MARKING THE HEADLINES

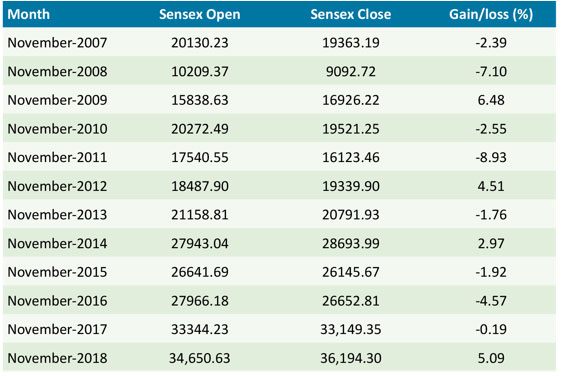

Nervous November? Sensex Closed In Red For 8 Out Of 12 Years

The Finapolis, Nov 13, 2019

With the Indian stock market touching new highs both through BSE Sensex and NSE Nifty, November may turn out to be a crucial month for index watchers. Historically, this month has changed its nature over the last many years. During 1999-2006, the November month saw hectic activity with the BSE Sensex jumping by 3-11 per cent every year. After the Global Financial Crisis (GFC), November has been a nervous time for markets. With markets at all-time highs in 2019 November, market participants may use the opportunity to book profits. Or, the opposite could happen where markets find a new ray of hope in November and steam ahead. Let us find out what will drive markets this month.

Instant triggers

India’s services PMI fell to 49.2 in October 2019 vs. 48.7 in September 2019. The slower pace of reduction was led by an increase in new export orders. “However, domestic demand remains muted, with competitive pressures and higher input prices building stress on profit margins. Employment growth too remains subdued. The 12-month outlook fell to its 14-year low in October 2019,” says Sameer Narang, Chief Economist at Bank of Baroda (BoB), in a report.

With the macroeconomic signals showing distress signals, more cues will be provided by CPI (Consumer Price Index), Wholesale Price Index (WPI) and Index of Industrial Production (IIP). The weak core sector data, Core sector industrial production in the country declined by a whopping 5.2 per cent in September 2019, has already set the stage for poor IIP number because these core sectors have heavy weight in the IIP.

“We remain watchful of global and domestic economic data. Over August and September, the economic data has taken a decided turn for the worse, both domestically and globally. However, our views on the market are forward looking by design,” says Sunil Sharma, Chief Investment Officer, Sanctum Wealth Management.

Quality comes at a price

Markey participants have argued recently that though quality growth stocks are doing well, they are now trading at very expensive valuations. Quality growth has rewarded investors handsomely. However, often quality growth companies coming with a tag of price-earnings multiples of 70-100 times. “Time will tell if we are in a new era on valuation. For now, the market remains comfortable with high valuations, and so are we,” Sharma said.

Portfolio managers have been shuffling their picks to be best positioned for November. For instance, Emkay Alpha Portfolio has seen key changes. “Due to our change in views related to stress in the telecom sector (in particular, Vodafone-Idea Ltd, report link), we include Bharti Airtel and Grasim Industries (replacing Ultratech) into the EAP-Nifty. We also bring in Tata Motors (the recent upgrade after a turnaround visible in JLR, report link), Jubilant Foodworks (replacing Berger Paints after a sharp rise in stock price). We also make the sector exposures more concentrated: 1) in Pharma by removing Divi’s (only Cipla remains now); and 2) in Banks by removing Kotak Mahindra Bank,” Emkay said.

In October, Sensex rose by 3.5 per cent. Nirmal Bang Retail Research is of the view that the momentum created in October is likely to sustain in November series and it expects market may see new high in current series. “Nifty range in November Series is likely to be 11,700-12,200,” it projected.

Earnings recovery in sight

Equity earnings yield came as close as attractive to bond yields post corporate tax cuts but not materially enough to offset macro concerns. “About 65 per cent companies reported positive and in line results for Q2FY20 so far vs. 51 per cent in Q1FY20. Financial, Industrial and Material sectors have done well. Relative valuations continue to favour Mid-caps over Large-caps,” says Validus Wealth Managers Private Limited. Liquidity flows are now in favour of Mid-caps and actual Q2FY20 results show Mid-caps have done better. But, earnings downgrades have been worse than Large-caps though both yielding CAGR of nearly 29 per cent on a 2-year forward basis, it said.

However, one thing has become clear for stock market participants. The Diwali consumption boost has not played out in the way markets expected. October being full of festive season with Navratri, Dusshera and Diwali all falling in the same month, the revival in demand is creating some doubt about sustainability for November.

Experts from BofA Merrill Lynch Global Research visited and spoke with store workers/owners at over 120 retail outlets in Mumbai in the week leading up to Diwali. While Mumbai is not India, yet the conversations help create a useful reference for recent festive season demand trends.

“Feedback from our visits is not encouraging: a majority of retailers reported weak festive sales with little hope or visibility of improvement. This a) confirms recent weak macro data, b) suggests some consumer companies may need to reduce elevated inventories, affecting upstream sales, and c) could drive earnings misses in some corners of the market. Indian staples/ discretionary stocks have recently moved sharply on the back of EM strength and trade at particularly elevated multiples. Earnings misses could hurt,” says Sanjay Mookim of BofA Merrill Lynch Global Research.