government bond yield

Two factors underscore the market’s increasingly relaxed attitude to risk : a steady decline in the VIX index, and the slow but steady decline in high yield bond spreads. For the first time since February 2020, the VIX Index of equity options volatility dropped below 20. The significance could be that it is indicative that investors are not paying up as much as before for protection.

High yield no longer high yielding

USD High yield bonds made news because the outright yield on some of the main benchmark indices dropped to all-time low levels, below 4%. The spread to government bonds is still marginally higher than at some other points in history, but there is a slow grind lower underway. Aside from the obvious, namely that the relentless hunt for yield continues unabated, default rates in high yield bonds are predicted to be much lower by the end of the year. Year to date it is one of the few bond markets to give a positive return; the carry of a higher yield has provided protection from the rise in government bond yields.

Moody’s Investor Services reports that the trailing default rate in high yield for December 2020 was 8.3%, up from 4.3% for the previous December. However, on a forward-looking basis, the expected level of defaults is likely to decline going forwards, and this is being priced into the market. The actual level could drop below 4%. The outlook for this asset class hinges to an equal extent on further spread tightening, coupled with developments in the treasury market. The credit market has taken comfort in the view that further (significant) moves higher in government bond yields pose a minor threat.

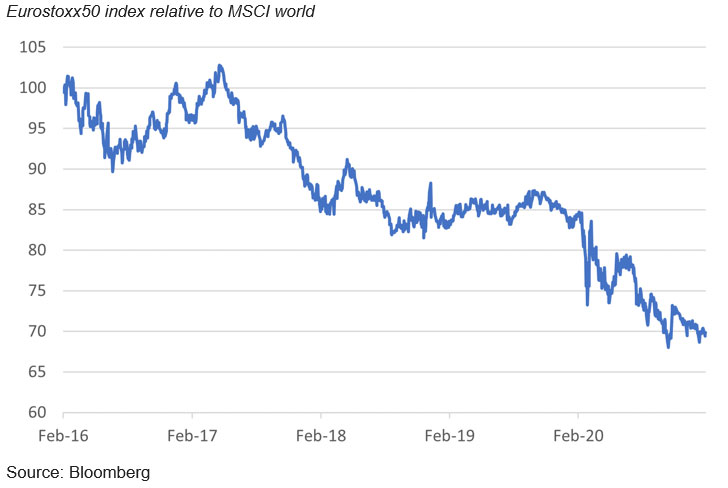

Italy – emerging from dark days

It is an open question whether the emergence of Italy from its dark days can act as a catalyst for some better performance from the eurozone equity markets. Over 12 months the eurostoxx50 index is still down around 4%against the global index up 16%.

Chart 2: Eurozone equities’ poor relative performance versus global equities

It is often forgotten that Italy’s economy is the world’s eighth largest economy. After yet another all-too familiar crisi al buio (crisis in the dark), former ECB President Mario Draghi was on Saturday appointed as Italy’s Prime Minister. He will head Italy’s third technocratic government of the last thirty years yet one that has garnered a remarkable amount of support including from the formerly eurosceptic Lega Party.

Assembly elections are due in Italy in 2023 but are more likely to happen in the summer of 2022. Mr. Draghi confronts both an enormous challenge and a blessing. The context is an Italian economy that contracted by almost 9% last year – one of the biggest in eurozone and an unemployment crisis that is disguised by a legal ban on lay-offs due to expire in the spring. There are challenges for the new administration right across the socio-economic spectrum – post-pandemic health reform, education needs especially for those affected by the lockdown, significant judicial and regulatory improvements and of course environmental targets. The new cabinet draws on an array of talents that will be sorely needed. The jewel or blessing is a €200 bn share of the EU Recovery Fund’s grants and loans to be spent over the next 3 years but coming with a series of strings (some unpopular) attached. As with President Biden, “Super’ Mario will need to move fast while his honeymoon in Rome lasts if the big offshore investor move to back Italian debt is to be vindicated.