Jan 25, 2021

• COVID cases continue to climb but market focused on President Biden’s promises.

• Asian data shows strong exports led principally by manufacturing.

• Emerging market debt challenged but still able to perform.

• Vietnam awaiting political news and primed for further performance.

• Corporate results season expected to beat expectations.

• Nothing expected from Fed meeting – market waiting for Yellen and Powell.

Investors continue to be pulled in two opposite directions. The current global COVID situation warrants caution, while Biden’s emergency recovery plan continues to encourage risk taking.

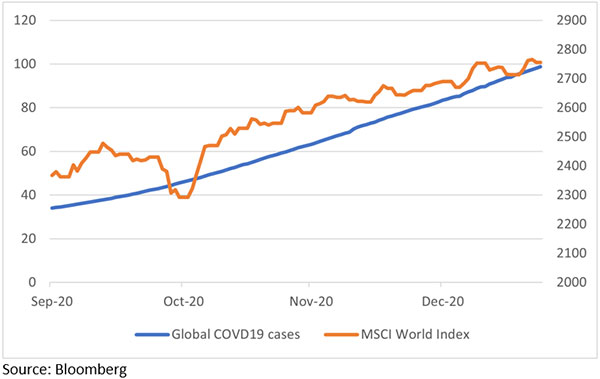

The current aggressive COVID19 infection rates and likely impact on growth have at least put a question mark in investors’ minds about the pace of the risk markets’ advance. While the vaccine rollout is picking up a pace in many parts of the world, the idea of ‘normal life’ still seems some quarters away. Vaccines that need two doses are often being spread out with a significant time delay. Also, the vaccines may take up to 12 weeks after the second injection to become fully effective. Hence it isn’t easy to see the world getting back to normal before the end of the year. It is also an open question as to how long the vaccines will provide immunity.

Chart 1: Equities continue to follow COVID cases higher

In the past week, there have been COVID scares in China. Japan is in state of emergency that looks likely to be extended by the government beyond the February deadline. President Biden’s initial message to the US population re COVID was very sobering for a country that had stayed so open. In the Middle East, the UAE has had to tighten restrictions after a significant spike in cases despite the impressive rollout of vaccinations. In Brazil, difficulties in sourcing and manufacturing vaccines have pushed out the vaccination programme’s likely completion to 2022.

The lockdowns are starting to test the pace of global consumer spending growth. While households have learnt how to spend money during a locked down, the recent lockdowns are undoubtedly stalling consumer spending. Looking at some of the higher-frequency data globally (which would include indicators such as public transport use, footfall in shopping malls and the like) reveals one pattern. While spending is holding up better than in the first series of lockdowns, there is weakness, nonetheless.

Asian economic data still please the eye.

Despite the global challenges Asian economic data has remained positive. However, like the rest of the world, there is a contrast between the manufacturing sector’s vibrancy and the service sector’s slackness. China’s fourth-quarter GDP data beat expectations at 6.5% year-on-year. Exports and manufacturing sectors were ahead of expectations, but domestic demand from consumption and investment were below expectations.

The firm exports theme was evident in Japan, Korea and Singapore. Japan registered Q4 real export growth of 61.4% quarter-on-quarter. The contrast between a vibrant manufacturing sector and the weakness of the service sector dragged down by weak consumer demand was evident in the Japanese industrial confidence survey where manufacturing sector confidence improved from -7 to -1, but the service sector deteriorated to -11 from -7.

In Korea, the flash report for exports for the first 20 days of the year points to a 15% year-on-year growth in exports, well ahead of expectations. In Singapore, exports were up 7.8% month-on-month significantly ahead of expectations.

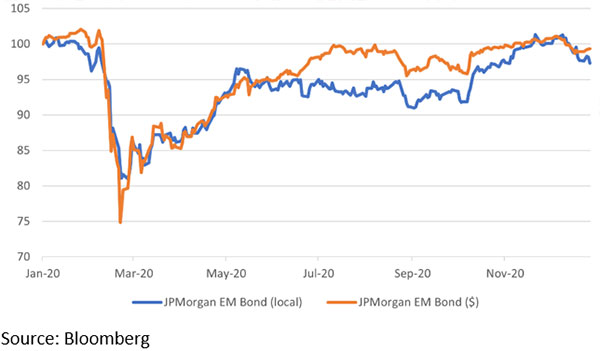

Emerging market debt challenged but still able to perform.

Emerging market bonds like other risk assets have rallied since the low in March 2020-. Local currency debt has returned 17% from the low; USD-debt is up by 21% – both as measured by the Bloomberg-Barclays Indices. Some of the rally is due to the drop in US Treasury yields and some to spread compression. Substantial further spread compression from the current base is difficult to see.

Both local and hard currency debt now yields in the 3.25% to 3.75% range, down from the yield highs above 8%. The EM USD Index’s spread to US treasury is very tight at 281 basis points, compared to above 300 in February 2020.

The hesitation in the performance of emerging market debt is partly a reflection of a few EM central banks starting to back off from their very easy policies. The Brazilian COPOM kept its interest rate unchanged last week but removed forward guidance implying that the risks of an earlier rate increase have built. In Turkey, the central bank remained on hold but stated that they would keep monetary policy tight for some time to come.

Chart 2: Emerging market bonds struggle for performance

One exception to the tighter policy trend was the Reserve Bank of India that indicated last week that they believe there is more room for easing. Some economists are penciling in a cut in interest rates at the April meeting.

One factor still possibly supporting local currency debt is the possible further weakness of the US dollar. A weaker dollar will enhance investors’ returns, as it implies the complex of local currency paper is delivering some performance. With weaker near-term global growth, the direction of travel for emerging market policy could be for further easing or stable rates for the first half of 2021. Inflation readings have been higher but driven by some very narrow increases in selected markets, where the pressure has already been easing (for example, food prices in India).

Vietnam – awaiting political decisions.

One of the market stars in recent months has been the Vietnam equity market. After a lacklustre performance in the early part of the year, the equity market suddenly took off. Investors appear to be rewarding the country for a brilliant COVID response and a positive view of the structural features that are looking to confer an edge to the country, relative to the other EMs. Growth in 2020 was one of the best at 2.9% year-on-year. The government expects a 6.4% growth rate in 2021. However, investors should always be aware of both upside and downside risks. The Vietnam ruling communist party holds its first national congress since 2016 this coming week. On the agenda is the choice of new leaders and the shape of new policies for the next five years. Such events can bring challenges. Should everything go smoothly, the Vietnamese market could be set for further gains.

Chart 3: Vietnam’s marked outperformance

Corporate results season brings limited challenges for markets.

The global equity markets may be torn between what may turn out to be a constructive fourth quarter 2020 corporate results season and challenging trading conditions in early 2021. Analysts already marked fourth-quarter earnings to relatively low figures. The consensus amongst analysts is that corporate profits will fall 10% in the US, and a fall 25% in Europe. Given that industrial confidence and macroeconomic data, in general, was relatively upbeat in the fourth quarter, corporate results could surprise to the upside.

No fireworks expected from the Fed meeting.

The Fed meets this week with little change expected in the statement. Do note that we also see the Fed’s preferred measure of inflation the PCE inflation due for release. The market expects a headline of just 1.2% with core inflation of 1.3%. We will have to wait for some weeks yet before seeing the dynamics of the relationship ex-Fed, Treasury secretary-elect Janet Yellen and Fed Chair Powell.